Closing Bell: ASX gains trimmed by deflating Chinese data, however it’s Kristmas at Krakatoa with thick peggies for all

Via Getty

- The ASX has closed higher

- Healthcare leads sector gains

- Small caps led by KTA and FG1

The Aussie sharemarket has trimmed the fat off this morning’s substantial gains – at one stage there we were easing past the 7,350 mark and off to the races.

But the big races have been run this week and some selling this afternoon, as well as some shonky data around Chinese domestic demand, has punched a bit of a hole through those plans.

Still, like sands through the hourglass, these are the gains of our lives…

At match out on Thursday November 9, the S&P/ASX 200 (XJO) index was about 20 points, or +0.28 higher at 7,015.

It’s been a session dominated by company news.

At the top end of town, some truth-telling form National Australia Bank (ASX:NAB) CEO Ross McEwen has taken the puff out of an otherwise happy FY23 report where NAB hoisted its cash net profit by 8.8% to $7.7 billion – way out ahead of analyst expectations.

Despite the favourable world of being a Big Bank in Australia, the chief executive thought it a good time to say things might not stay good.

“Growth is slowing, competitive and inflationary pressures are elevated and asset quality is deteriorating,” McEwan warned shareholders… who were still doing the math on their final dividend, after it was also hoisted (by +7.7%) to 84 cents a pop.

NAB FY23 short cuts:

· Net interest income is up 13.3% to $16.8bn, in line with expectations

· Cash earnings up 8.8% to $7.7bn vs $7.3bn expected

· Final dividend up 7.7% to 84 cents per share Full-year dividend up 16% to $1.67 per share vs. $1.68 expected

· Cash payout ratio down 70 bps to 67.7%

· Net interest margin of 1.74%, in line with expectations

· Operating expenses up 7.8% to $9.38 billion

· Credit impairment charges of $802m vs $922 million expected

At the lower end of town – in the Aussie automotive aftermarket sector to be exact – RPM Automotive (ASX:RPM) dropped a decent trading update, which offers some handy context for the local retail environment heading into Christmas.

The first quarter for RPM has been a winner – revenues are up 5.5% to circa$25mn and despite challenging trading conditions, has lifted its improved contribution margin to 34.5%.

CEO Clive Finklestein says a focus on ‘execution to create greater operational efficiency combined with margin growth’ has significantly improved profitability and brought some stability to the business.

“Margin growth was also supported by enhanced operating leverage due to increased scale and cross-sell opportunities, development of the retail and wholesale network, product diversification and warehouse expansion.”

The stock was up about 10% at 3PM in Sydney, after it reaffirmed FY24 guidance – expecting reported revenue between $130mn to $140mn and EBITDA between $10.5 to $12mn.

RPMs Q1 shortcut:

· Continued revenue growth with underlying revenue in Q1 FY24 of $24.9m, up 5.5% on prior corresponding period (pcp), despite challenging trading conditions, and reported revenue of $28.4 million, flat on pcp which included discontinued businesses

· Contribution margin improved to 34.1% (Q4 FY23 28.8%) driven by growing scale, a focus on operational optimisation and disciplined cost management

· Wholesale tyre division strengthened with the strategically aligned acquisition of Chapel Corner Tyres

· Cost benefits from restructure now flowing through, with around half of expected $1.5 million in annualised savings now implemented, primarily in the Repairs and Roadside division

· Disposed non-core assets, expected to generate an additional $1.4 million in cash across 2H FY23 and 1H FY24, and $0.5 million annual improvement in EBITDA to $3.0m Q1 FY24 v $2.5m Q1 FY23 (10.6% of revenue vs 9.2% pcp)

· Improved inventory management growing cashflow: Increased inventory turns resulting in growing cash balance of $5.8m at 30 September 2023

ASX Sectors on Thursday

Ripped from the headlines

We’re watching gold

At least I am. It’s soothing to watch it swing.

The gold price is steeling itself without any sense of resolve from my POV for a march on $1,950. That my friends is its lowest levels in three weeks, just as our equity markets hit their three-week apex.

