Oh damn, I hit the wrong button... never mind, no one'll notice. It makes an eerie kind of sense if you think about it... Via Getty

What economics data shocked and appalled us last week?

Friday night in America saw a bit of a modern twist on the traditional US jobs data “big show” which was eclipsed by excitement out of Asia – in this case talk of China putting an end to its COVID zero-sense policy.

“The Hang Seng and China A50 rallied over 5% while the USD fell close to 2% sending commodities like copper and iron ore up over 5%,”, Maqro Capital’s Mark Gardner said.

By Saturday morning commodities and the remorseless USD were having a reversal of fortune – the greenback fell nigh 2% while commodities we like round here – say copper and iron ore – jumped over 5%.

On the Nasdaq, Mark says, big tech made a recovery with Google (GOOGL) and Microsoft (MSFT) both rallying 3% as bargain hunters saw value in the companies currently trading at seven-year low PEs.

“With US CPI coming up on Friday this week, any sign that inflation is cooling will be the green light for buyers to start picking up undervalued quality companies while they have the chance.”

On local markets WA1 Resources put everyone else to shame. It’s up over 115% for the last week and well over 1000% for the month. The S&P/ASX Emerging Companies (XEC) index lost about 1% last week.

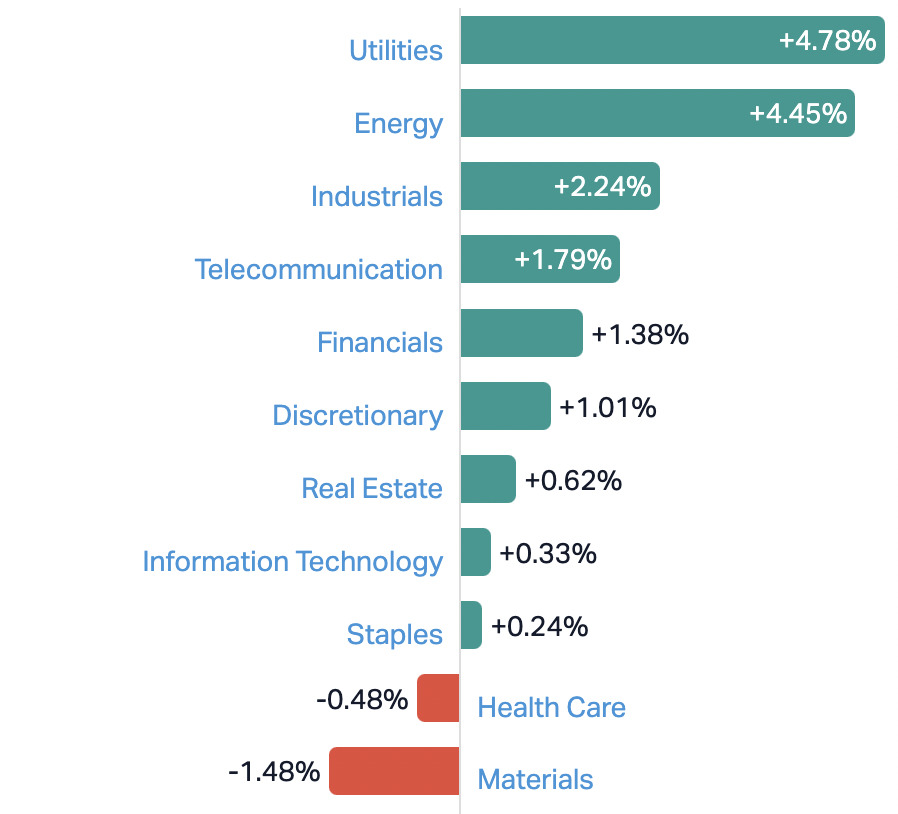

Although, fair play, the benchmark ASX200 gained about 0.8% last week, with all but two sectors ending the week in the green, aided and abetted by a slightly less hawkish RBA, with gains led by the Utilities, Energy, Industrials and Telecom Sectors.

Via Market Index

Jumpin’ Jerome Flash

Global markets took another week of whipsaw-existing in their stride, the major detonation on Thursday morning our time was another 75 basis point whack from the Federal Reserve in the US, reinforced by some blunt truth-telling from The Chair that interest rates may be higher than previously expected.

