Your economy doesn’t add up: Business confidence surges, consumer confidence crashes

Via Getty

I usually have zero interest in the monthly measurements of sentiment and confidence, but these ones are good and weird.

Three reliable reads make for unreliable conclusions. Business confidence is surging, while consumer confidence is collapsing.

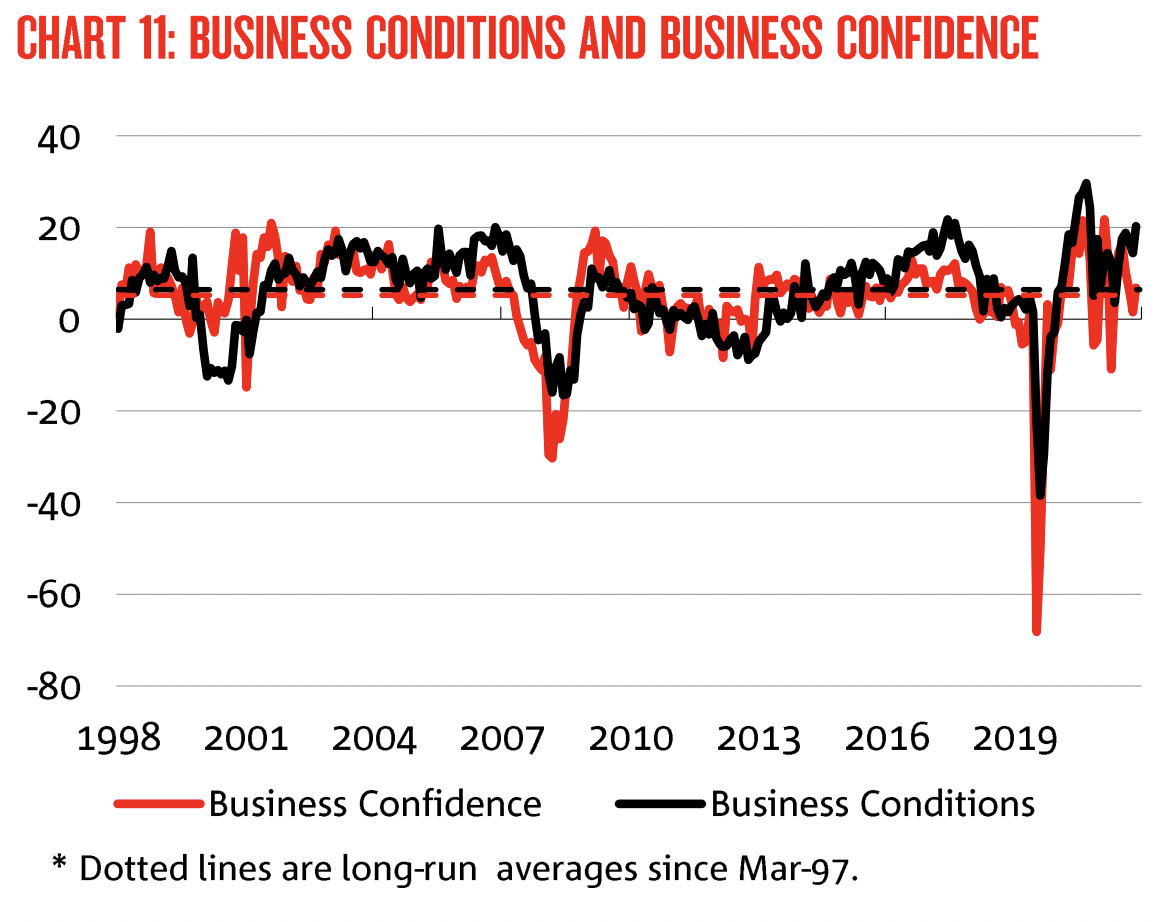

Let’s start with NAB’s Monthly Business Survey:

AMP Invest’s senior economist Diana Mousina says for once these monthly confidence surveys are highlighting a clear divergence as upbeat businesses confront unhappy consumers.

