Via Getty

It’s crazy, but the Aussie deficit just got slashed to within an inch of a surplus

News

Via Getty

News

According to the Word of the Sublime Ruling Council of Marrickville – ie: the Australian Federal Government and its brand new Mid-Year Economic and Fiscal Outlook (MYEFO) – you can forget all the math of May’s annual Aussie Budget.

‘Cos that was all wrong.

This week the official number crunchers and message massagers revised the official budget deficit projections.

Revised down. Sharply down.

Kevin Costner’s katana blade in The Bodyguard sharp. And a glass of chardonnay in the hands of Whitney Houston down.

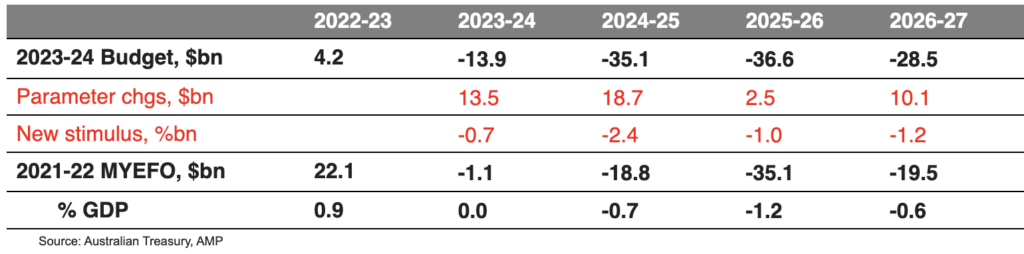

Basically, Treasurer Jim Chalmers and a thousand supporting accountants from Treasury said back in May that the deficit for this year would be $13.9bn.

A few months later and that deficit is just $1.1bn.

And while they warn structural pressures on spending remain (for a few years for sure) and are expected to steadily increase the rate of spending up as a share of GDP, one would suspect a budget surplus is already in the post.

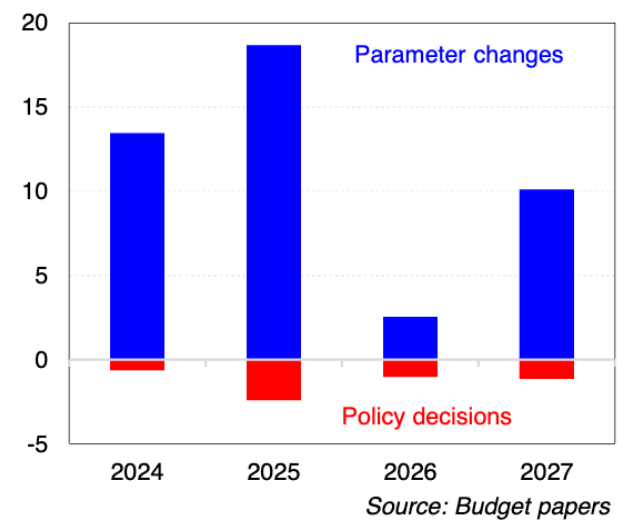

Stephen Halmarick at CBA says the cracking budget health flows mostly from a stronger economy, with parameter changes* accounting for $13.5bn of the improvement – while policy changes weakened the underlying cash balance by just $0.65bn.

And what’s more – there was not a single new, big ticket spending announcement in the MYEFO.

The government says it’s pumping 92% of all tax upgrades back into the MYEFO budget bottom line.

But Halmarick says forget the conservative estimates coming out of Treasury – CBA continue to expect that a surplus of ~$20bn (or 0.75% of GDP) will be achieved once the final budget outcome is received in the second half of 2024, provided there are no significant new policies announced.

*Ed: Parameter changes = savings

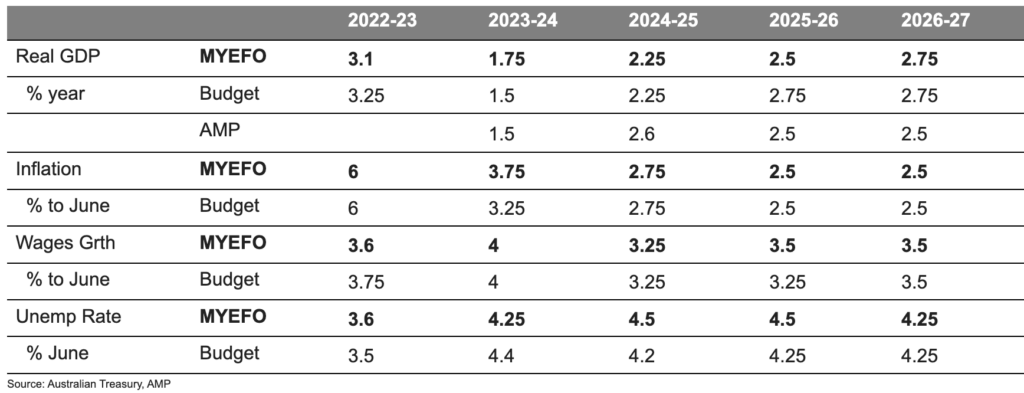

The Albo Government’s now forecasting slightly higher domestic growth as well as slightly higher inflation for this financial year, but – (though slightly lower than the Reserve Bank’s!)