This saw US shares fall 3.3% for the week, but Eurozone shares rose 1.6% and Japanese shares rose 0.3%. Chinese shares rose 6.4% helped by talk of a relaxation in China’s zero-COVID thingy.

However Shane Oliver at AMP Capital says central banks are slowing, or moving towards slowing, their strangle-tightening, but “are still hawkish and signalling we are not at the top yet”.

“The RBA is at the least aggressive end of the major central banks, but it held tight to a repeat 0.25% lift also revising up its inflation forecasts to peak this year at 8% for headline and 6.5% for underlying.”

On the plus side, Dr Oliver sees evidence building that RBA rate hikes are working.

“Housing indicators are all very weak; falling home prices will depress demand (and raise financial stability risks); consumer confidence has fallen back anew; and retail sales appear to be stalling in real terms. By the time the RBA meets in February there is likely to be enough evidence demand is slowing which will slow inflation for it to remain on hold, or if not just raise rates once more with 3.35% becoming the peak,” he said.

Let’s get to the bottom line:

“The bottom line is that while central banks may slow the pace of tightening, which should reduce the risk of over-tightening, we are still a long way from a ‘pivot’ toward easing,” Dr Oliver said.

Until then the Americans running into recession seems likely, if not fitting.

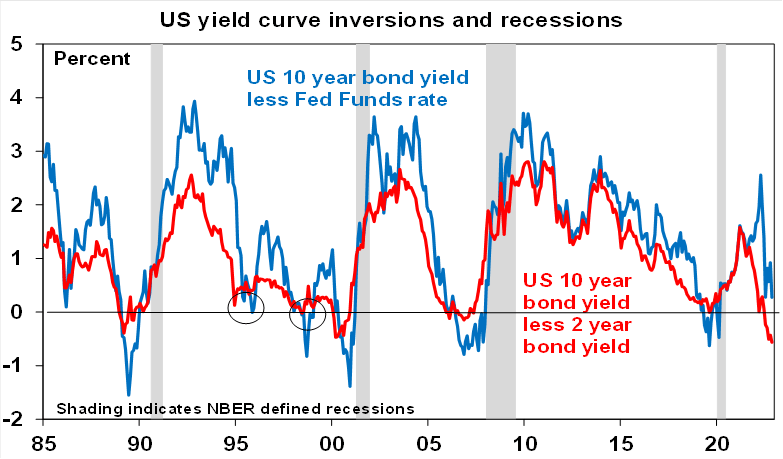

The US yield curve keeps curling into a deeper inversion for the 10-year/2-year yield gap which should keep traders and their shares teetering daily.

Dr Oliver says the flaring geopolitical problems – America v America, Brazil v Brazil, Ukraine v Russia, China v Everyone, Iran v Iran and South Korea v The Kims – add to the risk.

Via AMP Capital

However, here are two positives:

AMP’s forward looking prices measurement (Inflation Pipeline Indicator below) continues to show some slowing – suggesting inflationary pressures particularly for goods (which tends to lead services inflation) are continuing to recede.

