Closing Bell: Aussie stocks dive as big miners dig a great hole through Monday

Via Getty

- ASX slumps, dragged down by blue chips

- Materials sector plunges 2.5pc

- Small cap winners led by Bioxyne

This morning in Sydney the Aussie sharemarket quickly walked off last week’s new record high. And stayed there all day.

At 4.15pm on February 5, the S&P/ASX200 was down 73.5 points or 0.95% to 7,625.9.

All sectors were trading in the red at lunch, while ASX futures were down 0.7% at 8:30am, and that was the high point on Monday, after the ASX200 rode the interest rate optimism to climb more than 2% last week.

With the Reserve Bank of Australia regrouping on Tuesday for the country’s first monetary policy decision of 2024, local traders chose to take the points today, after being surprised by recent outsized gains.

The benchmark’s big names were at the heart of Monday’s broad based losses – the iron ore triumvirate and other major miners dragged the Materials sector to hefty Monday losses, down 2.2% in the early afternoon.

Iron ore prices collapsed by almost 4% since the previous session.

The other drivers of the wider retreat came from the big banks and the Energy sector.

Other than that, it’s a quick shout out to Appen (ASX:APX) where the stock has slumped to a new record low, in the wake of chief executive Armughan Ahmad’s surprise exit.

Appen’s been having a shocker for some months now – the share price melted following Google’s walk-away from its headline, megabucks contract with the tech giant.

Earlier, the ABS reported that the Aussie trade balance narrowed to $10.9 billion in December as imports kicked higher following a shock November retreat.

Gold and LNG led the demand-side for Aussie exports, which hit $11.8 billion in November.

In the states, US stocks recovered late on Friday to end significantly higher with some massive gains from Amazon and Meta following robust earnings reports.

The Dow rose 134 points or 1.2%, the S&P500 added 1.1% (both fresh highs) and the tech heavy Nasdaq soared 1.7%.

ASX Sectors on Monday

![]()

We’re watching oil…

WTI crude futures look like they’ve settled at around US$72 a barrel – which was needed after a tumultuous week that saw investors fear the worst for peace breaking out in the Middle East.

It didn’t.

Until prices steadied overnight, oil prices were in free fall, down more than 7% over the previous five sessions.

And regional markets…

Around the Asia-Pacific markets were mostly lower as the Japanese yen struck 2-month lows and the Hang Seng struggled early.

In Shanghai the benchmark Composite dropped almost 2% by lunchtime moving closer to an unwanted five year nadir under the weight of Beijing’s ongoing economic uncertainty which is pressing at the heart of market confidence.

Here’s the Shanghai and the Hong Kong markets over the last six months.

Meanwhile, in the States…

The S&P500 ended on Friday at its fourth straight record high, as Facebook-parent Meta’s 20% surge made CEO and Founder Mark Zuckerburg some $US28bn better off in a single day.

It surely was a big one for Meta, with a stock of that size jumping by one quarter in value almost unheard of… but not quite. Nvidia popped over 24% around this time last year.

So the Magnificent Seven has form on this.

Bond yields had driven equities post-COVID, but US earnings season became the new driving factor last week, no real surprise by the baton change on the stock level, but the moves have been extraordinary, propelling US indices higher.

The Nasdaq Composite gained 1.74%. This is another busy week of corporate earnings for markets, including results from McDonalds and Ford.

Fed Chair J Powell told US telly on Sunday that his crew at the FOMC will do nought but move with great care on rate cuts this year.

“We just want some more confidence before we take that very important step of beginning to cut interest rates,” he told 60 Minutes.

That may not’ve helped sentiment, although the state of trade in Asia today may’ve cast a further pall over Wall Street’s Monday morning.

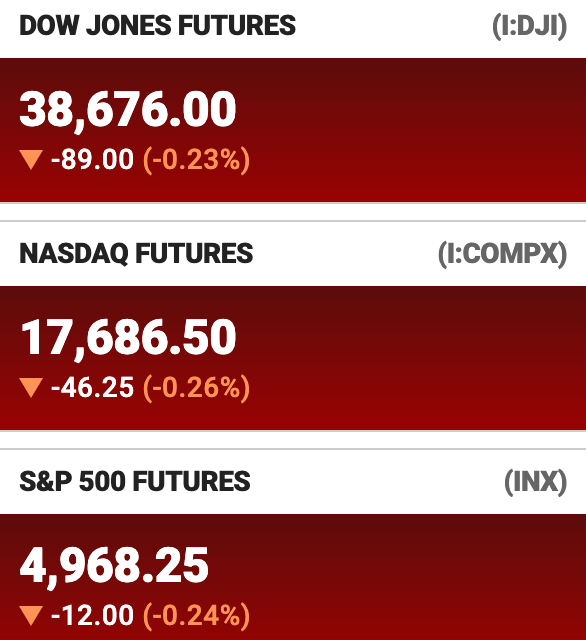

US Futures were lower in Sydney at 3.30pm on Monday.