Gold’s being hit by a bit of a risk-on mise en scène, with newly hawkish Fedspeak out of Minneapolis, where president Neel Kashkari said hold the horses USA, it’s way too soon to George W Bush this war and declare victory over inflation. Meanwhile, it seems the influential Irish central bank’s top paddy Gabriel Makhlouf reckons further tightening of the taps is an option.

But largely gold is weaker because things look stronger. And – as I recently heard someone, somewhere say – the “geopolitical risk premium” vis-a-vis the Israel-Hamas war is lower… for the moment.

What’s happening in China?

The price of pork has had a little of the collapse about it, declining at a far steeper pace (-30.1% vs -22.0%) than expected last month, a worrying sign that all is not what it should be in Chinese markets.

China is the only country with state-controlled “Pork Reserves”, so the price of a pig can say a great deal about domestic demand and official controls.

It’s not the end of the world, but it is another backward step for the Middle Kingdom says eToro market analyst Josh Gilbert after both consumer and producer prices in China both had the look of deflation about them.

In Hong Kong, the Hang Seng has given up more than 80 points – circa -0.5% – by lunchtime, making it a third straight session of morning retreats.

Official data out of Beijing indicates China might well be dancing with deflation again. Mainland (CPI) consumer prices fell to their lowest levels in 24 months. Meanwhile, the mainland’s producer prices (PPI) shrank for a 13th consecutive read, down in October by 2.6% vs forecasts of a 2.7% drop.

Josh told Stockhead Beijing’s latest fiddly attempts at stimulus are one foot forward, but not enough to lift benign domestic demand.

“We’ve seen the worst… but China’s recovery will take time. These challenges may be something investors simply have to accept in the months ahead as it won’t be all one way,” Josh says.

“China has committed to ensuring it doesn’t see a further growth slowdown, so more support from Beijing in the form of additional stimulus measures may be on the cards.”

TODAY’S ASX SMALL CAP LEADERS

Here are the best performing ASX small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | Market Cap |

|---|---|---|---|---|---|

| MGTR | Magnetite Mines | 0.01 | 233% | 185,908 | $62,808 |

| MTH | Mithril Resources | 0.002 | 100% | 1,994,907 | $3,368,804 |

| KTA | Krakatoa Resources | 0.043 | 65% | 150,541,212 | $11,307,346 |

| BP8 | Bph Global Ltd | 0.0015 | 50% | 1,256,492 | $1,615,563 |

| FG1 | Flynngold | 0.097 | 43% | 5,746,710 | $9,274,016 |

| ACM | Aus Critical Mineral | 0.385 | 43% | 1,592,421 | $8,027,438 |

| IMU | Imugene Limited | 0.11 | 36% | 269,666,019 | $580,362,964 |

| AHN | Athena Resources | 0.004 | 33% | 750,750 | $3,211,403 |

| BYH | Bryah Resources Ltd | 0.016 | 33% | 727,157 | $4,303,263 |

| CT1 | Constellation Tech | 0.004 | 33% | 246,667 | $4,413,601 |

| PNX | PNX Metals Limited | 0.004 | 33% | 568,706 | $16,141,874 |

| SQX | SQX Resources Ltd | 0.135 | 29% | 100,476 | $2,625,000 |

| RDN | Raiden Resources Ltd | 0.05 | 28% | 215,081,321 | $91,098,742 |

| ZNC | Zenith Minerals Ltd | 0.165 | 27% | 1,050,587 | $45,809,515 |

| EDE | Eden Inv Ltd | 0.0025 | 25% | 137,094 | $6,727,274 |

| EMP | Emperor Energy Ltd | 0.01 | 25% | 981,258 | $2,150,900 |

| IEC | Intra Energy Corp | 0.005 | 25% | 14,213,429 | $6,643,126 |

| KPO | Kalina Power Limited | 0.005 | 25% | 4,710,713 | $6,060,783 |

| MCT | Metalicity Limited | 0.0025 | 25% | 2,690,569 | $8,502,172 |

| RIE | Riedel Resources Ltd | 0.005 | 25% | 1,499,410 | $8,237,628 |

| TEM | Tempest Minerals | 0.01 | 25% | 1,732,048 | $4,091,068 |

| PIM | Pinnacleminerals | 0.29 | 23% | 2,926,116 | $6,010,125 |

| EFE | Eastern Resources | 0.011 | 22% | 46,056,251 | $11,177,518 |

| AS2 | Askarimetalslimited | 0.17 | 21% | 298,043 | $10,752,030 |

| BMM | Balkanminingandmin | 0.145 | 21% | 348,900 | $8,256,861 |

The only company holding a kandle to Krakatoa today is Flynn Gold, which was earlier pulled up by the ASX speed cops – and this is why:

