ASX Small Caps Lunch Wrap: China goes big then goes home, local markets dip despite iron surge

Pic: Getty Images

Local markets have fallen this morning, despite iron ore prices lifting and Chinese stimulus turning the markets there red-hot yesterday, ahead of a week of national holidays.

I’ll get to the Chinese market stuff later – but it’s worth noting that China and Hong Kong are both closed today, so there’s no action from them to report.

On the ASX, there’s been a broad sell-down in Materials that has weighed heavily during the session before lunch, leaving Health and InfoTech to struggle vainly to keep everyone’s spirits up.

After touching new records yesterday, the benchmark ASX 200 was down about 0.5% as the lunch bell rang.

Here’s how it’s all played out so far today.

TO MARKETS

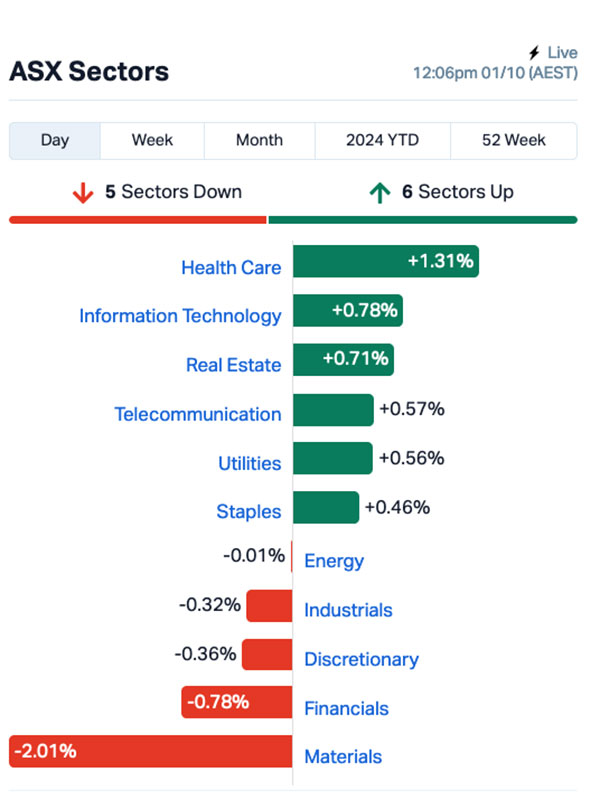

Health Care and InfoTech have been leading the charge on the ASX this morning, but it’s not been enough to offset a 2.0% drag from the Materials sector, which has brought the benchmark down by 0.5% before lunch.

Pre-market, the ASX 200 Futures was pointing 0.3% lower before the market opened this morning, with local investors waiting on data today around construction and retail spending.

Up the big end of town, REA Group (ASX:REA) has had its offer for UK real estate portal Rightmove rejected, with the Murdoch-owned REA expressing its disappointment that the UK takeover target never really came to the table to talk about the $12 billion deal.

And Qatar Airways has signalled its desire to purchase 25% of Australia’s Virgin Airlines (ASX:VAH) from US private equity firm Bain Capital, which could spell trouble for Qantas (ASX:QAN). The deal is in its infancy, and there are several major hoops that still need to be jumped through – including approval from the Foreign Investment and Review Board.

Overnight, gold fell by 1% to US$2,634 an ounce, oil prices rose by 0.2% with Brent crude trading at US$71.87 a barrel earlier this morning – but petrol around Australia is really cheap at the moment, according to the Australian Institute of Petroleum.

And the increasingly important iron ore price has jumped overnight by 6% to $US108.90 a tonne, which I thought was likely to put more vim and vigour in the step of the ASX’s big miners later today.

But, I was wrong. It happens from time to time… most days, actually, if I’m being honest.

The Materials sector was off by 2.0% at lunchtime, with some of the big names shedding value despite the vigorous hip-thrust of massive Chinese stimulus measures beefing up the iron ore price.

The three biggest Resources players on the market were all down this morning. BHP (ASX:BHP) shed 2.5%, Fortescue (ASX:FMG) fell 2.3% and Rio Tinto (ASX:RIO) was off by 2.65%.

At lunchtime, the market sectors looked like this:

Health Care was performing well, with big players Cochlear (ASX:COH) and ResMed (ASX:RMD) adding 2.9% and 2.0% respectively.

InfoTech was also performing strongly, thanks to tidy gains from WiseTech Global (ASX:WTC) and Life360 (ASX:360), up 1.2% and 1.6% in that order.

And in data news, we got the September housing numbers this morning, and they’re showing that home prices rose in that month – no surprise there, really – taking the national average price for a home to $807,110.

The data from Corelogic shows that’s an increase of 0.4% for the first month of spring, moving the 12 month climb to 6.7% – the take home from that being that the market is still climbing, but the pace is somewhat slower than it has been.