And

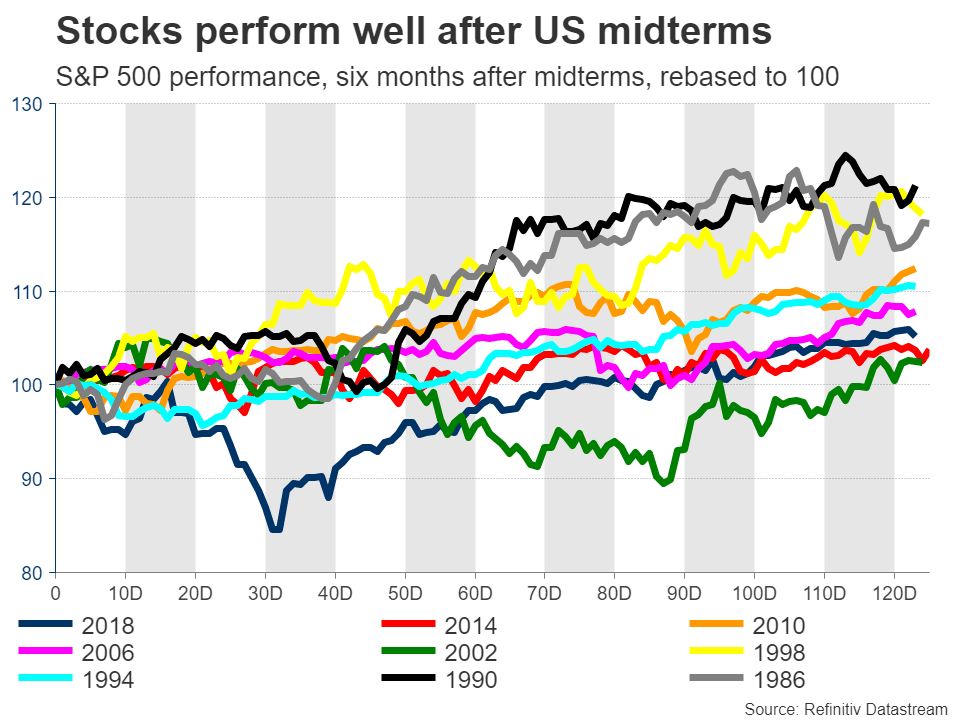

Shares (like me) like Christmas, and the run up to.

US shares also consistently rally after US mid-term elections Tuesday, with year three in the four-year presidential cycle normally being a strong year on average after year two (ie: this year) which is normally a poor year.

Via Refinitiv

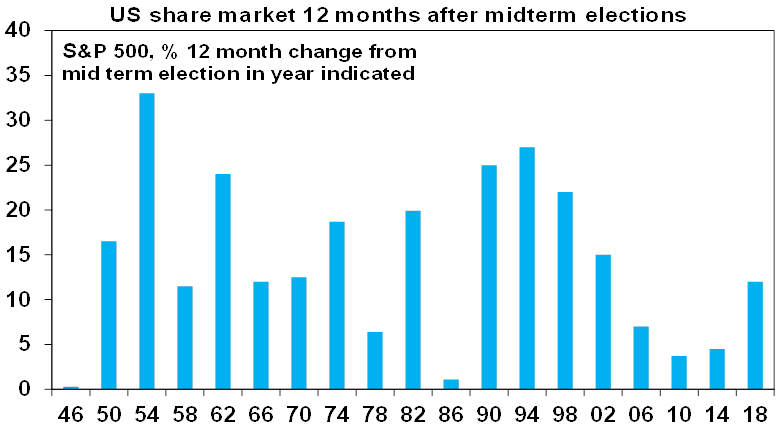

One’s Bidey Sense is tingling that The Dim’s are overdue a schellacking, gifting control of both houses (a curse upon them) to the Insane Ones (a curse upon them too).

Via AMP Capital

Also last week: Elon.

He was busy, as per. Pretty wrapped up in being Twitter’s new reaper:

Regarding Twitter’s reduction in force, unfortunately there is no choice when the company is losing over $4M/day.

Everyone exited was offered 3 months of severance, which is 50% more than legally required.

I’ve been meaning to post the graphs of the usage spike over the past week. But the best part is we don’t need to, because the data is all public and people like @AlexMahadevan can do an even deeper analysis! https://t.co/zGkO8UpDor

The world’s biggest summit on climate change COP27 is kicking off in Egypt.

We’re also pretty gripped here by the prospect of this week’s consumer price index (CPI) read in the States, as well as a few inflationary indicators out of best bud, China.

We’ll also be looking closely at how October trade figures come in for La Chine, while in l’Angleterre it’s blame the new PM Q3 GDP figures, which, as I’ve previously mentioned, but worth a second run up the flagpole, are likely to be very unTrussworthy.

German industrial production drops and while it won’t be The Weimar Republic, expectations are not sky high.

At home, Kristina Clifton at CBA says she’ll be watching:

“On Tuesday we expect the Westpac/Melbourne Institute consumer sentiment measure to remain in deeply pessimistic territory (it fell by 0.9% in October and the weekly ANZ Roy Morgan survey has also shown recent weakness.) The NAB business survey is also released the same day and has shown considerable resilience in recent months.

“We could see this continue in October given the lags in monetary policy transmission. The pricing measures in the survey will also be closely watched given inflationary pressures in the Australian economy.”