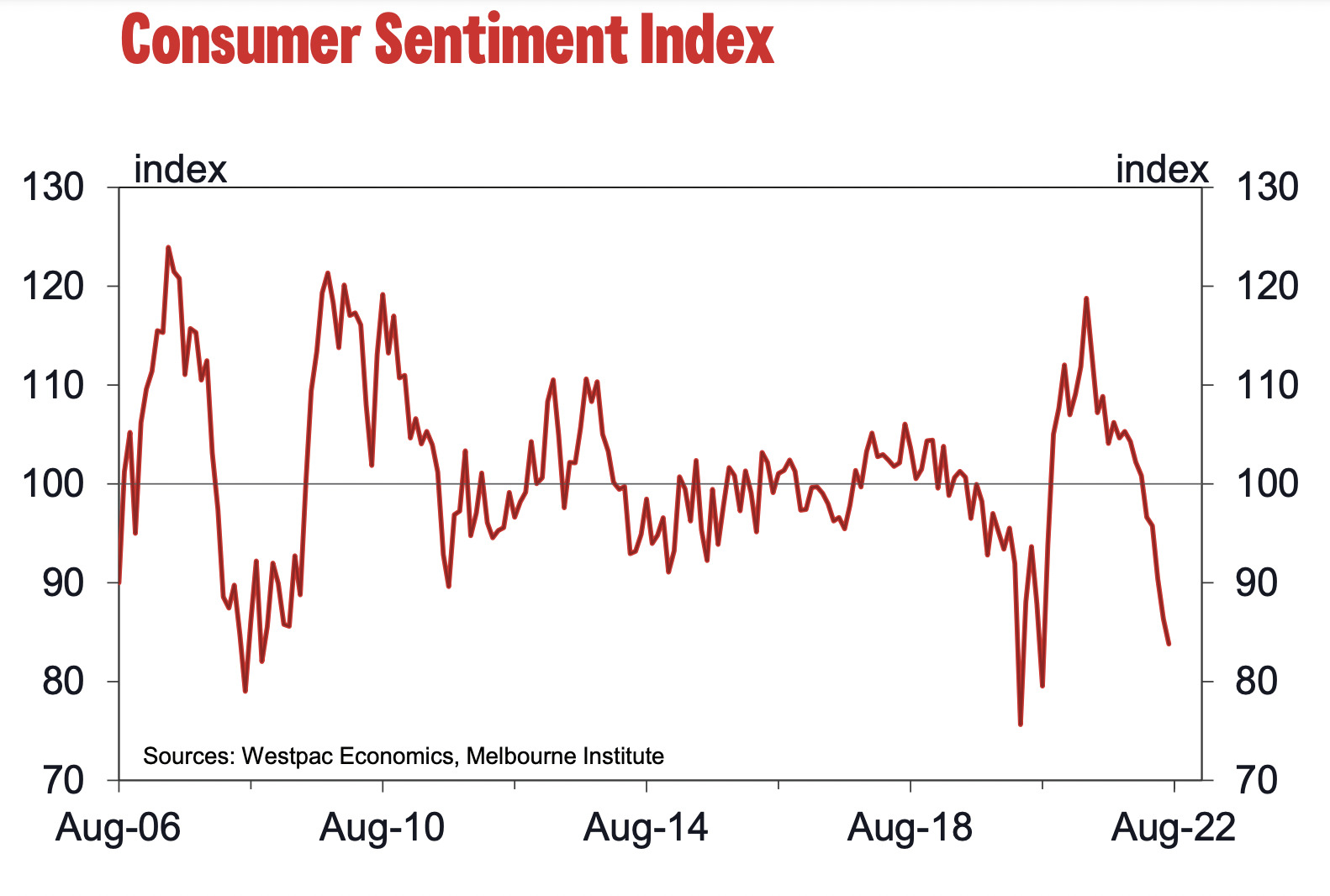

Consumer confidence fell by 3% in August to an index of 81.2 (any reading below 100 means that the average consumer has a pessimistic outlook), 22% lower than a year ago and tracking around recession-like levels (see the chart below). Business confidence, according to the NAB survey, rose to an index of 7, from 1 last month and business conditions rose to 20 from 13 – above long-run averages levels.

