Traders’ Diary: Everything you need to get ready for the week ahead

Traders Diary: Economic and IPO calendar for the week. Picture Getty Image

- The stock markets rallied last week, despite fresh geopolitical tensions

- Headlines last week include RBA and BOE rate hikes, and strong US non-farm payrolls

- Quiet week of data ahead this week

World stock markets rallied last week, led by the Nasdaq which was up by almost 3%. The S&P 500, the ASX 200, Nikkei and Hang Sang were also up by around 1%.

The week was headlined by geopolitical tensions sparked by Nancy Pelosi’s visit to Taiwan.

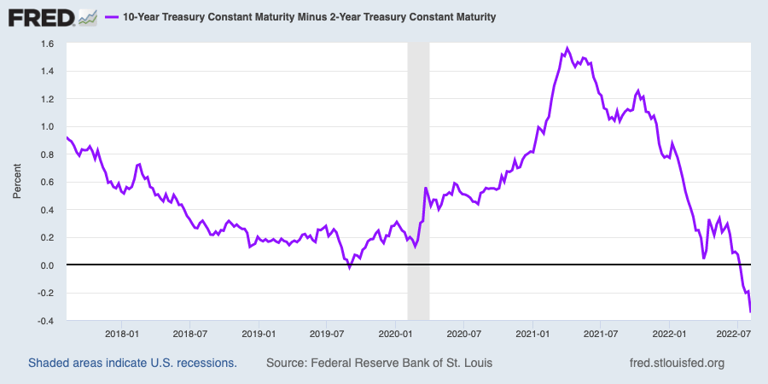

On the economic front, the bear market rally is picking up pace and Wall Street seems to ignore the deepest yield curve inversion since the early 2000s.

The 2yr vs 10yr US yield curve spread is now at 40bp. The spread is a traditional indicator of predicting a recession and the higher the spread is, the higher likelihood of a recession although there is usually an 18-month lag.

Investors were also impressed by the earnings release of some of the biggest names. Earnings highlights include Amazon posting a US$121 billion in Q2 revenue, beating analysts’ expectations by more than US$2 billion.

EBay reported Q2 revenue that beat expectations as it offered investors an upbeat profit outlook, while Apple posted a revenue record of US$83 billion for the June quarter, up 2% year over year.

In Australia, blue chips earnings are expected to be released this week.

Oil prices were wobbly last week on concerns of lower demand.

OPEC+ members agreed to the smallest increase in OPEC+ history. The cartel said they would increase production by 100,000 barrels a day in September, far less than the nearly 650,000 barrels a day that it agreed to add in July and August.

Here are the economics data making headlines last week.

US

US economic data continues to support the case that its economy is more resilient than expected.

The ISM services index surged to 56.7, much better than the consensus estimate of 53.5. US factory orders also impressed, another sign the economy keeps chugging along.

On Friday, the non-farm payrolls for July jumped past forecasts. According to the US Department of Labor, non-farm payrolls increased by 528,000 in July versus the forecast of 250,000.

Meanwhile, US jobless rate ticked lower to 3.5%, versus expectations of 3.6%.

“Certainly 75 basis points will be on the table for the next meeting,” Randall Kroszner, a professor at the University of Chicago Booth School of Business told Bloomberg Television.

The next FOMC meeting will be held on September 20.

Europe

The Bank of England (BOE) has slapped another 50bp hike, the steepest increase in 27 years as it took the UK cash rate to 1.75%.

The BOE has warned that the UK might enter its longest recession since the financial crisis of 2008-09, saying the British economy is expected to contract for five consecutive quarters beginning in Q4 this year.

Australia

The RBA hiked its rates by another 50bp last week to 1.85%.

The central bank warned against higher inflation and lower economic growth in the year ahead, while signalling that it’s not yet done with the rate hikes.

“The Board expects to take further steps in the process of normalising monetary conditions over the months ahead, but it is not on a pre-set path,” said RBA boss Philip Lowe.

“The size and timing of future interest rate increases will be guided by the incoming data and the Board’s assessment of the outlook for inflation and the labour market.”

Australia’s trade surplus has also hit a new record high of $17.7 billion, mostly driven by strong prices across our key exports.

Finally, retail sales topped forecasts in the June quarter. According to ABS data last week, Australian retail sales for the quarter rose an inflation-adjusted 1.4% from the previous quarter, beating market forecasts of 1.2%.

The Economic Calendar for this week

Source: Commsec

Australia and New Zealand

TUESDAY

CBA Household Spending Intentions (July)

Weekly consumer confidence index

Monthly consumer confidence index

NAB business survey

THURSDAY

Weekly payroll jobs and wages

Global

TUESDAY

US NFIB small business optimism index (July)

US Labour costs and productivity (June quarter)

US Consumer inflation expectations (July)

WEDNESDAY

China Consumer and producer prices (July)

US Consumer Price index (CPI, July)

US Monthly budget statement (July)

THURSDAY

US Producer Price index (PPI, July)

US Import and export prices (July)

The ASX IPO calendar for this week

According to the ASX, these two stocks will make their debut listing this week (subject to change without notice):

Listing: 11 August

IPO: $12m at $0.20

This nickel explorer is aiming to turn prospective nickel, cobalt and copper projects in Sweden into mines to satisfy demand from the electric vehicle and energy storage industries.

Bayrock’s Lainejaur deposit hosts 460,000t of ore within an area that equates only one per cent of the total licensed area the company holds, and contains 2.2% nickel, 0.7% copper and 0.15% cobalt along with 0.68g/t palladium, 0.2g/t platinum and 0.65g/t gold.

The company also has nickel targets across its 340.7sqkm of tenure known as the Northern Nickel Line – a collection of five projects called Vuostok, Nottrask, Skogstrask, Fiskeltrask and Kukasjarvi.

Australia Sunny Glass Group (ASX:AG1)

Listing: 12 August

IPO: $7.5m at $0.35

This Australian-based holding company, through its subsidiaries, operates a glass production and supply business for structural building facades.

The group has a fully automated processing plant which it says is highly efficient, accurate and scalable and an R&D focus on the development of cyclone-resistant glass using new laminating and bonding techniques.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.