ASX SMALL CAP LEADERS

Today’s best performing small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | MARKET CAP |

|---|---|---|---|---|---|

| TD1 | Tali Digital Limited | 0.0015 | 50% | 500,137 | $3,295,156 |

| CDT | Castle Minerals | 0.0085 | 42% | 16,628,324 | $7,346,958 |

| MTL | Mantle Minerals Ltd | 0.0035 | 40% | 23,534,162 | $15,493,615 |

| BRX | Belararox | 0.185 | 37% | 532,421 | $9,577,443 |

| BP8 | BPH Global Ltd | 0.002 | 33% | 3,115,961 | $2,753,345 |

| BXN | Bioxyne Ltd | 0.016 | 33% | 7,021,595 | $22,819,745 |

| MRD | Mount Ridley Mines | 0.002 | 33% | 1,585,990 | $11,677,324 |

| AMM | Armada Metals | 0.029 | 32% | 3,017 | $4,576,000 |

| GTE | Great Western Exploration | 0.0425 | 29% | 1,268,964 | $11,484,350 |

| MKG | Mako Gold | 0.023 | 28% | 28,230,989 | $11,923,369 |

| VML | Vital Metals Limited | 0.005 | 25% | 3,551,816 | $23,580,268 |

| 1TT | Thrive Tribe Tech | 0.016 | 23% | 109,375 | $3,856,080 |

| BPM | BPM Minerals | 0.14 | 22% | 500,434 | $7,719,055 |

| RDM | Red Metal Limited | 0.17 | 21% | 4,332,748 | $41,765,267 |

| EGR | Ecograf Limited | 0.15 | 20% | 1,093,942 | $56,753,977 |

| AHN | Athena Resources | 0.003 | 20% | 4,182,034 | $2,676,169 |

| ASR | Asra Minerals Ltd | 0.006 | 20% | 400,000 | $8,182,479 |

| CZN | Corazon Ltd | 0.012 | 20% | 429,800 | $6,155,979 |

| IEC | Intra Energy Corp | 0.003 | 20% | 700,000 | $4,151,954 |

| LNR | Lanthanein Resources | 0.006 | 20% | 5,436,674 | $6,449,060 |

| NRX | Noronex Limited | 0.012 | 20% | 1,311,700 | $3,783,018 |

| SER | Strategic Energy | 0.012 | 20% | 1,671,024 | $4,858,151 |

| TIG | Tigers Realm Coal | 0.006 | 20% | 500,000 | $65,333,512 |

| RHY | Rhythm Biosciences | 0.155 | 19% | 396,067 | $28,748,537 |

| 4DS | 4DS Memory Limited | 0.087 | 19% | 54,624,752 | $128,394,949 |

Winners and stuff – 05 Feb, 2024

WINNERS

The party was most definitely on at Bioxyne (ASX:BXN), after news that the company’s wholly-owned subsidiary, Breathe Life Sciences has been awarded a Good Manufacturing Practice (GMP) licence to manufacture medical cannabis. And psilocybin. And MDMA.

That’s huge news for Bioxyne, as the licence also allows Breathe Life Sciences to produce “final dose form capsules for supply to authorised prescribers and clinical trials”.

No doubt the company is now in the process of heavily fortifying its headquarters, ahead of the arrival of hordes of zombie-like hippies, armed with bongo drums and terrible BO, to surround the building and demanding to speak to “the man” about “some stuff”.

Battery anode business Ecograf (ASX:EGR) surged 36%, despite not having anything of interest to tell the market – and I’m not entirely sure why. I’ll try and find out, but don’t hold your breath waiting for an answer just yet.

And a couple of the smaller goldies, namely Belarox and Great Western Exploration saw significant post-lunch surges despite a lack of fresh announcements as well.

Red Metal continued its recent success, moving 21.5% higher on last week’s news of outstanding leach results received from initial metallurgical testing at the Company’s new Sybella discovery.

Last week’s high-flyer Mako Gold (ASX:MKG) was at it again, rising another 16.6% after delivering a presentation to the 121/Mining Indaba Conference in Cape Town, South Africa.

The prezzo didn’t contain any salient information that the market didn’t already know about, by the looks of things – but it does tie up all of Mako’s recent great news in a pretty format, so there’s that.

