ASX Small Caps Lunch Wrap: GDP drama is over, now markets brace for the lack of drama, drama

Via Getty

Australian markets didn’t know what to make of the impending fourth straight quarter of negative Aussie economic growth on Tuesday and now that it’s dropped few seem to know how to play it.

Weak overnight leads and dull Chinese economic ambitions led markets lower this morning, but there’ll be some decent action this arvo as traders decide how to play a GDP read which the Reserve Bank won’t hate.

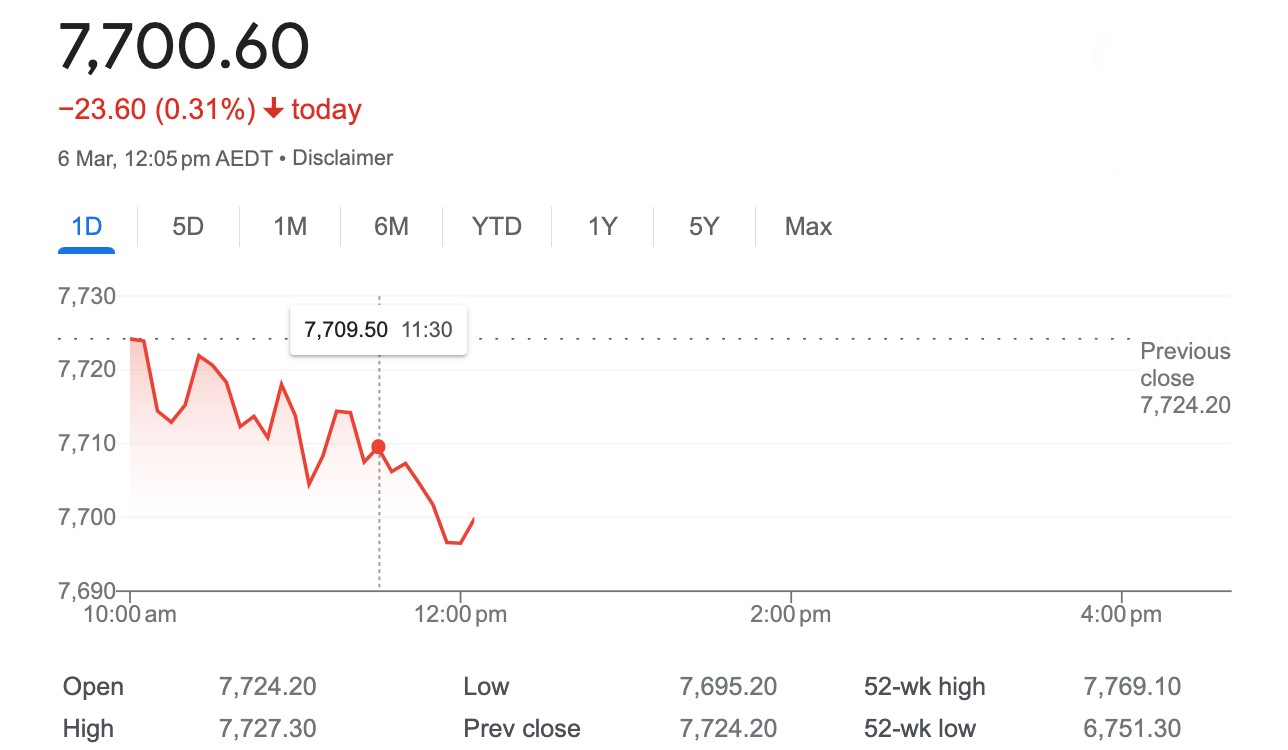

At 12pm on Wednesday March 6, the benchmark ASX200 (XJO) was down 23.5 points or 0.31% lower at 7,700.60.

I’ve marked the 11.30am moment above when the GDP data everyone was stressing about dropped.

It’s not the end of the world, or even Tassie and you’d think the RBA would be pleased with its handiwork in cooling spending.

The domestic economy expanded by 0.2% in Q4 of 2023, easing from an upwardly revised 0.3% in Q3 in line with concensus and making it nine straight quarters of growth.

Go Aussie. But not yet… this quarter was the softest of that consecutive run since the Q3 read of 2022.

Same problems though – household spending was muted, as was government spending

Through the year, Aussie GDP grew by 1.5%, slightly above forecasts of 1.4%.

