Tech Heavy: Disney and a dating app to wrap up Q2 earnings under shadow of US CPI read

Via Getty

Welcome back to your weekly preview to what’s about to blow up on Wall Street’s and it’s tech-laden Nasdaq a few hours from the open of a new of trade. With Wednesday’s key CPI read, all eyes are on Disney’s 2Q numbers, life for Coinbase following its big date with Blackrock and the attraction of US dating app Bumble.

Ahead of the open, things actually seem to be trotting along extraordinarily well Stateside.

After the S&P 500 closed Friday out with a third consecutive weekly gain, US Futures remain bedraggled, but not disgraced – US investors are probably not enjoying their proximity to another very important inflation report on Wednesday.

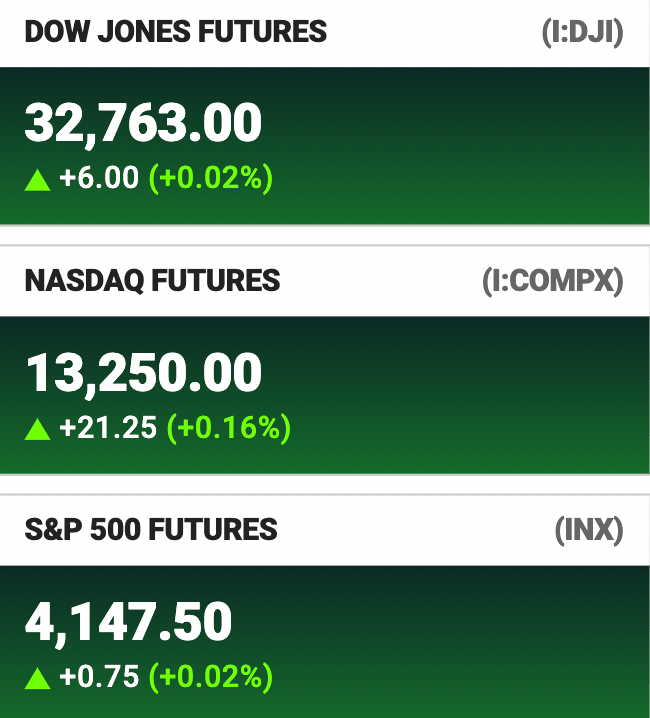

Futures have turned higher. on the Dow Jones and the Nasdaq are ever so slightly higher – 0.02% and 0.16% – pm Sydney time on Monday. The S&P 500 is ahead at 0.02% above parity.

Last week’s Wall Street gains were amplified by the unexpectedly strong monthly jobs report, which, despite the indicator’s recent volatility, has gone some way toward taking further sting out of recessionary fears.

The US added 528K full-time positions in July as the American market clawed its way back to where things were before the COVID-19 pandemic shredded 22 million US jobs.

The ISM services index surged to 56.7, much better than the consensus estimate of 53.5. US factory orders also impressed, another sign the economy keeps chugging along.

That’ll be encouraging for The Federal Reserve, which will look to continue using rate hikes to quell record high US inflation.

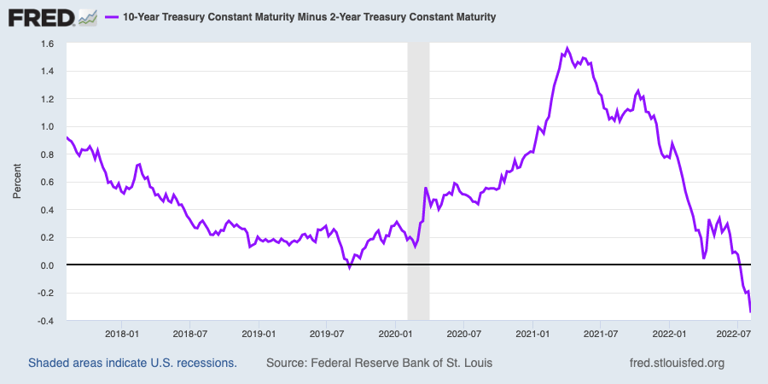

On the more disturbing side of the ledger, as Eddy Sunarto points out, Wall Street seems intent on ignoring the deepest yield curve inversion since around 18 months after the dotcom unboom.

The 2yr vs 10yr US yield curve spread is now at 40bp.

That’a a recession indicator and the higher the spread is, the higher likelihood of a recession – given an 18-month lag.

Company news this week

Amazon (AMZN) said it would acquire iRobot last week for US$61 a pop, in an all-cash deal putting the Roomba maker at $1.7bn. The robotic vacuum maker iRobot, has been branching out into other home cleaning robots like mops and lawn mowers.

Oracle reportedly laid off hundreds of employees last week, and flagged it using Linkedin. The business software provider is putting its healthcare IT services and cloud businesses ahead as priorities reports out of Fox News have suggested.

As always, we’ll be watching Elon and Twitter. Mr Musk says his $AUD62bn takeover should be good to go, if he can confirm details about how Twitter measures for ‘spam bots.’

The billionaire and Tesla CEO has been trying to back out of his April agreement to buy the social media company, leading Twitter to sue him and Mr Musk to counter sue.

Earnings Highlights

This week will bring the Q2 reporting season to a close.

Over 430 of the S&P 500 companies having already delivered their earnings and according to data from Refinitiv, well over three-quarters have been a beat on expectations (using an earnings per shares EPS metric).

Nearly 70% of companies posted quarterly revenue that topped analysts’ estimates, according to Refinitiv.

Berkshire Hathaway reported Saturday that its operating profits jumped 39% from a year ago in the second quarter despite fears of slowing growth. However, Warren Buffett’s conglomerate was not immune to the overall market turmoil with a whopping $53 billion loss on its investments during the quarter.

Coinbase Global (COIN) was i the news last week when it revealed a deal with great big asset manager BlackRock (BLK), allowing BlackRock’s institutional investors to buy bitcoin via the cryptocurrency platform. They report on Tuesday.

Other highlights include Palantir Technology (PNTR) on Monday, Ralph Lauren (RL) on Tuesday and keen beans will be watching Disney (DIS) data on Wednesday. DIS is slated to report its fiscal 3Q results after Wednesday’s close US time. Analysts, estimate earnings of $1.00 per share for the three-months to June 30, (+44.9% YoY), with revenue to jump 20.6% to $20.5 billion.

The American online dating app Bumble (BMBL) has been a bit of a goer so far in 2022, shares up about 10% year-to-date – easily outperforming the broader market’s roughly 13% loss.

US Earnings Highlights and Economic Week Ahead:

MONDAY

Novovax (NVAX)

News Corp (NWSA)

Palantir Tech (PNTR)

TUESDAY

Carlyle Group (CN)

Coinbase Global (COIN)

Ralph Lauren (RPN)

US Labour costs and productivity (June quarter)

US Consumer inflation expectations (July)

WEDNESDAY

Bumble (BMBL)

Walt Disney (DIS)

US Consumer Price index (CPI, July)

US Monthly budget statement (July)

THURSDAY

Baidu (BIDU)

Brookfield Asset Management (BAM)

US Producer Price index (PPI, July)

US Import and export prices (July)

FRIDAY

Broadridge Financial (BR)

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.