ASX Small Caps Lunch Wrap: Which beauty product is causing a Spiderpocalypse this week?

Hey, baby gurl... Back that booty up, baby, coz you be smellin' gooood. Pic via Getty Images.

Good morning, and welcome to 2024. I trust everyone’s consumed their own bodyweight in Panadol and is now sufficiently rehydrated after whatever booze-fuelled mayhem you indulged in over New Years, and you’re ready to get down to some proper, serious ASX business.

Because, unlike last year’s pathetic first day effort, it looks like the ASX has turned up match-ready on the first trading day of the year, with the benchmark turning in an almost exactly-inverse performance compared to 2023, lifting 0.5% before lunch and clinging on to it with all 10 of its dirty, pointy fingernails.

I’ll get into the specifics of that shortly, but first… let’s kick off the year with something of a product warning, because there’s a particular brand of skin cream that users are claiming works really, really well – provided you’re after both “supple, younger looking skin” and swarms of horny wolf spiders invading your personal space.

Customers of French beauty shopping company Sephora are reporting that Sol de Janeiro Delícia Drench Body Butter is doing a lot more than what its marketing literature promises, after a number of reports from people claiming to be users of the product mentioned a sudden, massive increase in the number of wolf spiders in their home.

A couple of theories have been posited, the best of them being that the industrial chemists – sorry, “beauty therapy specialists” – that created this concoction have inadvertantly combined a bunch of chemicals that mimic the smell of an extremely amorous ladyspider.

The company has categorically denied that its product – which they’ve inexplicably named in a manner that suggests that its users might like to be the victim of a Jamaican cannibal – contains spider pheromones.

So, in an effort to avoid a lawsuit on my first day back at work for the year, let me make it absolutely clear that I’m not actually claiming that the stories are true, and that this particular product seems to be drawing randy male wolf spiders out of their hidey holes in an errant, and probably futile, attempt to mate with users of this product.

In fact, it could just be an example of the Baader-Meinhof Effect – where the mention of something in the media leads people to start noticing something that has always been there, but that they’ve just never noticed before.

(Please note that this is different to the similarly-named Bernie Madoff Effect, where the mention of that dude’s name in the media leads people to start noticing that all their money has been stolen.)

But even still, if there’s a chance that slathering yourself in un-natural goo is likely to end up with your house, personal space and probably all available orifices infested with eight-legged nasties, it might be worth reconsidering it for personal use.

So… if you’ve got some, wrap it up nicely and give it to someone you hate – we’re still well inside the “late Christmas gift” window, so you’re unlikely to attract too much suspicion while you’re making a high-speed getaway to safer ground, before your gift’s recipient is overrun by the oncoming spiderpocalypse.

TO MARKETS

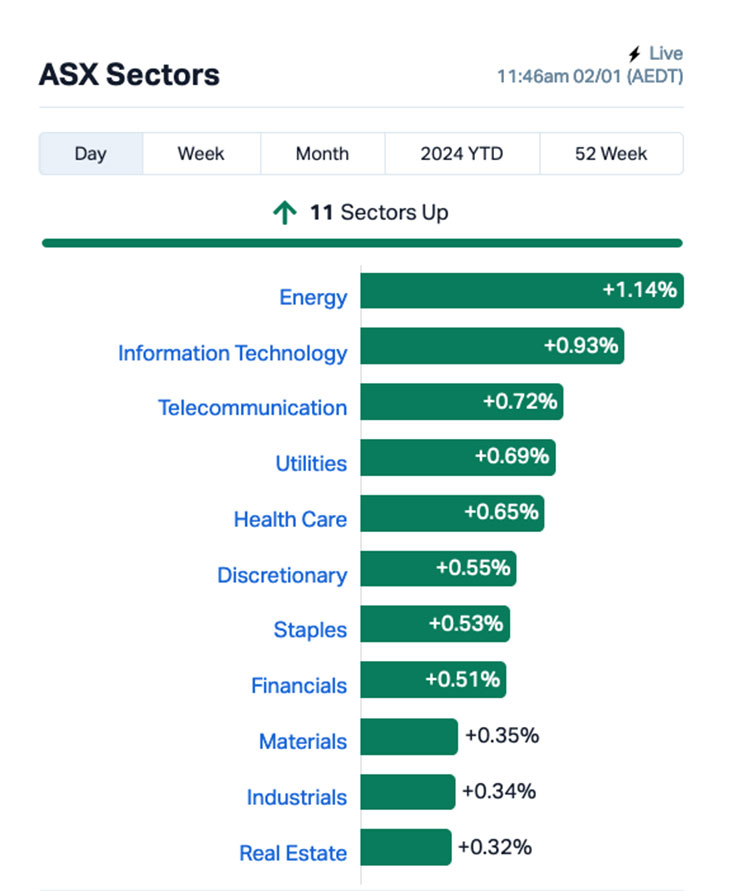

Local markets are enjoying a solid start to 2024, with most of the individual heavy lifting coming from the Materials sector, with a smattering of Healthcare stocks in the mix for moral support and to take care of any injuries in the stampede.

