ASX Small Caps Lunch Wrap: Lack of leadership has Aussie stocks flailing ahead of Big Wednesday CPI read

Via Getty

- S&P/ASX 200 index was down by 11 points or -0.15% at midday

- IT the winningest sector, as Materials leads the laggards

- Top ASX Small Caps: Sunshine Metals, Adore, Chariot Corp

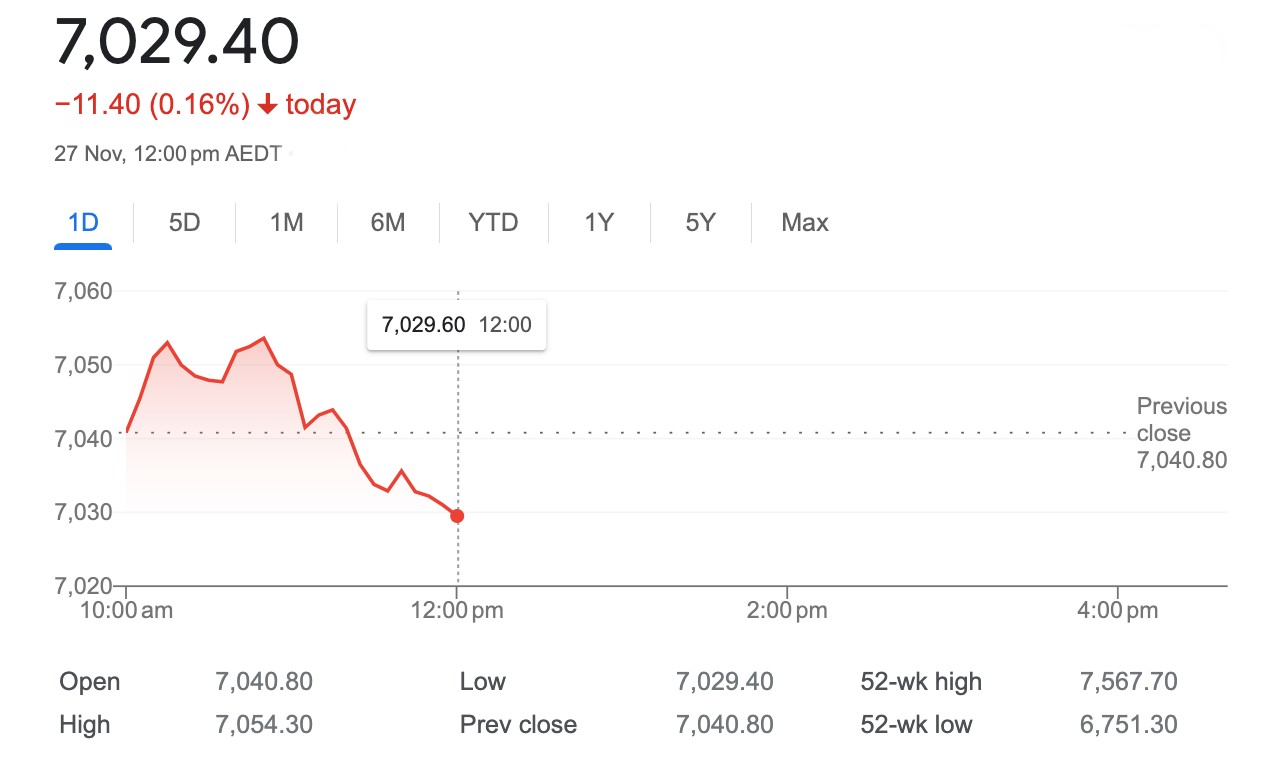

At midday on Monday Nov. 27, the S&P/ASX 200 index was down by 11 points or -0.15% to 7030.

‘Tepid’ is the word of the moment.

After rising reluctantly in the early hours of business the local market has wilted under the tyranny of uncertainty as traders keep one eye on this week’s monthly inflation report, and the likely reaction of a newly anxious central bank.

Wall Street’s given the local team very little to go on after a brief and light half-day of Thanksgiving trade.

At the 1300 close in New York, the S&P 500 was as good as flat (up +0.06%), the Dow Jones index was up by +0.33%, and the tech-heavy Nasdaq Composite handed back -0.11% after Nvidia fell by -2%.

