Margin lending data shows Australia’s ‘army of day traders’ is growing strongly

Pic: metamorworks / iStock / Getty Images Plus via Getty Images

Margin lending data shows Aussie traders are leveraging up to buy stocks in record numbers.

The data is compiled quarterly by the RBA, and analysis by CBA strategists Martin Whetton and Philip Brown revealed some notable post-Covid trends.

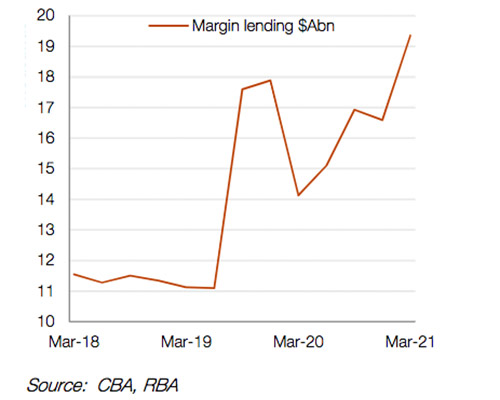

After a sharp fall in March 2020, the total amount of margin lending rose strongly to a new record high of almost $20 billion:

Margin lending — the breakdown

Margin lending allows a trader to take out a loan for investment purposes, using their current share portfolio or cash position as security.

If share prices fall, the size of the loan may climb above a designated maximum amount, relative to the value of the shares used as security (loan-to-value ratio).

In that case, the user will be required to add more cash or sell some of their shares to meet the LVR requirements — sometimes in a very short space of time.

So using debt can amplify investment returns, but it’s also riskier.

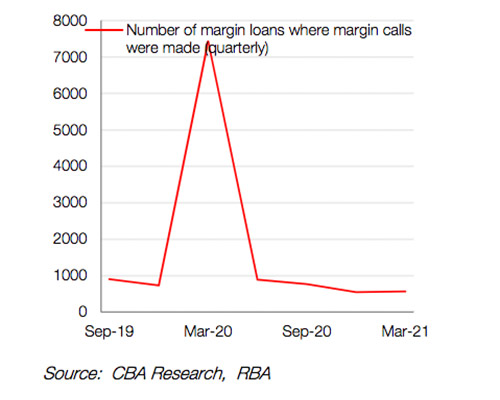

Whetton and Brown used the March 2020 market crash as an example of what happens when things go pear-shaped.

To use r/wallstreetbets parlance, traders using leverage pre-Covid “got wrekt”:

In a very short space of time, more than 7,000 margin loans got called, meaning traders had to pony up more cash to reduce their LVR.

If they couldn’t do it, some or all of they shares they bought using leverage would’ve been sold automatically.

The trader army

Since central banks turned the stimulus taps on and governments came to the party with fiscal firepower, post-Covid markets have been largely defined by a healthy dose of risk appetite.

Combined with stay-at-home orders and higher savings rates, “the army of day traders has grown strongly”, CBA said.

The increased margin loan activity has also been accompanied by a surge in new sign-ups to retail trading apps such as Commsec and Marketech.

While margin lending activity has ripped higher, strong gains on stock markets mean the underlying securities behind the loans have also risen sharply, CBA noted.

In one sense that creates a positive feedback loop, where traders can use their high asset balances as a basis to increase leverage and buy more stocks.

“This is a pretty positive wealth effect for spending, house purchases and superannuation balances,” Whetton and Brown said.

The chart above also shows an equally sharp rise in margin lending in 2019.

In the space of just 12 months before the COVID-19 crash, the amount of margin loans in Australia almost doubled — from $11bn to $19bn — after declining through the previous year.

That uptick in margin lending followed a key policy change from the US Fed, which started cutting rates after a big market correction in December 2018.

In response, the RBA also cut rates three times — from 1.5% to 0.75% — following an multi-year period of forward guidance where the bank projected that the next move in rates was likely to be up.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.