"... are you certain this gas leak's not going to be a problem, Mission Control?" Pic via Getty Images.

ASX Small Caps Lunch Wrap: Who’s blasting a leaky Boeing rocket into space next week?

News

"... are you certain this gas leak's not going to be a problem, Mission Control?" Pic via Getty Images.

News

Local markets were down again this morning, with the benchmark dropping sharply at open to be around -0.75% at lunchtime, as the market digested some unpleasant news from the ABS about the Consumer Price Index.

Short version of events: it’s moving in the wrong direction, so no rate cuts for you – and the market has reacted in a predictable fashion, throwing all the toys out of the cot and pouting like someone just told Mick Jagger “no!” for the first time in his life.

There’s more to it, of course, but first, we need to make a quick stop at Cape Canaveral Space Force Station in Florida, where a couple of astronauts are getting ready to really earn their paycheque next week, by being shot into space to rendezvous with the ISS and spend an extended period in zero gravity doing science stuff.

It’s all fairly standard stuff for astronauts Suni Williams and the improbably-named Butch Wilmore, except for a few key details – for starters, the rocket they’re getting ready to blast off in is one that’s been built by embattled airliner manufacturer Boeing.

That on its own should be enough to give just about anyone with a functional set of eyes slight pause, as Boeing has been in the news repeatedly over the past couple of months, largely because bits of their planes keep falling off.

Oh, and whistleblowers keep coming forward and then mysteriously dying. Not quite as mysteriously as the ponderously massive number of Russian oil company heavyweights that have been “falling out of windows” for the past few years… but still enough that it’s newsworthy enough to warrant a mention.

And… there’s one more thing that will no doubt be causing a number of puckering butts around Cape Canaveral in the lead up to the flight – the Boeing Starliner rocket has a helium leak, which Boeing engineers have labelled as a “nah, she’ll be right” level crisis.

The issue is broadly similar to the reaon why I have more half-built, very expensive Lego sets sitting in a cupboard in my home, destined to never be completed.

The leak is coming from a seal that is “about the size of a shirt button”, but it’s buried so deep inside the Boeing Starliner’s construction that it’s going to take weeks, and teams of people, to pull the whole thing apart to fix – and, in true Boeing style, ain’t nobody got time for that.

The technicians are making all the right noises, though, saying stuff like “we can handle this particular leak if that leak rate were to grow even up to 100 times.”

That’s according to Steve Stich, manager of NASA’s Commercial Crew Program, who pointed out that the leak only impacts one of a set of 28 thrusters “used to control the spaceship’s attitude”, which I can only assume is stuck on “petulant” and in dire need of adjustment.

So, Suni and Butch are gearing up for their launch next week, knowing that the hydrogen leak is there – and no one’s prepared for the time or the expense to fix it before the engines roar into life and the two hapless passengers up the pointy end are fervently praying that the leak isn’t going to end with one to the spacecraft doors landing in someone’s garden halfway across the country.

So to them, I say “Godspeed, you magnificent bastards”, and to the rest of you, I say “now might be a fabulous time to dump your Boeing shares, because this moonshot’s got the faint whiff of disaster about it already.”

Local markets have fallen on Tuesday morning, and that’s got quite a lot to do with the bean counters at the Australian Bureau of Spreadsheets (ABS), which delivered some unwelcome – but not unexpected – news this morning about inflation.

Turns out, the Consumer Price Index is being a stubborn little toddler, coming in at 3.6% for the year to April and making a mockery of everyone who has been banging the drum for short term interest rate relief.

The more concerning element is that the CPI index is still growing, month to month, despite all the “lever pulling” and “hand wringing” the RBA Board says it’s been doing for the past nine months.

CPI was 3.4% in February, 3.5% in March and now it’s at 3.6% in April – clearly going the wrong way, and clearly not adding fuel to the fire underneath hopes of a rate cut any time soon.

The main culprits driving it higher are all the things that The Average Australian™ has been quite justifiably pissing and moaning about for months… housing (+4.9%), food and non-alcoholic beverages (+3.8%), ) and transport (+4.2%) and alcohol and tobacco (+6.5%).

Obviously, the last thing on the list there isn’t exactly an “essential” (for most people, that is… they’re seriously essential for some of us), but with rents spiralling out of control in most capital cities and fuel prices regularly on the wrong side of $2.10 per litre, it’s becoming increasingly evident that somebody needs to do something.

Don’t look at me, though. I’m not in charge.