That’s largely due to an increase in the number of homeowners looking to sell, as the ongoing yoke of high interest rates is pushing more and more owners to tip out.

NOT THE ASX

Overnight, the S&P 500 was up by 0.4%, making it four quarters in a row of gains – its longest winning streak since 2021.

The blue chips Dow Jones rose by 0.04%, while the tech heavy Nasdaq climbed by 0.38%.

“We expect the fourth quarter to be quite similar to the third quarter – elevated volatility, but with a strong finish,” said Emily Bowersock Hill at Bowersock Capital.

In a speech last night, Fed Reserve Chair Jerome Powell gave markets a boost, saying the US economy is looking “strong overall” and the job market is solid.

He also said that inflation seems to be settling down towards that 2% target, but didn’t commit to any upcoming rate cuts.

“We’re not locked into any plan just yet. There are risks on both sides, and we’ll be making decisions as we go.

“We will do what it takes in terms of the speed with which we move,” Powell added.

Friday’s employment report in the US will now be the next focus as it will affect how the Fed goes about setting interest rates.

In US stock news, automaker Stellantis dropped by 12.5% after the company issued a serious warning about its North American business, causing other auto stocks to fall as well.

Meta is still riding high from its developer conference last week and its shares climbed nearly 1% last night after an analyst raised its price target from US$570 to US$620 (versus current price of US$572.44).

Boeing is still struggling as the factory worker strike enters its third week with no end in sight, and talks have stalled. Shares dropped 2.75%.

Nvidia fell by as much as 2% before rebounding after a Bloomberg report on Friday stating that Beijing is encouraging Chinese companies to purchase chips from local makers instead of Nvidia’s popular GPUs.

And Elon Musk’s decision to pay US$44 billion for The Social Media Platform Formerly Known as Twitter is looking even more like a terrible investment, after Fidelity’s Blue Chip Growth Fund revalued its stake in the company at about US$4.19 million, marking a huge 78.7% drop from the US$19.66 million it originally invested.

Fidelity’s revision values Musk’s social media microphone at just US$9.4 billion – well below 25% of the pricetag Musk coughed up two years ago.

In Asian market news, yesterday was one of the biggest in Chinese market history, with the markets there banking the best day they’ve had in more than 15 years as Beijing’s housing stimulus packages excited the market.

“Fevered trading was noted in Shanghai, Shenzhen and Beijing on Monday — the shortest-ever span of time in which stock trading hit the one-trillion yuan mark in the country’s history,” our friends at The Australian reported this morning.

That huge rush might also have had something to do with the markets in China going on an extended break this week, with China essentially closed for business over the next three days, and then a couple more days next week.

Hong Kong is also closed for a holiday today, leaving Japan’s Nikkei the only big player doing anything in the region today. The Nikkei was up 1.3% at lunchtime.

Annnnd that’s it from me for a while. I’m taking a much-needed holiday. I’ll be back… probably.

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for October 1 [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Name Price % Change Volume Market Cap WEL Winchester Energy 0.002 $100.0 279,662 $1,363,019 IBX Imagion Biosys 0.063 $57.5 1,480,140 $1,425,862 BLZ Blaze Minerals 0.006 $50.0 1,607,696 $2,514,233 CCZ Castillo Copper 0.006 $50.0 3,015,396 $5,198,021 IBG Ironbark Zinc 0.003 $50.0 452,378 $3,667,296 WML Woomera Mining 0.003 $50.0 157,448 $3,250,278 RGT Argent Biopharma 0.5 $42.9 15,485 $16,941,961 LM8 Lunnon Metals 0.225 $36.4 3,137,986 $36,377,343 CR9 Corella Resources 0.01 $25.0 275,530 $3,720,739 OVT Ovanti 0.005 $25.0 5,494,253 $6,225,393 5EA 5E Advanced 0.091 $23.0 1,774,811 $24,679,821 ZMM Zimi 0.011 $22.2 171,025 $1,139,982 REC Recharge Metals 0.034 $21.4 440,821 $3,911,319 TOE Toro Energy 0.285 $21.3 3,751,297 $28,266,234 DOU Douugh 0.006 $20.0 1,000,000 $5,410,345 LMG Latrobe Magnesium 0.038 $18.8 1,547,298 $75,153,196 PV1 Provaris Energy 0.019 $18.8 233,243 $10,095,477 ATC Altech Battery 0.045 $18.4 6,809,244 $71,587,842 PEC Perpetual Resources 0.01 $17.6 33,431,087 $6,256,259 AR3 Aust Rare 0.14 $16.7 838,608 $18,955,649

Lunnon Metals (ASX:LM8) has revealed that it has identified a new gold zone from surface at its Kambalda gold and nickel project, with fresh significant, near surface, high-grade intercepts from the current diamond drill and in-fill reverse circulation program returning 23m at 16.61g/t Au from surface including 6m at 62.47g/t Au from 17m in hole FOS24RC_056, and 13m at 4.10g/t Au from 3m in hole FOS24RC_023.