The ASX…

Well, there’s a fair bit of the risk-off sentiment about the ASX on Wednesday, just as we saw on global equity markets overnight.

Having cooked for the kids for two weeks straight now that Mrs Edwards is away on business, I for three, know risk-off sentiment when I see it.

The Europeans dropped at the close – as did Wall Street – both a little unofficially bummed about the signals from Beijing coming out of the opening of the National People’s Congress.

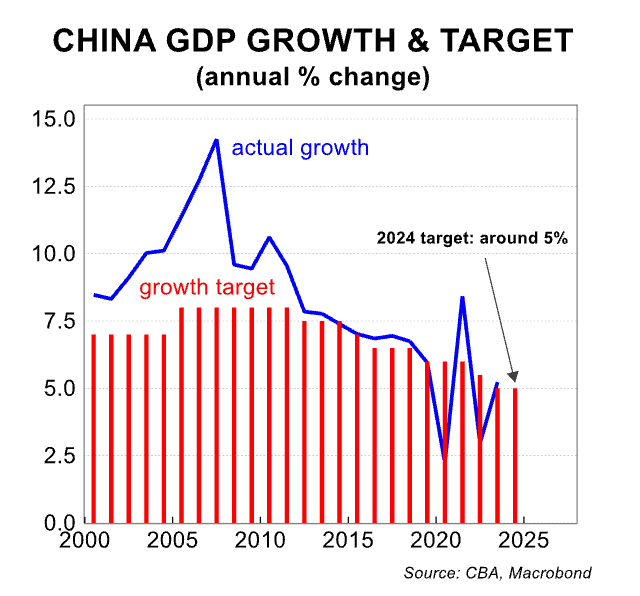

On Tuesday, the Chinese government got together for the semi-annual NPC where Premier Li Qiang delivered the Government Work Report which revealed a 2024 GDP growth target of ‘around 5%’.

The target is in line with last year’s kitten of a number as well as pretty much most consensus estimates I’ve seen.

That said, the 5% target will be a tough one for the Party to hit without further economic stimulus – a view supported by the economic team at CBA and elsewhere.

CBA economist and currency strategist Carol Kong expects fiscal support will increase modestly this year with a focus on infrastructure investment. But it remains to be seen if the policy support will be sufficient to meet the ambitious growth target. At this stage, it retains a 2024 GDP growth forecastof 4.9%.

In local company action, we saw Infratil lead out the blue caps, alongside Meridian Energy.

At the darker end of the tunnel, David Dicker’s Dicker Data crashed by double digits, which happens when the man the company’s named after begins to offload about 10% of the stock in a $200m block trade.

Safety assets gold and BTC meantime set new record highs, although gold stocks are generally lower alongside most of Materials sector which is weighing.

The price of gold clocked its new record high of US$2,141 per troy ounce, driven by what’d be growing anticipation of some US rate cutting.

Pushing that are the more than significant central bank buying of the safe haven and the mission of Chinese investors, sent forth to suck up what they can.