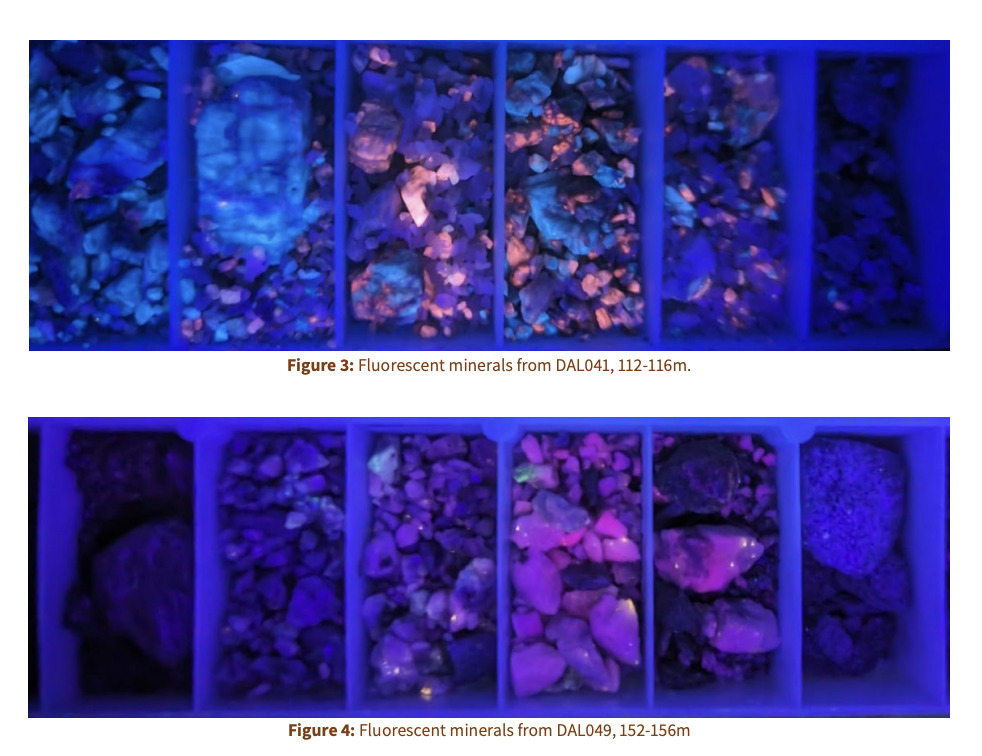

OFC no one can kompare to Krakatoa Resources (ASX:KTA) which is up about, oh, a million pc after RC drilling beneath high grade Li20 rock samples is all done at King Tamba in WA’s Mid-West, with the program expanded after discovery of up to 39m thick pegmatite under the 4.3% Li20 rock chip at Wilsons prospect.

Thick pegmatites. Juicy.

The drilling program has been heartily expanded, too, following the discovery, with KTA saying 13 of the 16 drill holes intersected pegmatites with consistent intersections of flat-lying pegmatite logged from 70m vertical depth.

More exciting, several samples fluoresced orange-pink under shortwave UV light:

Up almost +30% at the close, Raiden Resources (ASX:RDN), one of the top ASX stocks of 2023 with +952% YTD gains, has again tapped into some more pegmatite action at its Andover South tenements in the Pilbara.

Assay results have come in from recent rock chip sampling, and “continue to indicate high potential for significant and mineralised Lithium-Tantalum-Caesium (LCT) pegmatites”.

In fact, the latest sampling yields the highest grade lithium result (3.80% Li2O) defined to date from Andover South.