However, it’s the Energy sector that is polling the highest this morning, well out in front of the rest of the market, helped along by a surging oil market that has crude prices pointing 1.5% or 1.3% higher, depending on which flavour of crude you prefer on your Weetbix in the morning.

But the biggest surge this morning has come in the price of uranium, up 5.4% so far today, putting a fair bit of wind in the sails of ASX-listed yellowcake hunters like Paladin Energy (ASX:PDN) (+2.88%) and Deep Yellow (ASX:DYL) (+1.61%).

Coal prices are also continuing to climb, up more than 10% so far over the past month, lending momentum to the likes of Yancoal Australia (ASX:YAL) (+3.23%) and Whitehaven Coal (ASX:WHC) (+2.82%).

An interesting tidbit on the market this morning is an off-market takeover proposal that’s landed on the desk of enviro-chocolate company Yowie Group (ASX:YOW), which is up more than 16% this morning after the market was informed that Keybridge Capital (ASX:KBC) delivered an offer of $0.034 per share on the final trading day for 2023.

This morning, Yowie has asked shareholders to “take no action” until the board has had time to digest the contents of the offer, which will probably take as long to happen as it does to digest those horrendous chocolate Yowies naughty kids get instead of Easter eggs each year.

Yowie’s previous close was at $0.03, but that’s risen beyond the $0.034 offer this morning… so you could be forgiven for expecting that Yowie’s board will view the offer from Keybridge as well-below market value, and request something extra to sweeten the deal.

NOT THE ASX

The final trading day of 2023 was something of a disappointment on Wall Street, especially for investors who were hoping for the fairytale ending that would have seen the S&P 500 close the year on a record high.

Spoiler alert: it didn’t – instead, the S&P 500 retreated by 0.28%, the Nasdaq dropped 0.56% while the Dow was pretty much flat, at -0.05%.

But, all up, it turned out that 2023 was a pretty good year for the US indices. The S&P managed to rise 23.91%, the Dow managed a comparatively paltry 13.45% gain and the tech-heavy Nasdaq recovered from its 2022 annus horribilus to deliver a stonking 43.26% rise.

Tech bubble? What tech bubble? etc etc…

That all pales in comparison to the performance from Bitcoin, though, which delivered a relatively blistering 152% rally over the course of 2023 – and it’s kicked off the year with another gain this morning.

At the time of writing, BTC is up 1.52% to US$44,910.50.

Crypto bubble? What crypto bubble? etc etc…

In Asia market news, Japanese markets are thankfully closed this morning for a National Holiday, which has been marred somewhat by a 7.6-magnitude earthquake that triggered tsunamis around the island nation, leaving at least six people dead.

In China, Shanghai markets are down 0.21% and Hong Kong’s Hang Seng is down 0.51% in early trade, amid claims from Chinese President Xi Jinping’s annual New Year’s address that China’s “reunification” with Taiwan is inevitable, two weeks out from elections for a new leader in the disputed island territory.