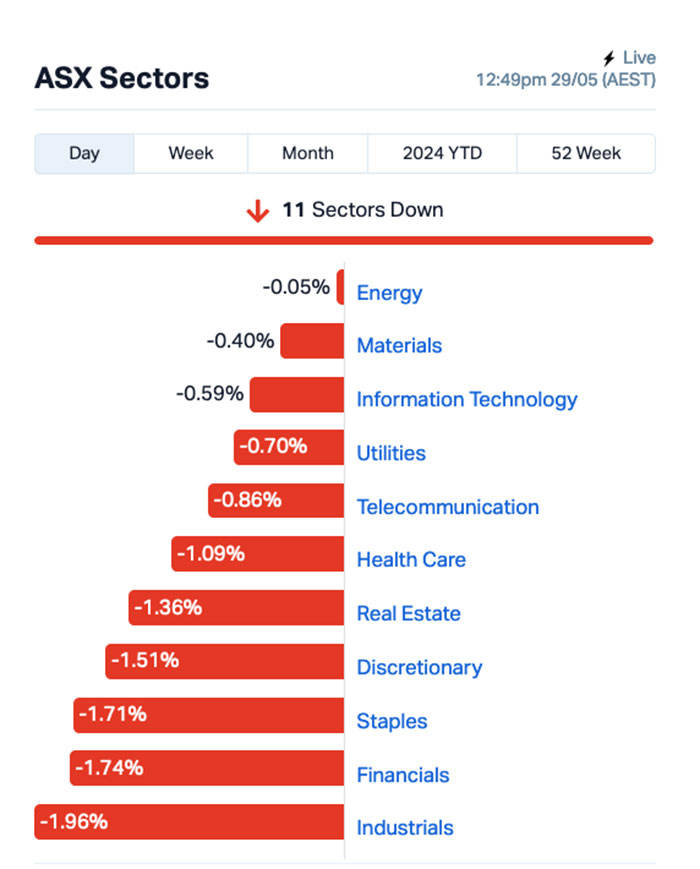

Anyhoo… a look at the ASX sectors at lunchtime showed that things are grim all over:

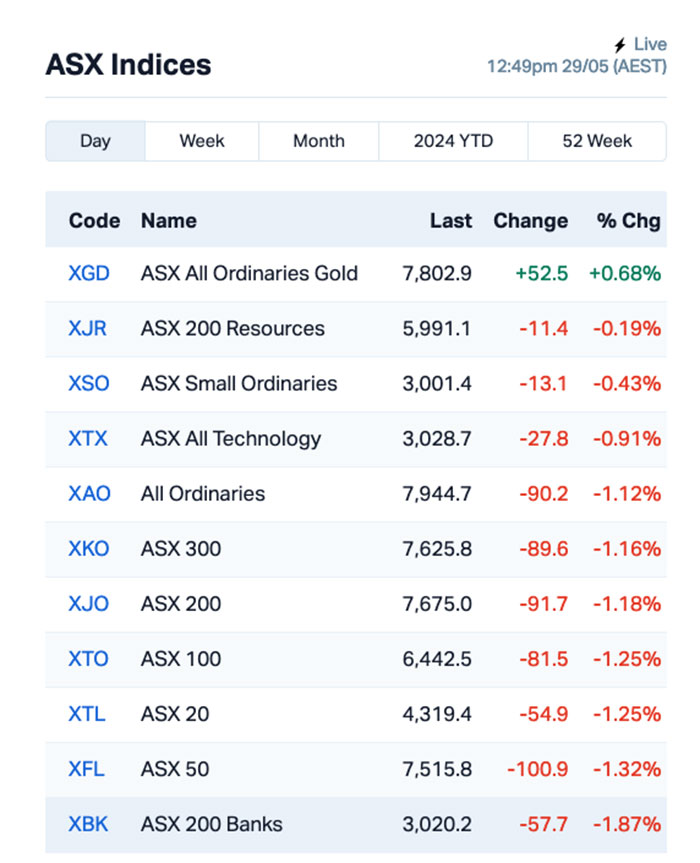

And the ASX indices are saying exactly what you thought they’d be saying – everything’s a bit crap, but safe haven goldies are still making bank.

Try not to fret too much, though – things are being weird everywhere else as well.

Overnight, the S&P 500 closed flat, the blue chips Dow Jones index was down -0.55%, but the tech-heavy Nasdaq surged by +0.59% to yet another all-time high, as US inventors wandered groggily back to work after a hard day on the cans “remembering the fallen troops”.

Nvidia led the tech rally as it jumped +7% on no specific news. The AI chipmaker’s market cap is now just a mere, teensy tiny US$100 billion short of surpassing Apple’s total worth.

Wagering stocks took a dip after the Illinois Senate passed legislation that would raise taxes on sports betting. Flutter Entertainment, a company that offers a diverse set of sports betting, iGaming, and online racing, fell -7% on the news – more than enough to beat the spread for anyone shorting the stock.