And further X-Ray Diffraction (XRD) analysis confirms spodumene as the dominant lithium mineral in the sampling.

Raiden MD Dusko Ljubojevic:

“While the high-grade results from Andover South continues to impress us, we are particularly excited by the definition of further mineralised pegmatites on the western periphery of the high-grade trend we have defined to date.

“The western anomalies are reporting the highest grades defined to date and are characterised by multiple pegmatites.”

Meanwhile, Impact Minerals (ASX:IPT) has announced “outstanding economics” from a scoping study showing its Lake Hope project in WA to potentially be the lowest-cost producer of high purity alumina (HPA) globally.

And clinical stage immuno-oncology small cap Imugene (ASX:IMU), run by MD Leslie Chong, has been developing a portfolio of innovative new treatments for that spectacular global growth market called cancer.

The stock jumped earlier this week, after IMU dropped a promising clinical trial update of its Phase 1 MAST (Metastatic Advanced Solid Tumours) trial evaluating the safety and efficacy of novel cancer-killing virus CF33-hNIS (VAXINIA).

OD6 Metals (ASX:OD6), has given back a little after gaining strongly in the AM, on the back of phase 3 drilling at its Splinter Rock clay hosted REE project in WA have returned grades of up to 6,441ppm TREO with extensive clay thickness up to 77m at high grades and 77% of holes returned grades >1,000ppm TREO.

TODAY’S ASX SMALL CAP LAGGARDS

Here are the least performing ASX small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | Market Cap |

|---|---|---|---|---|---|

| NRZR | Neurizer Ltd | 0.001 | -80% | 10,509,328 | $638,370 |

| CLE | Cyclone Metals | 0.001 | -50% | 21,165,123 | $20,529,010 |

| TWER | Treasury Wine Estate | 0.635 | -35% | 197,232 | $74,094,469 |

| AKM | Aspire Mining Ltd | 0.061 | -26% | 244,327 | $41,626,233 |

| NRX | Noronex Limited | 0.009 | -25% | 983,533 | $4,539,621 |

| ICG | Inca Minerals Ltd | 0.016 | -24% | 525,644 | $10,340,395 |

| SIX | Sprintex Ltd | 0.01 | -23% | 2,061,245 | $4,406,974 |

| 14D | 1414 Degrees Limited | 0.025 | -22% | 521,655 | $7,621,393 |

| TG6 | Tgmetalslimited | 0.865 | -21% | 9,349,127 | $44,331,695 |

| GBZ | GBM Rsources Ltd | 0.015 | -21% | 4,280,449 | $11,786,114 |

| KZA | Kazia Therapeutics | 0.087 | -21% | 2,428,685 | $25,998,431 |

| FAU | First Au Ltd | 0.002 | -20% | 1,060,801 | $3,629,983 |

| GTG | Genetic Technologies | 0.002 | -20% | 495,209 | $28,854,145 |

| MRQ | Mrg Metals Limited | 0.002 | -20% | 1,754,565 | $5,514,797 |

| TMX | Terrain Minerals | 0.004 | -20% | 15,010,360 | $6,767,139 |

| TSL | Titanium Sands Ltd | 0.008 | -20% | 499,666 | $17,718,047 |

| YPB | YPB Group Ltd | 0.002 | -20% | 2,695,045 | $1,951,154 |

| OKJ | Oakajee Corp Ltd | 0.022 | -19% | 25,000 | $2,469,043 |

| NIS | Nickelsearch | 0.098 | -18% | 17,604,973 | $19,235,679 |

| R3D | R3D Resources Ltd | 0.049 | -18% | 75,494 | $8,889,095 |

| MHK | Metalhawk. | 0.195 | -17% | 664,060 | $18,511,188 |

| MPG | Manypeaksgoldlimited | 0.22 | -17% | 14,000 | $9,639,238 |

| FGL | Frugl Group Limited | 0.01 | -17% | 205,700 | $11,472,744 |

| H2G | Greenhy2 Limited | 0.01 | -17% | 33,793 | $5,025,070 |

| MEL | Metgasco Ltd | 0.01 | -17% | 113,870 | $12,766,641 |

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.