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for 02 January [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap PEC Perpetual Resources 0.015 50% 3,531,176 $6,300,294 BPP Babylon Pump & Power 0.006 50% 25,290,811 $9,986,590 MTM MTM Critical Metals 0.092 35% 19,839,754 $6,761,722 NVQ Noviqtech Limited 0.004 33% 2,500,659 $3,928,336 CPO Culpeo Minerals 0.044 26% 4,740,247 $4,079,683 EMV Emvision Medical 2.12 25% 387,192 $132,137,305 EDE Eden Inv Ltd 0.0025 25% 240,741 $7,334,027 NWM Norwest Minerals 0.033 22% 443,126 $7,764,377 RDS Redstone Resources 0.006 20% 714,285 $4,606,892 VAR Variscan Mines Ltd 0.012 20% 390,318 $3,644,448 SGC Sacgasco Ltd 0.013 18% 260,669 $8,547,609 AMM Armada Metals 0.033 18% 14,285 $5,824,000 CPM Cooper Metals 0.4 18% 484,094 $21,880,921 CDR Codrus Minerals Ltd 0.067 18% 2,572,045 $4,998,188 BIO Biome Australia Ltd 0.24 17% 1,336,678 $43,457,058 EYE Nova EYE Medical Ltd 0.28 17% 3,204,152 $45,750,934 YOW Yowie Group 0.035 17% 95,982 $6,557,037 AYT Austin Metals Ltd 0.007 17% 242,029 $7,361,248 MTL Mantle Minerals Ltd 0.0035 17% 2,355,668 $18,592,338 PAM Pan Asia Metals 0.145 16% 650,736 $20,877,679 DAF Discovery Alaska Ltd 0.022 16% 215,526 $4,450,459 IXU Ixup Limited 0.038 15% 200,000 $35,888,675 DXB Dimerix Ltd 0.235 15% 4,632,971 $87,346,959 GSR Greenstone Resources 0.008 14% 92,543 $9,576,794 SRZ Stellar Resources 0.008 14% 920,619 $8,043,185

Something’s happening at MTM Critical Metals (ASX:MTM) this morning, and it looks like the cat is at least partially out of the bag.

MTM’s price surged more than 35% on no news early in the day, before a trading halt was requested at 11:23am “pending [the company] releasing an announcement”.

At the time of writing, that announcement hasn’t landed yet. We’ll have something on it once it does.

In second place, Culpeo Minerals (ASX:CPO) is still enjoying its rapid rise in fortune, ostensibly off the back of last December’s announcement of significant widths of visible copper mineralisation intersected at very shallow depth at the El Quillay Prospect, Fortuna Project in Chile.

Meanwhile, Pan Asia Metals (ASX:PAM) jumped around 20% this morning on news that the company has signed on the dotted line to convert existing MOUs into binding Option Agreements to purchase 100% of the ~1,200km2 Tama Atacama Lithium Brine Project, one of the largest lithium brine projects in South America.

PAM says that Tama Atacama is a Tier 1 asset in a Tier 1 jurisdiction “in the truest sense of the term ‘Tier 1’”, citing “extensive lithium surface anomalies with elevated lithium results up to 2,200ppm Li and averaging 700ppm Li (270ppm Li cutoff) extending over 160km north to south”.

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for 02 January [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap LSR Lodestar Minerals 0.003 -25% 1,357,044 $8,093,589 ME1 Melodiol Global Health 0.0015 -25% 1,244,193 $9,457,648 NOV Novatti Group Ltd 0.066 -20% 595,000 $28,108,493 88E 88 Energy Ltd 0.004 -20% 3,986,028 $123,204,013 EQS Equity Story Group 0.03 -19% 30,000 $1,576,747 IPB IPB Petroleum Ltd 0.009 -18% 1,089,481 $6,216,347 OAR OAR Resources Ltd 0.0025 -17% 163,526 $7,931,183 SFG Seafarms Group Ltd 0.005 -17% 351,636 $29,019,595 FCT Firstwave Cloud Tech 0.034 -15% 124,940 $68,383,225 AVE Avecho Biotech Ltd 0.003 -14% 8,782 $11,092,540 IEC Intra Energy Corp 0.003 -14% 35,000 $5,812,736 PXX Polarx Limited 0.006 -14% 20,493 $11,477,317 RIL Redivium Limited 0.006 -14% 851,937 $19,115,984 ST1 Spirit Technology 0.069 -14% 1,622,107 $58,955,043 HIQ Hitiq Limited 0.019 -14% 6,200 $7,182,069 TSI Top Shelf 0.19 -14% 23,636 $45,644,689 OEC Orbital Corp Limited 0.091 -13% 115,763 $15,309,707 SMS Star Minerals Ltd 0.035 -13% 95,500 $3,036,912 HMI Hiremii 0.036 -12% 1,723,286 $4,940,235 A8G Australasian Metals 0.15 -12% 41,718 $8,860,484 XGL Xamble Group Limited 0.054 -11% 20,000 $18,030,674 DOU Douugh Limited 0.004 -11% 32,427 $4,869,310 GBZ GBM Rsources Ltd 0.008 -11% 102,000 $6,582,896 GLV Global Oil & Gas 0.016 -11% 1,120,973 $8,406,006 ODE Odessa Minerals Ltd 0.008 -11% 623,611 $8,524,006

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.