The worst of the worst: Wolfe Research names Albemarle and Tesla among Wall Street’s most likely to blow up your money

Via Getty

The American independent sell-side research firm which calls its analysts the Wolfpack (it’s Wolfe Research) has sifted through the ashes of Q4 on Wall Street and cherrypicked the select handful of stocks which could blow up at anytime.

If the worst of the worst or just that special kind of stock which can single-handedly implode a portfolio is your thing, then read on.

Based off the latest Q4 earnings, Wolfe has sifted through the potentially underperforming Wall Street muck using its bare hands and an earnings quality score, which sucks up all kinds of variables like valuation metrics, all kinds of financial ratios and a bit of sentiment.

Wolfe doesn’t sugarcoat the list either:

“With the Fed tightening, economic growth slowing, and recession risks rising, we expect a larger number of stock blow-ups over the coming quarters. Our work in this note focuses on the balance sheet and cash flow statement as leading indicators of potential earnings misses or other income statement issues.”

Altogether Wolfe’s pack looked at some 2,400 stocks with market caps over US$250 million.

From this group, the very worst 240 or so (the bottom 10% of its earnings quality score) got the full spotlight treatment. According to the Wolfe format, these muffins scored – on average – an underperform of circa 4% annually.

Not quite done, Wolfe Research also identified stocks with glaringly high short-seller interest relative to the company’s sector.

Short selling a stock means that investors are betting it will fall in value. When investors short a stock, they first borrow shares and sell them at market price. If the stock price drops, the investor can buy back the shares at a lower cost and then profit from the difference.

In this case, Short Interest is a measure of the percentage of equity in the target company is being shorted by investors.

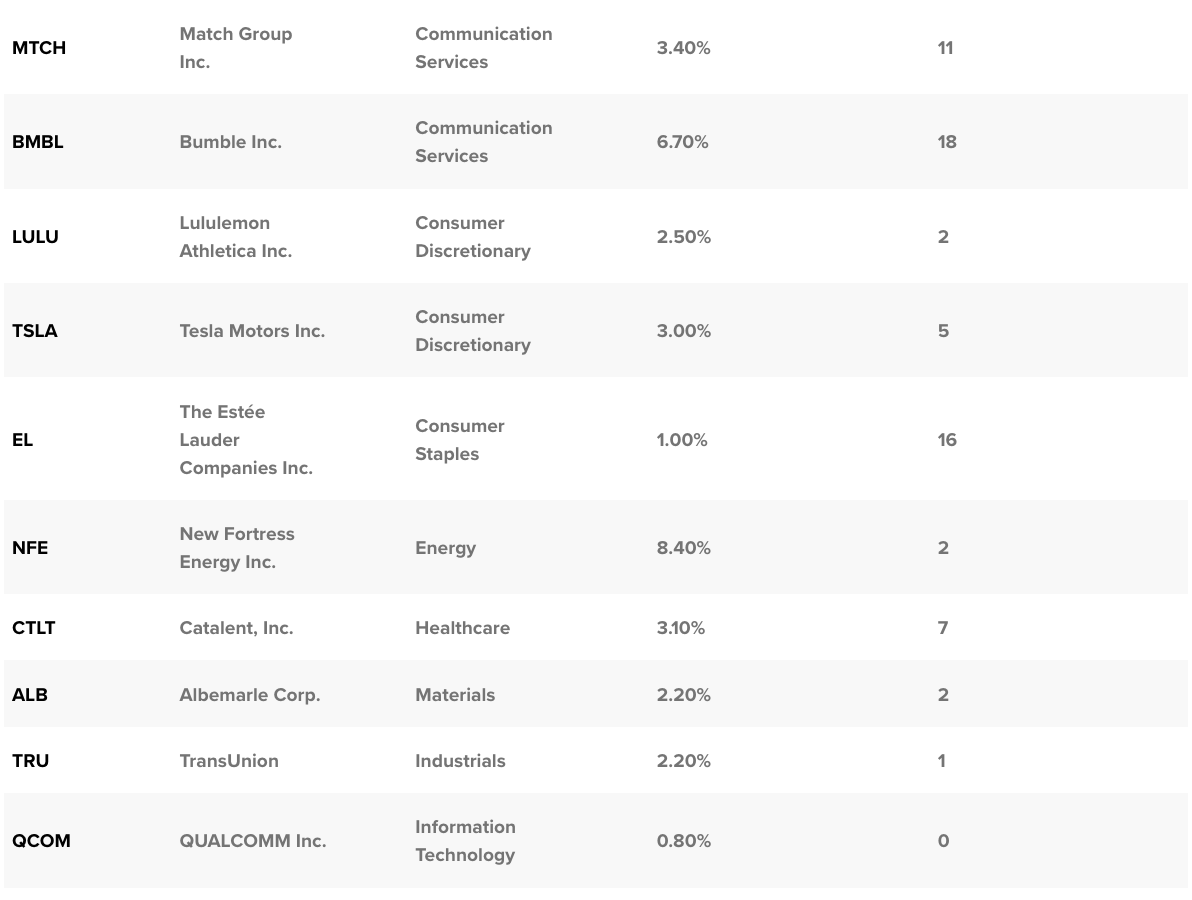

Here’s their worst of the worst:

A few standouts from the Wolfpack’s sample:

Tesla (TSLA)

Shares in Elon’s cars were downgraded by the Wolfpack a few weeks ago. From “Outperform” to “Peer Perform.” Although Wolfe remains ‘optimistic’ about Tesla’s long-term outlook, there’s some deep concerns about macro-economic headwinds over the short-to-mid.