US retail stocks outperformed the broader market as online sales on Black Friday hit almost US$10bn.

Also just in – Chinese industrial profits remain awfully subdued, according to the latest data out of the mainland.

Profits earned by China’s industrial firms fell by 7.8% year-on-year to RMB 6,115.42 billion in the first 10 months of the year, dragging lower on the a 9.0 % slump in the prior period. In October alone, industrial profits increased by 2.7% yoy, much slower than a 11.9% jump in September.

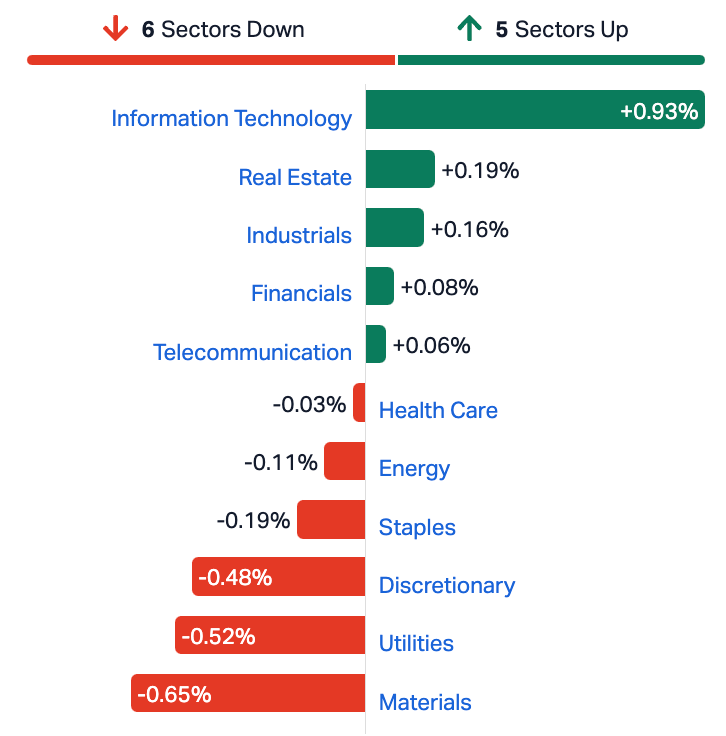

At home, the IT sector has gone about its cyclical dance, recouping some of last week’s losses:

The Materials Sector doing its very best to offset the gains out of IT, with major iron ore miners and the broader digging family again the major drag on local stocks.

The iron ore price is softer over in Singapore, the December contract wheeling back toward $130/t after threatening $140.

That’s naturally taken the edge off the big three iron ore heavyweights, BHP (ASX:BHP) and Rio Tinto (ASX:RIO) are around 0.9% lower, while Fortescue (ASX:FMG) has already lost -1.6%.

The Energy Sector is slightly lower after Brent oil futures remain close to the $US80 mark, as traders trade water ahead of the OPEC+ meeting that was pushed from 26 November to 30 November.

The outcome for oil production targets for 20 OPEC+ members for 2024, alongside any voluntary production cuts are on the line.

CBA’s Vivek Dhar notes that with the meeting delay tied to reports that Nigeria and Angola wanted higher production quotas for next year, markets have “justifiably reduced their expectation that the group will deliver deeper production cuts.”

Meantime, the Healthcare Sector can thank Healius (ASX:HLS) for leaving it near parity. The HLS share price is rebounding after a broker upgrade following heavy losses late last week, while the surprise catalyst is the exit-stage-left for chair Jenny Macdonald with non-exec director Kate McKenzie to take over as interim chair.