For the more resilient-than-expected resources-driven Aussie economy, the Government’s forecasts aren’t too far off those made by the RBA in its latest cracking edition of the Statement of Monetary Policy – although Treasury now has unemployment peaking at 4.5% vs the RBA’s forecast peak of 4.25%.

On the inflation front the Government of His Majesty of Marrickville, PM Anthony Albanese, has upwardly revised its inflation forecast to about 0.25% below those of the RBA – reckoning inflation will drop below the 2-3% target by mid-2024 – which is six months earlier than the RBA is forecasting.

“If the Government is right it may justify a slightly lower profile for the cash rate and an earlier start to rate cuts than the RBA’s forecasts would imply, but there is not much in it,” says Dr Shane Oliver, head of investment strategy and chief economist at AMP.

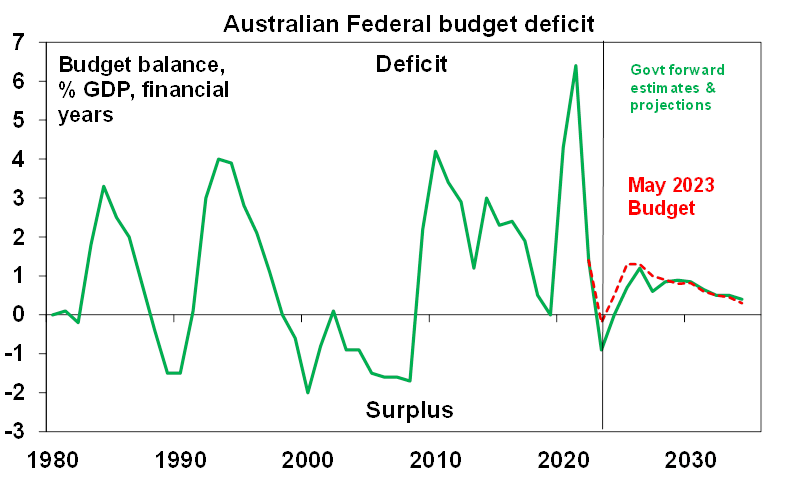

The Government is now projecting sharply lower budget deficits, with the deficit forecast to fall to $1.1bn this financial year from the Budget forecast of $13.9bn.

Right now, four months into the fiscal year the Aussie Budget is some $9bn ahead of where the last estimate expected to be back in May.

Now one need only a slide rule and a cursory understanding of politics to know this is all working out sublimely for both fans of the Government and of His Marrickvillian Majesty, the PM Albo.

The money, evidently, is pouring in and while no-one’s officially using the word surplus yet – that’d be against the under-promise/over-deliver thesis of the Treasurer – a slide rule and a cursory understanding of using it would show a surplus is a distinct possibility ahead of July next.

Dr Oliver says the circa $64bn in estimated higher tax company receipts over the four years to 2026-27 (due largely to higher commodity prices) as well as higher personal tax (due to stronger employment and ‘bracket creep’) along with a $7.4bn delay in infrastructure payments are what has driven the big dollars

As eagle-eyed readers will note on the next table, the greater portion of the savings* are being used to reduce the budget deficit with only $1-2bn a year in new spending.

(*Ed: called parameter changes)

Underlying cash budget balance projections

The Government’s move to overhaul the visa system to better control long term (mainly student and work) arrivals and hence total net overseas migration is good news, says Dr Oliver.

After all, net migration last year absolutely ran rampant, blowing out to an assumed record of (circa) well over half a million (from 180,000 expected).

That’s like the population of Canberra, except colourful.

The Gov reckons that as a result there’ll be circa 185,000 less arrivals over the next four years, but net migration is still likely to top 375,000 this financial year.

“Moving to get immigration under control is good news but it’s still above pre-covid average levels (which were around 230,000 a year) and will still be adding to the housing shortfall which we estimate to have been around 120,000 dwellings in June rising to around 180,000 by June next year.

“This is because underlying demand will continue to run above housing completions of around 170,000 dwellings a year.

“As a result, the supply shortfall will remain a source of underlying upwards pressure on rents and home prices, although an affordability constraint and high interest rates will likely dominate and push prices lower in the year ahead,” Dr Oliver adds.

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.