So here’s three almost infinitely-running sentiment surveys showing Aussie business confidence sort of inexplicably rallied last month even as Aussie consumer confidence turned unexpectedly gloomy.

NAB’s July Biz Survey, which puts the gentle word on 400 (non-farm) businesses between 19 to 29 July, has business confidence jumping five points to +7 – just above its long-running average.

Even more compelling for business which like to boom, NAB says capacity utilisation (like when a business is working at peak) is at the highest level in the survey’s heroic 25-year history.

The bank described the result to AAP as really stunning.

Business is great, custom is crap

But the other two surveys focusing on how consumers feel about the commercial world, also released this week, showed confidence dropping again last week as the Reserve Bank increased interest rates for a fourth month in a row.

The Westpac/Melbourne Institute Survey of Consumer Sentiment recorded its ninth straight monthly decline, while the weekly ANZ/Roy Morgan Australian Consumer Confidence also put consumer confidence in a room where the walls have started closing in fast.

Here’s the Westpac read in brief:

-

Consumer Sentiment Index falls 3% to 81.2.

-

Confidence now down 22.9% since November 2021.

-

House Price Expectations tumble 7.5%.

-

58% of respondents still expect the cash rate to increase by 1% or more over the next year following the 0.5% increase in August.

-

Confidence of mortgage borrowers down by 8.9%.

-

Confidence in the job market improves by 5.8%.

Westpac’s Bill Evans says it’s ominous just how fast the pace of these price increases have been going up.

And that’s not fun.

Especially as the price of the average Aussie Castle is whittling ever lower after the historic pandemic era gains.

“A strong message from the collapse in the index over the last nine months has been the negative attitude to major household purchases where confidence has fallen almost as fast as the 12-month economic outlook,” the Westpac chief economist said.

Interest rates are weighing on us big time

July’s Westpac and ANZ consumer surveys went pretty dark, pretty fast.

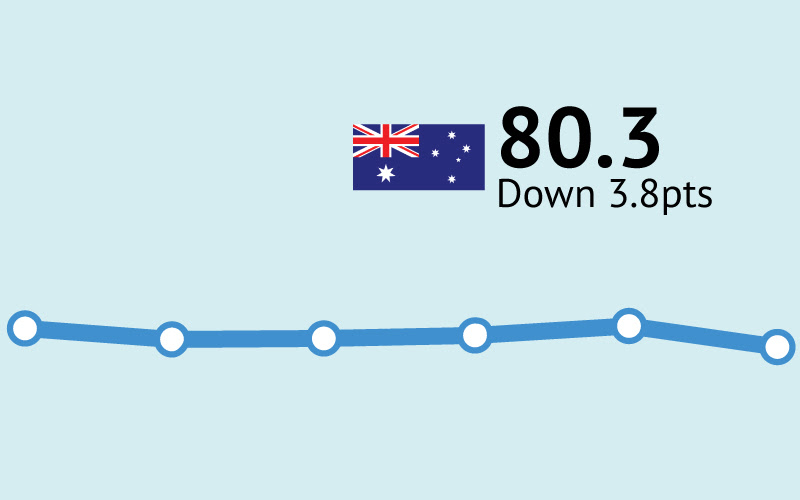

The ANZ/Roy Morgan How We’re Feeling index hit 80.3 – well over 18 points below what it was a year ago – and a better numerical read of human depression there ne’er was.

Confident shoppers are now a very significant 11.6pts below the already crappy 2022 weekly average of 91.9pts. The lowest ANZ read for over two years – right back to early April 2020 during the early stages of the pandemic.