ASX SECTORS ON MONDAY AT LUNCH

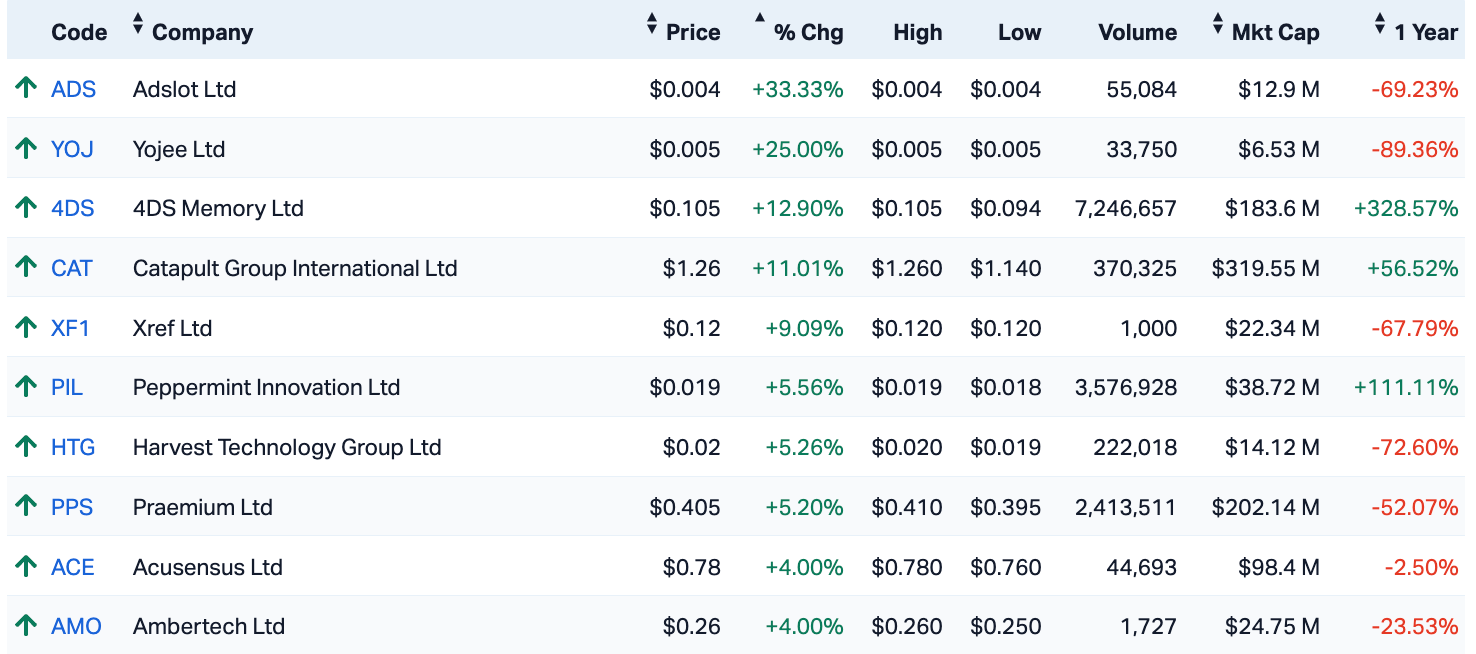

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for 27 November [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | Market Cap |