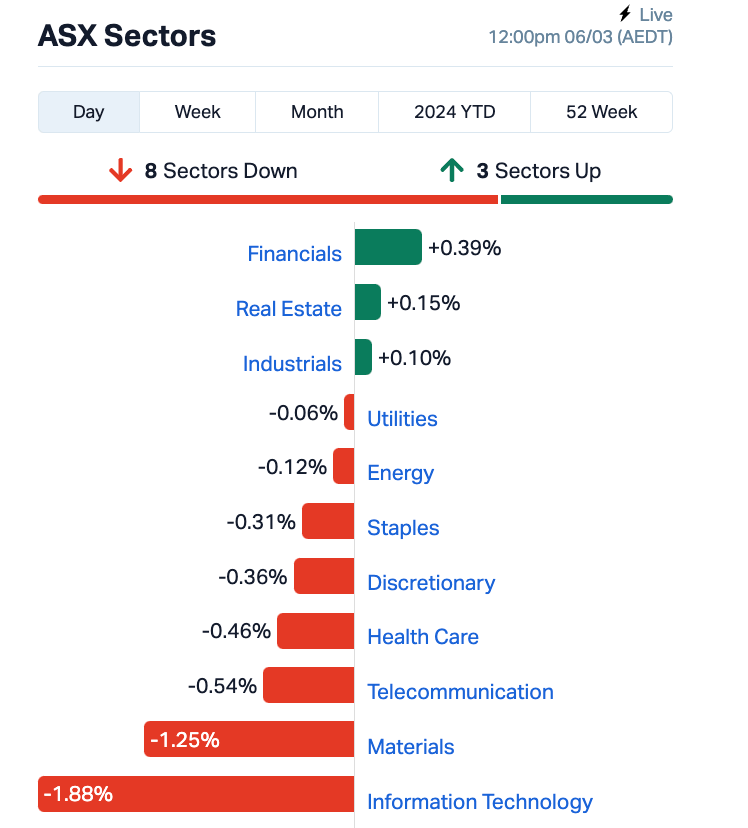

The banks are about 0.4% higher. The other 10 sectors aren’t really up for Wednesday so far. That could change now GDP isn’t hiding any tricks.

The brief success of the lithium sector and friends from the battery minerals family over the last few sessions looks like being more a blip and the dip could be back.

Majors IGO (ASX:IGO) and Pilbara Minerals (ASX:PLS) were 5% and 3% worse off by lunch.

But that may change again – and certainly the news that Canada and Australia have formally agreed to collaborate on advancing shared priorities concerning the extraction, processing, and refining of critical minerals, as per the joint ministerial statement late on Tuesday.