The fall in Consumer Confidence followed the RBA’s decision to increase interest rates for a fourth straight month, increasing the official cash rate by 0.50% to 1.85%. The official cash rate has now increased by 1.75% since early May – the fastest rate of increase since late 1994.

Both conducted last week, both involving surveys of well over 1200 and 1500 Australian consumers respectively and hot on the heels of the central bank’s latest chunky 0.5% rate increase.

The surveys showed consumer confidence was on par with the levels last seen at the start of the COVID pandemic in 2020.

“Consumers are feeling negative about their current family finance situation and economic conditions over the next year,” Diana told Stockhead. “This makes sense in an environment of high inflation, rising interest rates and negative real wages growth.”

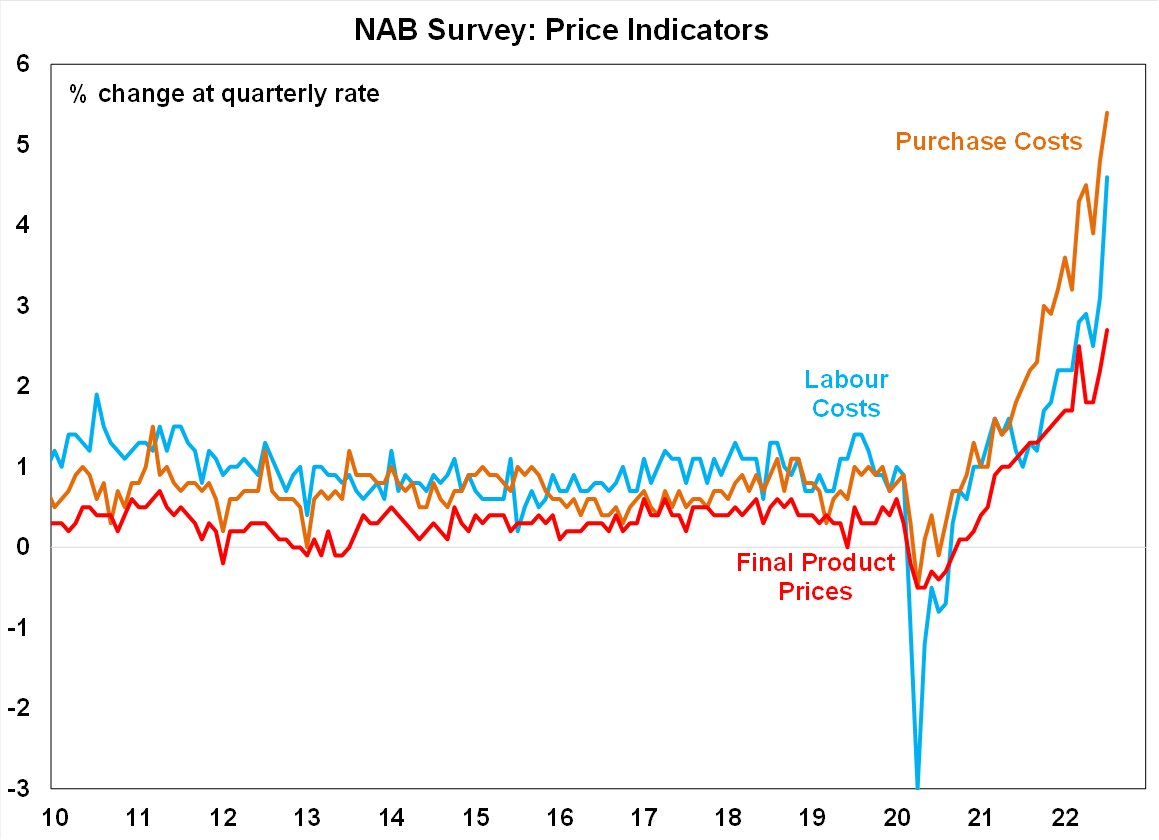

On the flipside she says business confidence is toppy, despite very steep increases in purchase costs and labour costs which also lines up with company earnings estimates remaining positive for the next year (at around +7%).