|---|---|---|---|---|---|

| ADS | Adslot Ltd | 0.004 | 33% | 55084 | $9,673,487 |

| MRD | Mount Ridley Mines | 0.002 | 33% | 4450000 | $11,677,324 |

| SHN | Sunshine Metals Ltd | 0.0275 | 31% | 63773660 | $25,704,177 |

| IDT | IDT Australia Ltd | 0.12 | 29% | 1563704 | $32,687,591 |

| HNR | Hannans Ltd | 0.009 | 29% | 4344733 | $19,115,984 |

| CAV | Carnavale Resources | 0.005 | 25% | 2207598 | $13,694,207 |

| YOJ | Yojee Limited | 0.005 | 25% | 33750 | $5,221,941 |

| CC9 | Chariot Corporation | 1.18 | 19% | 1393444 | $72,598,252 |

| AEI | Aeris Environmental | 0.032 | 19% | 114409 | $6,632,403 |

| ABY | Adore Beauty | 1.105 | 18% | 267095 | $87,803,393 |

| SIX | Sprintex Ltd | 0.013 | 18% | 5324615 | $4,003,956 |

| HAR | Haranga Resources | 0.23 | 18% | 505591 | $12,833,734 |

| BWF | Blackwall Limited | 0.53 | 18% | 1000 | $30,641,183 |

| A1G | African Gold Ltd. | 0.035 | 17% | 2714 | $5,079,336 |

| CHR | Charger Metals | 0.295 | 16% | 215111 | $15,839,164 |

| HMI | Hiremii | 0.045 | 15% | 600000 | $4,650,971 |

| KCC | Kincora Copper | 0.03 | 15% | 178561 | $4,163,303 |

| AYT | Austin Metals Ltd | 0.008 | 14% | 18 | $7,111,123 |

| BUY | Bounty Oil & Gas NL | 0.008 | 14% | 2940853 | $9,593,507 |

| RGL | Riversgold | 0.016 | 14% | 28698552 | $13,317,660 |

| UVA | Uvrelimited | 0.17 | 13% | 1123189 | $4,904,734 |

| DGH | Desane Group Hldings | 0.95 | 13% | 547 | $34,364,392 |

| A8G | Australasian Metals | 0.175 | 13% | 29636 | $8,078,677 |

| ATH | Alterity Therap Ltd | 0.0045 | 13% | 156111 | $9,759,590 |

| KP2 | Kore Potash PLC | 0.009 | 13% | 649596 | $5,352,460 |

Sunshine Metals (ASX:SHN) is still collecting kudos coupons on Monday morning for its efforts late last week out at the Ravenswood Consolidated Project in North Queensland.

The heavily diluted $24 million micro cap may’ve struck ultimate paydirt in a gold and copper rich feeder zone to its 2.3Mt zinc, gold, copper, lead and silver VMS resource at the Liontown deposit.

Last week the MD Damien Keys said the “stunning intercepts at Liontown” were the reward for the team’s “solid geological work.”

“The decision was made to target the gold-copper rich footwall and feeder zones to the Liontown Resource with a high impact, shallow RC program. The feeder zones have not been recognised by past explorers and are often difficult to target.”

Another 11 holes have already been drilled to target these feeder zones and footwall lodes, with assays due in December this year.

The stock has found another 30% on Monday morning.

Adore Beauty (ASX:ABY) is the surprise Monday morning package. The online cosmetics retailer is nearing a 12 month high after choosing to turn its nose up at a takeover offer from British giant THG.

After speculation about an offer over the last few weeks, Adore Beauty this morning confirmed that it’d received a non binding, conditional and indicative proposal from THG plc (LON:THG) for 100% of the shares of the Company by way of a scheme of arrangement for A$1.25-1.30 cash per share.

Here’s what ABY thought of it:

Following a review of the terms of the Proposal with the assistance of its financial and legal advisers, the Board of Adore Beauty (Board) concluded that the Proposal undervalued the Company, was unable to be implemented, and was not in the best interests of shareholders. For these reasons, the Board rejected the Proposal.

