Iron ore market seen as the cornerstone of a new commodities super cycle

A train carrying 30,000 tonnes of iron ore wends its way to a WA port. Image: Getty

- Investment banks have a price target of $US150 to $US165 per tonne ($197 to $216/tonne) for iron ore

- ‘Looking at the 2020s, we believe similar structural forces to those which drove commodities in the 2000s could be at play’

- Chronic underinvestment in new mines means supply has not kept pace with surging iron ore demand

Many market experts are seeing the early signs of a new super cycle in commodities, including iron ore, that could equal the wild ride that prices experienced in the 1970s and 2000s.

What is more, they single out iron ore as a commodity heading for an inflection point when prices stay at elevated levels for a considerable period of time.

“Looking at the 2020s, we believe that similar structural forces to those which drove commodities in the 2000s could be at play,” said investment bank Goldman Sachs in a report.

In terms of the scale of the new commodities boom, an indication was given by Goldman Sachs’ global head of commodities research, Jeffrey Currie, in a recent speech.

“Policy driven demand is going to create a capex cycle that is bigger than the BRICs (Brazil, Russia, India, China) in the 2000s, not quite as big as the ’70s, but we are talking about that kind of a bull market in commodities,” Currie told a business forum in December.

The bank has a price target for iron ore of $US150 per tonne ($197/tonne) for the first half of 2021, reporting that it sees a market deficit for the period.

“Seasonal disruption risks remain elevated in the near term on seasonal weather trends in both WA and Brazil.

“On the demand side, China’s mill restocking is also a current tightening influence onshore,” said the bank in a report.

Analysts at Morgan Stanley also hold to a bullish scenario for iron ore prices in the years ahead.

They laid out a ‘plausible scenario’ in a report last week of iron ore prices trading at more than $US165 per tonne ($216/tonne) for a three-year period out to 2024.

Under-investment sows the seeds of next boom

The bullish case for iron ore eloquently outlined by investment bank analysts and other market experts is shared by many in the iron ore industry.

They include Magnetite Mines (ASX:MGT) director Mark Eames who suggested under investment in the industry over the past few years has sown the seeds of a new upswing in prices.

“We had a big crash in 2015 particularly in iron ore, but also in metals, and the mining industry effectively shut down investment beyond sustaining capital and there has been very little growth capital in iron ore,” he said.

The metals markets crash of that time also had a devastating effect on the industry’s lower tier of iron ore producers in Australia, and wiped out a good many of their number.

Only a few new mines have been brought on stream by major iron ore producers in the past few years, and most are replacement mines for depleted ore bodies.

Fortescue Metals Group’s (ASX:FMG) $1.8bn Eliwana mine with a production capacity of 30 million tonnes per year came online in December and partly replaces its Firetail operation.

The Andrew Forrest-led company is also planning to build a 22 million tonnes per year mine, Iron Bridge, at a cost of $3.4bn that has a start-up date in 2022.

BHP’s (ASX:BHP) $3.6bn South Flank project, which replaces its 80 million tonnes per year Yandi mine, is around 85 per cent complete.

Rio Tinto’s (ASX:RIO) $3.5bn Koodaideri project for 43 million tonnes per year is set to start up later this year and is another replacement project.

Hancock Prospecting’s Roy Hill mine plans a marginal, 5 million tonnes pear year expansion of its output to 65 million tonnes also in 2021.

“The existing major producers — BHP, Rio and Vale — have given a lacklustre response to a doubling of iron ore prices as there has not been any change in their output. The only explanation is that they are already flat out,” he said.

Australia accounts for the lion’s share of supply for the seaborne market for iron ore, with the balance largely made up by Brazil which has suffered some recent supply setbacks.

They include the Brumadinho and Samarco mine dam failures in 2019 and 2015, respectively, which have slowed the flow of iron ore exports out of Brazil.

“A number of other iron ore exporting countries such as India and Iran have dropped out of the market,” Eames added.

Magnetite Mines is developing its Razorback high-grade iron ore project in South Australia for which a pre-feasibility study is advancing.

Steel production in China seen as robust and growing in years ahead

Eames played down suggestions that Chinese steel production could crater, as this scenario has not happened to any major industrialised country.

This is because they tend to move from one type of steel-intensive production such as for construction, to another, consumer goods like cars and washing machines.