GameStop Corp surged +25% after announcing that it managed to raise almost US$1 billion from a share sale program amid renewed interest for the meme stock, baffling observers watching from the sidelines and wondering just how many stakes nerd to be hammered through Gamestop’s heart before it stops breathing.

BHP shares on the NYSE were flat after rumours swirled that the company is likely to request more time to finalise a deal with Anglo American. BHP has until 5pm in London today to make a new offer to Anglo after its previous three were rejected, while Anglo is no doubt gossiping to its friends about how BHP “just won’t take the hint”.

Word on the street is that BHP is gearing up to turn up to Anglo’s front yard, and is prepared to stand there all night, holding a boombox over its head and blasting Peter Gabriel at staggering volumes until Anglo relents and says yes.

Meanwhile, oil-related stocks will be in focus today as crude prices rose by 2% due to increased tensions in the Middle East following an attack on a vessel in the Red Sea and Israeli tanks reaching the centre of Rafah.

In Asian markets this morning, Japan’s Nikkei (-0.45%) and Hong Kong’s Hang Seng (-1.36%) are behaving as expected, while Shanghai markets (+0.28%) are once again just going their own way, without a care in the world.

There’s a lesson in there for all of us, probably… it’s either that one about dancing like nobody’s watching, or something about “making your own rules and controlling your own destiny” – or maybe Shanghai’s just got an army of investors standing out the front with boomboxes, with the persuasive sounds of Peter Gabriel driving the benchmark up through sheer force of will.

I guess we’ll never know…

Here are the best performing ASX small cap stocks for 29 May [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Name Price % Change Volume Market Cap DES Desoto Resources 0.115 51% 7,690,699 $4,554,414 8IH 8I Holdings Ltd 0.015 50% 96,064 $3,573,560 APC Australian Potash Ltd 0.0015 50% 56,094 $4,020,189 CNJ Conico Ltd 0.0015 50% 26,500 $1,805,095 BP8DD BPH Global Ltd 0.004 33% 716,893 $1,172,470 OAR OAR Resources Ltd 0.002 33% 7,121,741 $4,729,966 OLY Olympio Metals Ltd 0.047 31% 19,483 $3,077,153 COV Cleo Diagnostics 0.215 26% 802,254 $12,597,000 BDX BCAL Diagnostics 0.175 25% 922,247 $35,321,260 IVX Invion Ltd 0.005 25% 56,568 $25,698,129 PUR Pursuit Minerals 0.005 25% 4,566,667 $11,775,886 SQX SQX Resources Ltd 0.12 24% 319,576 $2,425,000 CLA Celsius Resource Ltd 0.011 22% 431,774 $21,851,215 LRL Labyrinth Resources 0.006 20% 100,000 $5,937,719 PRX Prodigy Gold NL 0.003 20% 3,000,982 $5,294,436 BEZ Besra Gold Inc 0.105 18% 2,223,974 $37,210,981 ASQ Australian Silica 0.04 18% 87,700 $9,583,253 DY6 DY6 Metals 0.14 17% 2,271,268 $4,849,300 GTR Gti Energy Ltd 0.007 17% 2,739,159 $12,299,683 HYD Hydrix Limited 0.014 17% 358,517 $3,050,626 POS Poseidon Nick Ltd 0.007 17% 295,343 $22,281,209 TMX Terrain Minerals 0.0035 17% 152,488 $4,295,012 TX3 Trinex Minerals Ltd 0.0035 17% 4,125,511 $5,485,957 KP2 Kore Potash PLC 0.036 16% 5,012,312 $20,406,200 RC1 Redcastle Resources 0.029 16% 988,990 $8,207,104

Winning on Wednesday morning was Desoto Resources (ASX:DES), soaring early on news that the company is all set to buy a rare earths project in the Northern Territory called Spectrum, where previous drilling pulled up a highlight 6m @ 6.55% total rare earths (TREO) from 248m.

The details are as follows: DeSoto has signed a binding term sheet to acquire 70% of Copperoz’ Spectrum REE project via a two stage minimum exploration spend of $5m over the next 39 months, with a right to acquire up to 100% of the project.

During the first 15 months, DeSoto agrees to spend a minimum of $2m, including a minimum 3500m worth of RC/DD drilling, while Stage 2 requires a minimum $3m expenditure during the following 24 months, and upon completion of a positive feasibility study, DeSoto has an option to buy out the remaining 30%.

Oar Resources (ASX:OAR) was also rising nicely on news that it has increased its uranium exploration ground by 283% to 880km2 in the Brazilian states of Rio Grande Do Sul and Goiás.