ANZ head of Australian economics, David Plank noted the 4.5% crash in consumer confidence came right off the back of the RBA’s hat-trick.

“Household inflation expectations increased 0.1ppt to 5.6% despite petrol prices falling for a fourth consecutive week. Demand for housing has been dropping, along with house prices.

“That and rising interest rates caused confidence among homeowners to drop 7% last week.”

The divergence is momentary and not monetary, Mousina says. But it won’t be because consumers suddenly find their mojo.

“While businesses have so far been able to pass on higher prices to consumers, this can’t last as consumer spending power has been hit from rate rises and high inflation.

“Also, while selling prices have risen, purchase and labour costs are rising faster which indicates some potential margin pressure for firms. As consumer spending volumes decline (which is just starting now), business confidence and conditions should also fall.”

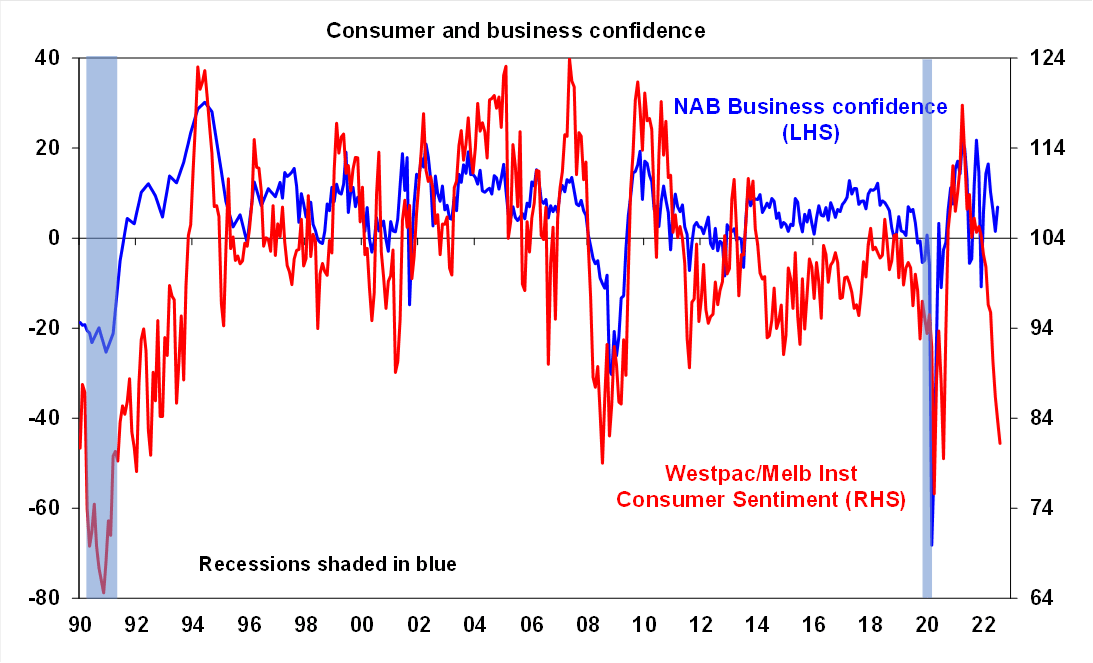

Source: NAB, AMP

Monetary policy acts with a lag, Diana says which goes some way to explaining the difference between consumer and business perceptions.

The strength in the business survey is unlikely to continue as consumer spending volumes start to weaken and margin pressure accelerates.

“The RBA would be expecting a softening in consumer confidence as rates rise, but would prefer spending to soften (to reduce pressure on inflation), without crashing,” Mousina says.

“This will be difficult for the RBA to achieve given the recent aggressive pace of rate hikes and expectations for more rate rises…although probably at a slower pace from here.”

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.