ASX Sectors at 12pm on Wednesday

I’m going Ex-Dividend (so are these stocks)…

Accent Group (ASX:AX1) is paying 8.5 cents fully franked

Capitol Health (ASX:CAJ) is paying 0.5 cents fully franked

EQT Holdings (ASX:EQT) is paying 51 cents fully franked

Hearts and Minds Investments (ASX:HM1) is paying 7 cents fully franked

Jupiter Mines (ASX:JMS) is paying 1 cent unfranked

Laserbond (ASX:LBL) is paying 0.8 cents fully franked

Monadelphous Group (ASX:MND) is paying 25 cents fully franked

Northern Star Resources (ASX:NST) is paying 15 cents unfranked

Pacific Current Group (ASX:PAC) is paying 15 cents unfranked

QBE Insurance (ASX:QBE) is paying 48 cents 10 per cent franked

Reliance Worldwide (ASX:RWC) is paying 3.459 cents unfranked

Smartgroup Corporation (ASX:SIQ) is paying 32 cents fully franked

SkyCity Entertainment Group (ASX:SKC) is paying 4.87 cents unfranked

Servcorp (ASX:SRV) is paying 12 cents 20% franked

Shaver Shop (ASX:SSG) is paying 4.7 cents fully franked

Super Retail Group (ASX:SUL) is paying 32 cents fully franked

Treasury Wine Estates (ASX:TWE) is paying 17 cents 70% franked

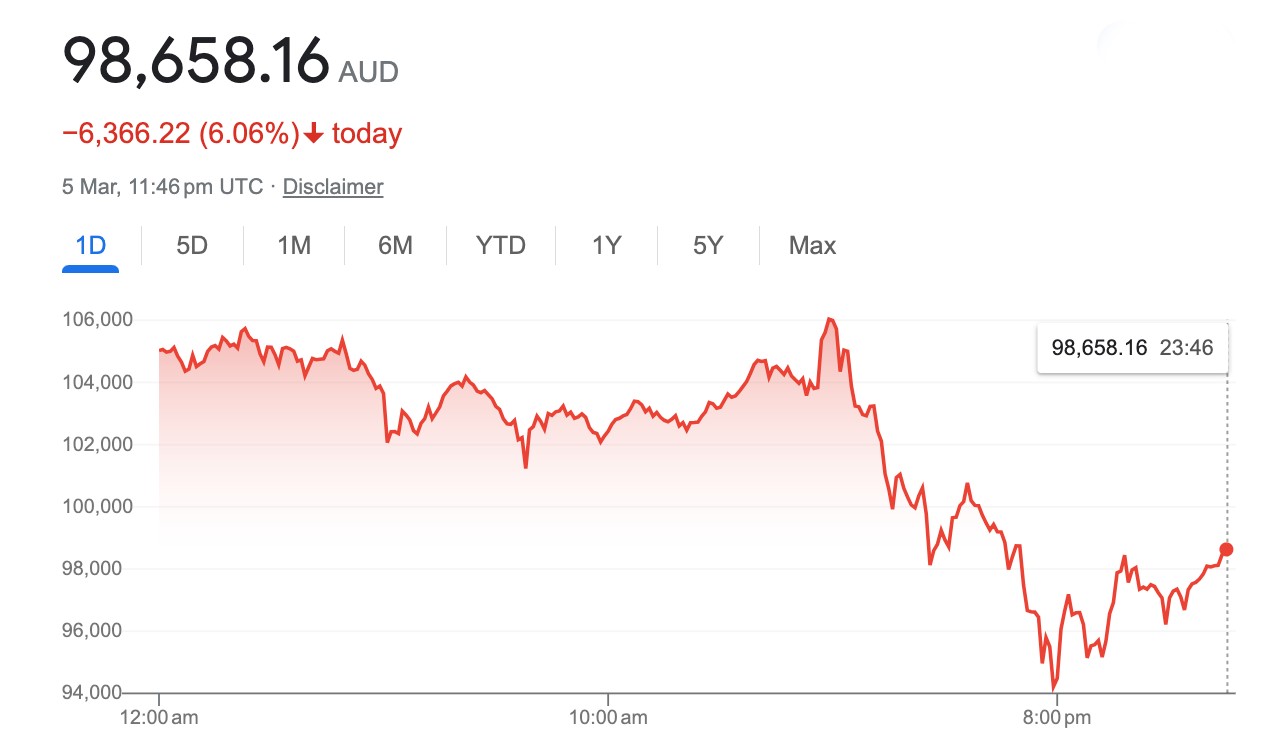

Bitcoin’s getting halved again and all that new record high jazz…

The price of Bitcoin, touched a new all-time high of more than US$69,000, whacking the previous November 2021 high.

The world’s biggest crypto then gave most of it up in the intervening 12 months, hitting US$16,500 at its nadir.

The new surge in price has been spurred by US finance giants pouring billions into buying Bitcoins.

BTC Market’s crypto analyst Caroline Bowler says the integration of cryptocurrency into mainstream financial institutions is a crucial moment for Australian investors.

“Recent developments in US regulations regarding spot Bitcoin ETFs and the advocacy of major investment firms highlight the growing acceptance of crypto in traditional finance.”

The cryptocurrency rose to around $69,200 on Tuesday…

…before falling back to around US $63k or about $94,000 Aussie.

Bowler says the SEC move to open up Bitcoin to retail and institutional investors has been pivotal.

“Locally, it sets the stage for potential ASX listings of spot Bitcoin ETFs, further integrating crypto assets into mainstream financial services. The lasting impacts of these developments are expected to unfold progressively over time, influencing cryptocurrency markets and investor participation.

Research from Standard Chartered forecasts a potential US$100k valuation for Bitcoin by the end of the year, drawing parallels with the growth of gold ETFs.

Caroline says the upcoming Bitcoin halving in April is viewed as an additional positive indicator for its market dynamics.

“The Bitcoin halving typically impacts BTC price positively. The halving event occurs approximately every four years and involves a reduction in the rewards miners receive for validating transactions by half. This event is hard coded into Bitcoin’s protocol and is designed to limit the total supply of Bitcoin to 21 million.”

Not the ASX…

Wall Street fell for a second session Tuesday in New York, as Mega Tech got less mega for a day.

Apple lost ground after a research report showed iPhone sales in China fell 24% year-on-year in the first six weeks of the year in the face of increased competition from Chinese rivals such as Huawei.

Tesla shares continue to hit reverse a suspected arson attack went down at the Gigafactory in Germany.

The Nasdaq Composite crashed 1.7% overnight as tech led markets lower.

The Dow Jones Industrial Average shed more than 1% as did the S&P500. Intel and Salesforce were the worst performers on the Dow, both dropping about 5%.

Apple was lower again – this time shedding 3% as our old short-selling research mates at Counterpoint spread word that iPhone sales were way down in China so far this year.

Netflix and Microsoft were as bad – down 3% – while Tesla dropped another 4% possibly because of Elon and his adventures.

Elsewhere in tech GitLab crashed over 20% after the software maker laid out the weakness of its likely full year overnight.

Tuesday’s moves come as investors digest the market’s recent rally to all-time highs, which has been powered by optimism around artificial intelligence. Despite the intraday losses, the three major averages are solidly higher year to date.