ASX SMALL CAP LAGGARDS

Today’s best performing small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | MARKET CAP |

|---|---|---|---|---|---|

| YOJDA | Yojee Limited | 0.027 | -40% | 2,275 | $7,636,629 |

| BCT | Bluechiip Limited | 0.008 | -38% | 9,638,231 | $10,339,859 |

| EMU | EMU NL | 0.001 | -33% | 2,569,981 | $3,037,157 |

| MCT | Metalicity Limited | 0.002 | -33% | 54,800 | $13,455,161 |

| EPX | EPT Global Limited | 0.021 | -33% | 1,449,207 | $13,880,803 |

| ADY | Admiralty Resources | 0.007 | -30% | 4,400 | $13,035,792 |

| SHO | Sportshero Ltd | 0.01 | -29% | 1,623,916 | $8,649,660 |

| KNB | Koonenberry Gold | 0.03 | -27% | 1,260,044 | $4,909,713 |

| RBX | Resource B | 0.056 | -25% | 376,250 | $6,201,336 |

| AL8 | Alderan Resource Ltd | 0.003 | -25% | 1,374,303 | $4,427,445 |

| DCX | Discovex Res Ltd | 0.0015 | -25% | 44,366 | $6,605,136 |

| TOY | Toys R Us | 0.006 | -25% | 1,768,234 | $7,859,708 |

| SUH | Southern Hemisphere Mining | 0.0355 | -24% | 605,142 | $27,753,796 |

| IS3 | I Synergy Group Ltd | 0.007 | -22% | 1,782,472 | $2,736,723 |

| NRZ | Neurizer Ltd | 0.007 | -22% | 3,469,494 | $12,682,761 |

| TTI | Traffic Technologies | 0.007 | -22% | 505,862 | $6,819,032 |

| SVL | Silver Mines Limited | 0.135 | -21% | 11,127,954 | $238,736,464 |

| QXR | Qx Resources Limited | 0.012 | -20% | 456,383 | $16,651,168 |

| IVX | Invion Ltd | 0.004 | -20% | 238,558 | $32,122,661 |

| ROG | Red Sky Energy | 0.004 | -20% | 202,809 | $26,511,136 |

| XST | Xstate Resources | 0.016 | -20% | 77,011 | $6,430,383 |

| YAR | Yari Minerals Ltd | 0.008 | -20% | 3,187,682 | $4,823,578 |

| MSG | Mcs Services Limited | 0.013 | -19% | 2,905,146 | $3,169,594 |

| NPM | Newpeak Metals | 0.018 | -18% | 169,851 | $2,198,938 |

| PLN | Pioneer Lithium | 0.135 | -18% | 43,611 | $4,690,125 |

In Case You Missed It

Maiden drilling within Viridis Mining and Minerals’ Fazenda mining licence in Brazil has uncovered a major high-grade zone and eye-popping intersections of up to 23,556ppm (2.36%) TREO.

Marmota has reported that two distinct, largely untested uranium bearing formations requiring follow-up drilling have been identified at the Bridget prospect, outside the known 5.4 Mlbs Junction Dam project in South Australia.

Firetail has reported that the company has pulled up significant copper, silver lead and zinc in its very first hole at Cumbre Coya, part of the Picha project in Peru.

Manuka has secured firm commitments from several new and existing sophisticated investors that will see it boost the coffers by an initial $2.5m and increase it further via a $2.5m debt conversion.

Anson Resources has received the green light to start resource drilling at its Green River lithium brines project in Utah’s Paradox Basin, with a conceptual exploration target of between 2Bt and 2.6Bt of brines grading 100ppm to 150ppm lithium and 2,000ppm to 3,000ppm bromine.

Sunshine Metals says that it has resumed drilling at the Liontown prospect in north Queensland to test extensions to the 17m intersection grading 22g/t gold that the company announced in November last year.

Future Battery Minerals (ASX:FBM) says that maiden metallurgical testwork program on mineralised material from the Big Red pegmatite within the Kangaroo Hills Lithium Project (KHLP) in WA’s Goldfields shows that it is amenable to conventional Dense Media Separation (DMS) and Froth Flotation separation techniques.

Silver Mines has kickstarted its development plans for 2024 and beyond with an oversubscribed $8 million placement which will be backed up by a $2 million share purchase plan for new and existing institutional, professional and sophisticated investors.

Pantera Metals has announced that its Superbird project acreage position – located on Exxon Mobil’s literal Smackover doorstep – has been expanded by 11% with 13,457 acres now leased within an exclusive abstract area of 50,000 acres.

GCX Metals’ maiden drill program at the Dante project, located in WA’s 140,000km2 West Musgrave region, has been brought forward and expanded following the confirmation of several additional drill targets.

TRADING HALTS

Reward Minerals (ASX:RWD) – pending the release of an announcement in relation to its proposed acquisition of the Beyondie Project and associated entitlement offer.

Indiana Resources (ASX:IDA) – pending an announcement to the market in relation to a decision from the ICSID ad hoc Committee concerning the Claimants’ preliminary objections to the United Republic of Tanzania’s application for annulment of the Award pursuant to ICSID Arbitration Rule 41(5).

Kalamazoo Resources (ASX:KZR) – pending the release of an announcement pertaining to a material corporate transaction in relation to the disposal of the Ashburton Gold Project.

Anagenics (ASX:AN1) – pending the release of an ASX announcement regarding a proposed capital raise.

Flexiroam (ASX:FRX) – pending the release of an announcement in relation to a capital raising.

Locality Planning Energy (ASX:LPE) – pending the release of an announcement in relation to a board restructure.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.