“We’re still convinced of Tesla’s impressive cost trajectory, which should propel impressive growth over time. However, we’ve also become incrementally more concerned about macro challenges. Tesla has already had to cut prices quite a bit more than we expected. And we worry that macro challenges are intensifying in ways that could disproportionately affect US EV makers,” Wolfe noted.

Tesla stock jumped over 6% on Friday as the Nasdaq Composite surged +1.75%.

A very favourable tweaking of Electric Vehicle tax credits in the States are behind the bump, while a waiver from Environmental Protection Agency (EPA) will allow California to electrify its heavy duty truck fleet faster is an additional tailwind.

Tesla is up about 68% so far this year, marking the best start to a year in the company’s history.

That said, the shares did collapse by about the same amount in 2022.

Match Group Inc (MTCH)

The online dating firm Bumble made Wolfe’s worst of, but its rival online dating company Match Group Inc was less attractive.

This is Dallas headquartered, very American internet and technology play with what it says is the ‘largest global portfolio of popular online dating services.’

It’s the home of Tinder, Match.com, Meetic, OkCupid, Hinge, PlentyOfFish and OurTime, among a total over 45 global dating companies.

But for now it’s all about Tinder.

From Match Group’s Q4 2023 Shareholder Letter

Tinder plans to launch its first-ever global marketing campaign this quarter. From its inception, Tinder grew rapidly through strong, organic word-of-mouth, so there was less of a need to market. However, over time, this lack of marketing has contributed to a narrow brand perception that does not celebrate the breadth of relationship possibilities Tinder creates every day. Through a fresh, multi-channel brand campaign, Tinder will have the opportunity to showcase the full range of what it offers and develop a more accurate brand story that resonates with its core audience.

We believe that investing to build and properly position Tinder’s brand will, over time, help engage both new and previous users, and cement its position as a premiere global dating app.

Wolfe is not impressed and won’t be swiping right.

“Match Group is one of the companies with consistent earnings adjustments that increase GAAP, or generally accepted accounting principles, earnings by at least 20% for over 9 of the last 12 consecutive quarters. This is an additional negative sign for the stock as consistent differences in GAAP and non-GAAP earnings could indicate lower likelihood of persistence of those earnings.”

Match Group, whose portfolio of brands includes Tinder, have fallen 7.2% in 2023. The company has an earnings quality score of just 11.

Albemarle Corp (ALB)

In the headlines for throwing money at an unresponsive ASX lithium play Liontown (ASX:LTR), the US-based lithium manufacturer Albemarle has all kinds of red flags for Wolfe.

Liontown on Tuesday rejected a takeover offer from the lithium giant valuing the mine developer at $2.50 per share – a big premium to Monday’s closing price of $1.54.

Ablemarle has built a ~2.2% stake on-market, previously offered $2.35 per share on 3 March, and $2.20 per share on 20 October 2022. There’s a smack of desperation in the air and everyone knows it. Josh Chiat as ever has all the juiciness on the LTR play.

“In coming to its decision, the Liontown board noted the opportunistic timing of Albemarle’s indicative proposal, coinciding with recent softness in companies exposed to the lithium sector and the pre-production status of the Kathleen Valley project.”

ALB has a short interest of 4.6% and an earnings quality score of just 1. Albemarle disgraced itself again in the new bid to acquire LTR, which holds two lithium deposits here.

RBC’s US analyst Arun Viswanathan says investors may not look favourably on ALB were it to make another attempt at a deal at an increased offer price given lithium prices are falling.

If they continue to fall, projects like Kathleen Valley could be available cheaper later in the year, according to Viswanathan, but there are positives as well, he noted.

“With that said, if the deal did go through, we see three positives: 1) ALB would increase its backward integration and have greater access to spodumene resources, 2) ALB would gain more control over how much supply comes online, and 3) ALB would have greater control of when new supply comes online.

“Recall ALB had ~200ktpa LCE of conversion capacity in 2022 ramping to 500-600ktpa by 2030e, and therefore is likely interested in securing more spodumene resource capacity.”

Shares of Albemarle are up 3.5% in 2023.

Albemarle investors have fled the giant over the last month, on fears for the slumping price of lithium carbonate prices in China.

It’s down 35% over the last month.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.