All sectors ended lower overnight except for Energy, Consumer Staples and Financials. Tech was unsurprisingly the worst, following the gaggle of poor returns from the magnificent friends of Google et al.

US Futures are thusly on Wednesday at lunch in Sydney:

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for 6 March [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap AT1 Atomo Diagnostics 0.042 56% 36,708,598 $17,258,462.37 M4M Macro Metals Limited 0.0045 50% 99,831,000 $8,436,233.27 1AD Adalta Limited 0.034 36% 52,128,629 $13,145,101.93 NME Nex Metals Exploration 0.017 31% 107,298 $4,582,922.85 AN1 Anagenics Limited 0.015 25% 445,851 $5,029,594.32 NVQ Noviqtech Limited 0.005 25% 11,892,308 $5,237,781.18 ODY Odyssey Gold Ltd 0.022 22% 790,326 $16,179,680.41 SLZ Sultan Resources Ltd 0.017 21% 228,176 $2,074,660.69 AL8 Alderan Resource Ltd 0.006 20% 4,333,333 $5,534,306.53 G88 Golden Mile Res Ltd 0.012 20% 164,057 $4,112,228.55 OAU Ora Gold Limited 0.006 20% 12,452,087 $28,700,004.46 AAJ Aruma Resources Ltd 0.019 19% 1,160,753 $3,150,264.10 IKE Ikegps Group Ltd 0.415 19% 65,312 $56,085,041.25 ASV Asset Vision Co 0.013 18% 345,000 $7,984,202.22 CR1 Constellation Res 0.1 18% 816,829 $4,241,961.21 TAM Tanami Gold NL 0.034 17% 1,027,931 $34,077,814.33 EPM Eclipse Metals 0.007 17% 90,000 $12,450,325.43 RNX Renegade Exploration 0.007 17% 1,896,028 $6,010,342.68 DEL Delorean Corporation 0.065 16% 252,661 $12,080,371.24 IPT Impact Minerals 0.015 15% 19,723,159 $37,241,150.56 FFG Fatfish Group 0.031 15% 8,388,835 $37,536,471.55 BFC Beston Global Ltd 0.008 14% 5,965 $13,979,328.24 ZEU Zeus Resources Ltd 0.008 14% 2,507,990 $3,214,967.00 ARV Artemis Resources 0.017 13% 4,655,242 $25,367,942.24 ASO Aston Minerals Ltd 0.017 13% 4,416,645 $19,425,964.04

Local medical device maker Atomo Diagnostics (ASX:AT1) says it’s just secured a very handy purchase order from Viatris Healthcare worth about a million Aussie.

The order is for HIV Self-Tests, manufactured by Atomo under the Mylan brand for supply to a number of Low-and Middle-Income Countries (LMICs), where the spread of HIV-related disease is still a massive challenge, according to MD and CEO John Kelly.

The orders are for manufacture during H2 of FY24.

Atomo considers the revenue from these orders to be material.

“We have seen growing demand during FY24 for the Atomo HIV Self-Test here in Australia as well as across branded versions supplied to international markets. Following significant increases in sales to Europe and in Australia, it is good to now see emergent demand across LMIC markets from our global health partner for HIV testing, Viatris,” Kelly says.

Also soaring from the small cap Aussie medspace is clinical stage drug development firm AdAlta (ASX:1AD).

The Melbourne-HQ’d 1AD says key results are in from its Phase I extension study of lead asset AD-214, which “positively answer questions being asked to date by pharma company partners, while establishing the safety and tolerability of the planned Phase II dose.”

AD-214 is being developed for fibrotic diseases including the debilitating and fatal disease, Idiopathic Pulmonary Fibrosis (IPF) and is now ready to progress to Phase II clinical studies, says AdAlta CEO and MD, Tim Oldham.

“With these excellent results, we believe we have answered in the best way possible the key clinical questions large pharma company partners have been asking about AD-214.”

With these questions apparently answered, the molecule, Oldham says, is now prepared for Phase II clinical studies, a “significant milestone” for AdAlta.

“We have already commenced the process of sharing these latest results with our potential partners with a view to progressing a licensing or asset financing transaction in the near term. Such a transaction would enable AD-214 to advance to Phase II clinical trials in Idiopathic Pulmonary Fibrosis to provide a new option for patients with this debilitating and fatal disease as well as providing a return on our investment to date.”