Cleo Diagnostic’s (ASX:COV) made gains after revealing that its ovarian cancer blood test outperforms the current clinical benchmark, correctly detecting 90% of early-stage cancers compared to only 50% using standard workflows.

And Pursuit Minerals (ASX:PUR) was celebrating some early success, with results from Drill Hole 1 at its Maria Magdelena tenement in the Rio Grande Sur project delivering “significant high grade intercepts of lithium brine at shallow depths of ~131m”.

Here are the most-worst performing ASX small cap stocks for 28 May [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap TKL Traka Resources 0.001 -33% 322,518 $2,625,988 AVE Avecho Biotech Ltd 0.003 -25% 220,000 $12,677,188 SFG Seafarms Group Ltd 0.003 -25% 20,000 $19,346,397 XGL Xamble Group Limited 0.023 -23% 987,000 $8,884,713 VN8 Vonex Limited 0.018 -20% 493,685 $8,141,144 AIV Activex Limited 0.004 -20% 9,822 $1,077,513 EMU EMU NL 0.029 -19% 304,908 $2,429,747 EOF Ecofibre Limited 0.063 -17% 55,032 $28,794,417 PNT Panther Metals 0.049 -17% 301,768 $5,142,804 1MC Morella Corporation 0.0025 -17% 3,094,297 $18,536,398 88E 88 Energy Ltd 0.0025 -17% 2,726,709 $86,678,016 BXN Bioxyne Ltd 0.005 -17% 658,481 $12,279,872 MTL Mantle Minerals Ltd 0.0025 -17% 1,350,000 $18,592,338 LM1 Leeuwin Metals Ltd 0.063 -16% 35,261 $3,513,875 AAU Antilles Gold Ltd 0.006 -14% 251,462 $6,975,745 AQX Alice Queen Ltd 0.006 -14% 20,000 $4,836,930 CMB Cambium Bio Limited 0.006 -14% 16,000 $5,362,646 MCL Mighty Craft Ltd 0.006 -14% 48,950 $2,582,365 TSL Titanium Sands Ltd 0.006 -14% 4,573,706 $15,482,230 VAR Variscan Mines Ltd 0.006 -14% 31,842 $2,653,003 MLM Metallica Minerals 0.02 -13% 500,000 $22,078,250 HLX Helix Resources 0.0035 -13% 2,500,000 $13,056,775 IS3 I Synergy Group Ltd 0.007 -13% 277,778 $2,832,643 PRM Prominence Energy 0.007 -13% 1,253,674 $2,491,011 RNE Renu Energy Ltd 0.007 -13% 2,031 $5,809,072

Belararox’s (ASX:BRX) 3D interpretation of assay results from samples collected at the Malambo prospect within its Toro-Malambo-Tambo project, have confirmed porphyry-style targets similar to deposits at globally recognised copper mining operations.

CuFe (ASX:CUF) has completed the first heritage survey and secured approval of additional Programme of Works for an extended Stage 1 drill program at its North Dam lithium project near Coolgardie, WA.

Existing shareholders in De Grey Mining (ASX:DEG) have subscribed for ~39.1 million shares under its fully underwritten retail entitlement offer priced at $1.10 per share to raise about $43m.

The shortfall of about 38.7 million shares will now be placed with the underwriters to raise a further $42.6m.

Along with the completed placement and institutional component of the entitlement offer, which included major shareholder Gold Road taking up its entire entitlement, DEG will have raised a total of $600m to fund the equity component of its Hemi gold project development.

It also satisfies a key pre-condition of access to debt financing with the company expecting to receive credit approved term sheets from debt financiers in mid-2024.

Elevate Uranium (ASX:EL8) continues to progress its Koppies uranium project in Namibia with the collection of bulk samples for key metallurgical test work.

Future Battery Minerals (ASX:FBM) has started Phase 4B drilling at its Kangaroo Hills lithium project in WA’s Goldfields region.

The 3000m reverse circulation program will test the interpreted north-easterly extension of the high-grade Big Red lithium mineralisation.

It follows on successful Phase 4A drilling that had demonstrated a further 65m of northern continuity via a project-best intercept of 31m grading 1.13% Li2O from a down-hole depth of 86m.

Zinc of Ireland (ASX:ZMI) is nearing completion of its maiden geochemical auger drilling program targeting large rare earths targets at its Cascade project about 70km northwest of Esperance.

At Stockhead, we tell it like it is. While Belararox, CuFe, De Grey Mining, Elevate Uranium, Future Battery Minerals and Zinc of Ireland are Stockhead advertisers, they did not sponsor this article.