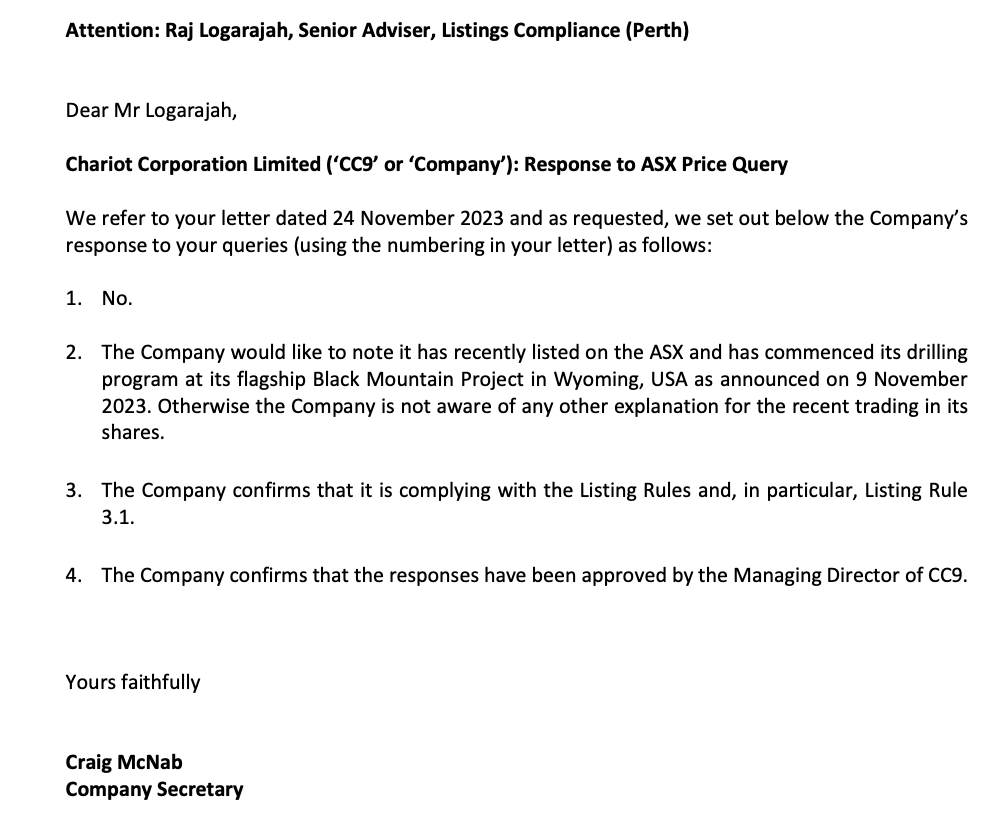

In late October one of the biggest lithium IPOs of 2023, Chariot Corp (ASX:CC9), hit the bourse with a market cap of $67.5m at 45c per share.

This stock is killing it.

It’s up again today after rising some +145% last week, earning it this warning (and reply) near the end of last session:

CC9 has one of the largest lithium exploration landholdings in the United States, plus a bunch of JVs, farm outs and optioned projects.

Their focus is the 2sqkm Black Mountain in Wyoming, an emerging hard rock province quickly gaining in popularity.

This project has never been drilled — until now — despite 60cm long spodumene crystals (~6-7% lithium) being observed back in 1997 and subsequent early-stage exploration returning assays up to 6.68% Li2O from rock chips.

That’s high grade and it would seem the word is getting out faster than expected.

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for 24 November [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | Market Cap |

|---|---|---|---|---|---|

| AMD | Arrow Minerals | 0.001 | -33% | 2,093 | $4,535,648 |

| BP8 | BPH Global Ltd | 0.001 | -33% | 2,800,000 | $2,423,345 |

| ME1 | Melodiol Glb Health | 0.002 | -33% | 8,014,606 | $12,654,126 |

| VPR | Volt Power Group | 0.001 | -33% | 9,951 | $16,074,312 |

| AVM | Advance Metals Ltd | 0.003 | -25% | 803,000 | $2,889,387 |

| PRX | Prodigy Gold NL | 0.007 | -22% | 100,012 | $15,759,970 |

| EDE | Eden Inv Ltd | 0.002 | -20% | 1,100 | $8,409,092 |

| IEC | Intra Energy Corp | 0.004 | -20% | 12,615,561 | $8,303,908 |

| M4M | Macro Metals Limited | 0.004 | -20% | 16,795,751 | $12,335,389 |

| FAR | FAR Ltd | 0.355 | -18% | 644,560 | $40,198,197 |

| M2R | Miramar | 0.018 | -18% | 42,500 | $3,275,130 |

| AAU | Antilles Gold Ltd | 0.023 | -18% | 3,969,635 | $22,201,397 |

| HIQ | Hitiq Limited | 0.019 | -17% | 32,106 | $7,508,527 |

| ESR | Estrella Res Ltd | 0.005 | -17% | 152,622 | $10,554,431 |

| SFG | Seafarms Group Ltd | 0.005 | -17% | 405,173 | $29,019,595 |

| ILT | Iltani Resources Lim | 0.145 | -15% | 15,000 | $5,781,786 |

| LRL | Labyrinth Resources | 0.006 | -14% | 137,163 | $8,312,806 |

| MEM | Memphasys Ltd | 0.012 | -14% | 1,132,240 | $13,433,285 |

| MTB | Mount Burgess Mining | 0.003 | -14% | 24,000 | $3,554,764 |

| OAR | OAR Resources Ltd | 0.003 | -14% | 205,000 | $9,193,272 |

| AMM | Armada Metals | 0.045 | -13% | 200,000 | $8,973,540 |

| FYI | FYI Resources Ltd | 0.075 | -13% | 541,713 | $31,520,513 |

| GGE | Grand Gulf Energy | 0.007 | -13% | 4,241,600 | $16,761,976 |

| PAB | Patrys Limited | 0.007 | -13% | 302,408 | $16,459,579 |

| PLG | Pearl Gull Iron | 0.035 | -13% | 251,493 | $8,181,672 |

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.