CommBank releases its Household Spending Intentions Index for October next week as well.

The Economic Calendar

Monday November 7 – Friday November 11

All sources from Westpac, Trading Economics

Australia and New Zealand

MONDAY

ANZ Job Advertisements

Ai Group Services Index

TUESDAY

Westpac Consumer Confidence Index

NAB Business Confidence

WEDNESDAY

ABS Private House Approvals & Building Permits

RBA Bullock Speech

THURSDAY

Consumer Inflation Expectations NOV

Global

MONDAY

CN Balance of Trade OCT

WEDNESDAY

CN Inflation Rate, PIP

US MBA 30-Year Mortgage Rate

THURSDAY

US Inflation Rate

US Core Inflation Rate OCT

US Wholesale Inventories

FRIDAY

GB GDP Growth Rate

GB Industrial Production

GB Balance of Trade

Here’s some of the ASX IPOs ahead in November:

Now imagine in this space I put a pretty official disclaimer absolving me of any marriage to these numbers. Probably in bold and maybe italics, it’ll say something like – honestly, you can’t trust the dates of these IPOs. I really have NFI how it works.

Taiton’s delayed IPO features projects that include the Lake Barlee gold project in WA, the Highway poly-metallic project in SA, and the Challenger West gold project also in SA.

The company believes its dominant land holding at the Highway Project will allow it to potentially uncover the next elephant deposit in Australia.

Taiton will be undergoing a series of grassroots exploration and also several walk-up drilling targets.

Tiger Tasman Minerals has projects in WA and QLD focused on copper, lithium, nickel, manganese, silver, gold, base metals and industrial minerals (DMM) essential to the global clean energy transition, decarbonisation and a more sustainable future.

The projects are in proven and prospective jurisdictions including Paterson Province, Fraser Range, Earaheedy Basin, Ashburton and the Townsville region.

The Iron Skarn silver-copper-lead-zinc project (QLD), the Copper Canyon copper-gold project (WA), the Fraser Range lithium-nickel-copper project (WA), the Mt Minnie manganese project (WA) and the Crater copper-zinc-lead-silver-gold project (WA).

This company develops and sells Unmanned Aerial Vehicles (UAVs) or drones for commercial applications – and there’s a bunch of them.

NGL says its tech has applications across solar farms, ports, O&G facilities, critical infrastructure like dams and power stations, in construction, border patrol, securing pipelines, fire and oil spills along with search and rescue, crowd control and for prisons.

Basically, the drones can respond to a threat; when a security alarm is triggered the system automatically dispatches a drone to the alarm location and streams live video to the security team.

DeSoto holds the Pine Creek project in the Northern Territory’s prolific Pine Creek gold and pegmatite province.

The company’s six granted licences will cover 1,467km2 and three licence applications cover 420km2.

Historical drilling has identified gold mineralisation hosted but there has been no lithium exploration conducted in the Project area – which DeSoto sees as a “significant” opportunity.

It also takes encouragement from the fact that Core Lithium (ASX:CXO) recently acquired ground adjacent to the Pine Creek Project and is now exploring for lithium across the Project area.

This resources player is focused on developing a gold platform in West Africa.

The company is primarily focused on the development of the Kobada Gold Project in Southern Mali, which has a global resource base of over 2.3 Moz of gold and the potential to produce more than 100,000 ounces of gold per annum.

SC1 provides a scientific provenance verification service for agriculture, seafood, mining and resource sectors.

SC1 says scientific analysis of physical product samples allows clients to mitigate risk, validate digital data, protect their brand and support transparency within their supply chains.

The company’s origin verification solution is able to identify the mine, farm, fishery or plantation from which a product originated.

Orpheus was established to explore for and discover greenfield uranium deposits in South Australia and the Northern Territory at economic grade and scale.

And the focus is exploring around approved and operating (or recently operating) uranium mines because these are also the jurisdictions considered to have high prospectivity for economic uranium deposits and have the regulatory systems at both state and federal level supportive of the development of new uranium mines.

They have four projects in the NT – Woolner, Ranger North-East, Mt Douglas and T-bone – and two projects in SA – Frome and Cummins.

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our

Privacy Policy.

Get the latest Stockhead news

delivered free to your inbox

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our

Privacy Policy.