In the digging stuff up sector and right off the bat, Aruma Resources (ASX:AAJ) says its maiden REE-focused drilling program at the Salmon Gums Project in WA has intersected high-grade rare earths (REE).

Maiden REE drill at Eastern Gold Fields “returned multiple high-grade clay REEs of significant thickness”, the company says;

– 11m at 904ppm TREO from 18m in SG24AC024

– 6m at 770pmm TREO from 24m in SG24AC030

– 6m at 727ppm TREO from 15m in SG24AC048

– 3m at 933ppm TREO from 21m in SG24AC053

The company also says surface sampling of exposed ionic clays has returned the highest REE result in the area to date; 8,700ppm TREO with high-value Nd + Pr oxides

representing 22.5% of TREO grade.

The REE drilling also confirms a northern extension of recent REE discoveries by Meeka Metals (ASX:MEK) and OD6 Metals (ASX:OD6) in the same region.

And finally Metalicity (ASX:MCT) is higher after drilling approvals came in for its maiden drilling program at Yundamindra – lodged for the first drill program in over a decade at the Project

MCT says the plan is to target the “highly prospective Western Line, including the Landed at Last prospect.”

Yundamindra has only ever had limited shallow drilling, to a maximum of 50-80m and the Landed at Last prospect has historically returned outstanding shallow, high-grade results.

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for 6 March [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap ABE Australian Bond Exchange 0.01 -33% 125,584 $1,690,022 CTT Cettire 3.63 -22% 8,839,802 $1,776,570,105 EDE Eden Innovations 0.002 -20% 390,375 $9,195,678 ESR Estrella Resources 0.004 -20% 3,759,351 $8,796,859 ROG Red Sky Energy 0.004 -20% 775,755 $27,111,136 SEG Sports Entertainment Group 0.19 -19% 2,200 $62,215,872 GCM Green Critical Minerals 0.005 -17% 2,066,940 $6,819,510 VAL Valor Resources Ltd 0.0025 -17% 18,909 $13,767,040 REY REY Resources Ltd 0.085 -15% 900 $21,168,754 WHK Whitehawk Limited 0.042 -14% 12,392,442 $16,565,465 HFY Hubify Ltd 0.012 -14% 7,194 $6,945,908 T3D 333D Limited 0.006 -14% 3,333 $836,115 SRX Sierra Rutile 0.1 -13% 121,857 $48,787,191 AKN Auking Mining Ltd 0.02 -13% 1,975,169 $5,413,135 ASQ Australian Silica 0.04 -13% 245,876 $12,965,577 PPG Pro-Pac Packaging 0.205 -13% 43,350 $42,696,612 EXT Excite Technology 0.007 -13% 2,010,299 $10,633,934 EWC Energy World Corporation 0.015 -12% 50,001 $52,341,661 BKG Booktopia Group 0.055 -11% 40,158 $14,148,716 LTM Arcadium Lithium PLC 7.31 -11% 2,552,868 $3,482,139,070 NSB Neuroscientific 0.04 -11% 14,532 $6,507,219 SOP Synertec Corporation 0.12 -11% 83,000 $58,251,951 ADG Adelong Gold Limited 0.004 -11% 4,350,500 $3,230,950 TSL Titanium Sands Ltd 0.008 -11% 132,524 $17,943,572 TRE Toubani Resources 0.125 -11% 30,610 $18,741,193

ICYMI at Midday

Pursuit Minerals (ASX:PUR) has started drilling the first hole into the Maria Magdalena tenement which forms part of its Rio Grande Sur lithium project in Argentina.

Each drill hole is expected to reach a depth of 500-600m and will take about one month to complete. Results are expected over the coming months.

This phase of drilling is aimed at growing the project’s existing inferred resource of 251,300t LCE @ 351 mg/Li.

Conrad Asia Energy (ASX:CRD) has added a further $2.85 million to its bank account following the completion of a security purchase plan and shortfall placement to eligible CDI holders.

The supplementary raising was announced alongside last month’s $13 million placement to new and existing institutional and sophisticated investors.

Proceeds from both capital raisings will be used to complete a 3D seismic survey across the company’s shallow water Aceh gas discoveries and ongoing costs associated with the Mako gas project offshore Indonesia.

At Stockhead, we tell it like it is. While Conrad Asia Energy and Pursuit Minerals are Stockhead advertisers, they did not sponsor this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.