“No country that has produced steel in large volumes historically has ever seen production crash,” he said.

China’s urbanisation levels are currently around 50 per cent compared to a level of 80 per cent in Europe and North America, indicating the Asian country still has some way to go to equal urbanisation rates in Western countries.

“Chinese steel production has picked up against all expectations and while some people predict it to fall, there is the simple dynamic of stronger-than-expected demand, little investment in new mines and limited investment in replacement mines,” he said.

Current steel production in China is around 1.1 billion tonnes per year and has increased by around 200 million tonnes in the past few years.

“That means another 300 million tonnes a year of iron ore is needed. So a new mine of 20 million or 50 million tonnes per year is a drop in the ocean compared to that incremental demand,” Eames said.

This is a point often missed by market commentators who focus on monthly trade flows and who perhaps overlook the growing gap between demand and supply for iron ore.

“Structurely, market demand has gone up by hundreds of millions tonnes, while supply has only gone up by tens of millions of tonnes,” he said.

To see the iron ore market return to levels of five years ago — $US40 per tonne — would require an additional 150 million tonnes of production, said Eames.

In the meantime, some of the current supply lag is being filled by shipments from non-traditional supply sources such as Ukraine.

Elevated market prices are a response to under-investment

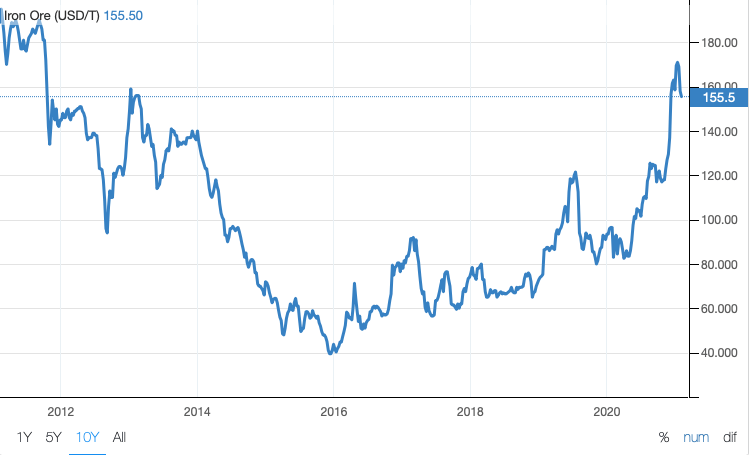

The market’s backdrop of increasingly tight supply and rocketing demand goes a long way to explaining why spot prices for seaborne-traded iron ore are trading at $US160 per tonne.

“The price response we are seeing now is predictable,” said Eames.

There is also very little that major iron ore companies can do in the short term to release some of the price pressure in the market.

“There is practically nothing that they can do about their iron ore output for this year that they have not already done,” he said.

Lead times are very long for building new mines and related infrastructure such as railways, and for ordering and taking delivery of new mining equipment.

“It can take years to get more trains and trucks into the system, or to lay new track or to add new dump stations,” he said.

Today’s spot price is also not too far off from historical levels.

Iron ore prices over the past decade have averaged around $US100 per tonne.

This has also been the commodity’s average price over the past 80 years on an inflation-adjusted basis.

“One of the reason for the [industry’s] structural under investment is that you need higher prices to incentivise new mines to be built, and people will not build new mines until that happens,” said Eames.

“Typically you need a price of around $US100 per tonne plus before you build a new mine.”

Headline prices for iron ore can also lead to confusion as they represent a standardised price for cargoes arriving in Chinese ports on a cost and freight (CFR) basis.

This means the price includes freight and shipping costs which can be considerable, and there can be discounts for the moisture content of iron ore cargoes sold on wet tonne basis.

Around 8 to 10 per cent of an iron ore cargo can be moisture from processing the ore.

There is also quality adjustments to be accounted for, as the standardised price is for cargoes with a 62 per cent iron ore content, and cargoes with a lower iron content earn less.

Transaction prices for lower quality iron ore can be at a significant discount to standardised cargoes, and the gap is growing as Chinese buyers seek higher-grade shipments.

In this context, current market prices for iron ore of $US160 per tonne may be the market signal needed to encourage investors to build more production capacity.

At Stockhead we tell it like it is. While Magnetite Mines is a Stockhead advertiser, it did not sponsor this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.