5E Advanced Materials (ASX:5EA) was rising on news that it has received a non-binding letter of interest from the Export-Import Bank of the United States (EXIM), expressing potential for the creation of a debt facility to backstop project debt financing of up to $285 million, which would be utilised for commercial scale development and construction of 5E’s Boron Americas Complex, under the Make More in America Initiative.

Provaris Energy (ASX:PV1) was up on news that it has entered into a binding Joint Development Agreement with Yinson Production to develop storage tank solutions for the bulk storage and marine transportation of carbon dioxide. The Collaboration will also assess the potential for other hydrogen derivatives such as ammonia, combining the track records of both companies in that area of engineering solutions.

Altech Batteries (ASX:ATC) has announced that its first CERENERGY ABS60 battery prototype is online and operating successfully, with the unit “passing all physical tests with flying colours”. Altech reports that the prototype was installed at its joint venture partner Fraunhofer IKTS’ test lab in Germany, integrated into a specially designed battery test station that enables continuous daily charging and discharging cycles to assess the battery’s efficiency, stability, and overall performance under real-world conditions.

Exploration at Perpetual Resources’ (ASX:PEC) Isabella Lithium Project has confirmed several spodumene-bearing pegmatite trends stretching up to 800 metres, supported by new artisanal workings. Multiple spodumene occurrences have been found, with lab results pending. Before the project was acquired, rock samples showed high lithium grades of up to 5.62%. The Isabella site is close to two established spodumene projects: Atlas Lithium’s Das Neves Project, which is building a lithium processing plant, and Sigma Lithium’s advanced Sao Jose Project. Perpetual expects to share preliminary rock chip results in the next three weeks.

Earlier, NickelSearch (ASX:NIS) was up on news that it has commenced reconnaissance work at the recently acquired Mt Isa North project, with geologists onsite prepping for the company’s maiden drilling campaign. Rock chip and grab samples collected and assayed during the due diligence site visit returned copper, gold and silver grades including 24.8% Cu & 1.23g/t Au, and 30.0% Cu & 64.7g/t Ag from different areas of the project.

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for October 1 [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap RNE Renu Energy 0.001 -50.0 2,502,764 $1,608,268 FHE Frontier Energy 0.12 -45.5 9,950,546 $113,034,561 LNR Lanthanein 0.003 -25.0 1,111,109 $9,774,545 NTM NT Minerals 0.003 -25.0 24,392 $4,069,612 OAR OAR Resources 0.0015 -25.0 5,304,895 $6,601,669 TTI Traffic Technologies 0.003 -25.0 2,683,334 $3,891,541 NSM North Stawell 0.014 -22.2 40,000 $2,893,964 AKN Auking Mining 0.004 -20.0 1,000,000 $1,762,851 CTO Citigold Corp 0.004 -20.0 1,581,154 $15,000,000 TYX Tyranna Resources 0.004 -20.0 250,000 $16,439,627 BSX Blackstone 0.03 -18.9 599,429 $19,533,666 AHN Athena Resources 0.005 -16.7 162,978 $6,422,805 ICE Icetana 0.02 -16.7 197,672 $6,351,082 ICU Investor Centre 0.005 -16.7 58,032 $1,827,068 LPD Lepidico 0.0025 -16.7 318,223 $25,767,375 NAE New Age Exploration 0.005 -16.7 26,597,642 $10,763,393 PRM Prominence Energy 0.005 -16.7 120,000 $2,335,058 VML Vital Metals 0.0025 -16.7 7,397 $17,685,201 MKR Manuka Resources 0.029 -14.7 820,351 $26,512,101 SRR Sarama Resources 0.029 -14.7 2,081,567 $5,671,953

ICYMI – AM EDITION

Vertex Minerals (ASX:VTX) has acquired a Boart Longyear LM90 underground drill rig as part of its strategy to advance exploration drill works at the high-grade Reward gold mine.

The plan is to advance exploration below the existing resource, particularly focussing on the Fosters target and South Star prospect area along with the ‘Reward mid depths’ target which is around 80-200m below the Amalgamated Adit, where drilling has only reached 50m below.

“This is an important development for Vertex and we’re excited to get started with targeted drill works that have the potential to unlock significant value from the project,” executive chairman Roger Jackson said.

“Our analysis has shown that it is significantly cheaper, safer and more practical to drill the Reward mine from underground, which is exactly what the LM 90 allows us to do.

“With an extensive framework of priority drill targets already set out, we look forward to advancing exploration and building on what is already an exciting resource at the Reward mine.”

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.

At Stockhead, we tell it like it is. While Vertex Minerals and Altech Batteries are Stockhead advertisers, they did not sponsor this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.