Rabobank says the sun is shining brightly on Aussie agriculture in 2022 – here’s the stocks that could benefit

Pic: Getty

Global agribusiness bank Rabobank reckons Australia’s agricultural sector is set for another profitable year ahead, with the gross value of agricultural production on track for a fourth consecutive year of, uh, growth.

In its flagship annual Australian Agribusiness Outlook for 2022 report classically called ‘Making Hay While the Sun Shines’, the bank says a ‘stellar’ 2021 saw some agricultural commodity prices and production volumes reaching record levels.

This meant recovery from the crippling 2017-2019 drought continued and that the sector is positioned for a strong year ahead – and can prepare for when the sun isn’t shining so brightly.

Basically this means preparing for an increase in margin pressures (when global prices decline and Australian farm returns come under pressure), diversifying markets and trading relationships, and equipping farm businesses for future droughts and climate change.

2021 was a blue moon year

RaboResearch senior commodities analyst Dr Cheryl Kalisch Gordon said in 2021 there was a combination of drought and adverse weather in key cropping regions around the world, strong stockpiling demand in the face of potential food shortages along with Covid-induced labour shortages which impacted intensively-produced agri products and transport.

“This delivered clouds to agriculture sectors in many regions of the world and a silver lining for Australian agriculture,” she said.

“This second straight year of increasing commodity prices coincided with again favourable to very-favourable Australian production conditions. And for those commodity sectors where production has been lower, high pricing still delivered strongly profitable positions.”

‘South Australia floods spark food shortage fears in WA, Darwin & remote towns

Businesses warn of the biggest supply chain disruption in ‘living memory’ after flooding cuts major transport links’

“This is a very serious situation”#ClimateCrisis #foodhttps://t.co/qNIExErcEB

— Jim Baird (@JimBair62221006) January 30, 2022

Supply chains are a bit sticky

Dr Kalisch Gordon expects another favourable year ahead for Australian agriculture despite supply chain challenges from labour shortages due to COVID and crazy flooding cutting railways that supply goods between South Australia and Western Australia.

“We start 2022 with the Australian food supply chain under unprecedented pressure, supply chain disruption and bottlenecks being felt across the board – from access to inputs at the farm level through to consumers accessing food on supermarket shelves,” Dr Kalisch Gordon said.

And the impacts on supply chains are expected to linger at least through the first quarter of the year.

“We also expect some of the heat to come out of prices for a number of commodities in 2022 as supplies are renewed globally, stock levels are increased and demand tempers,” Gordon said.

“However, we expect prices to remain at levels above the five-year average for our main agricultural commodities.”

The Rabobank Rural Commodity Price Index – which tracks local prices of key commodities in Australian dollar terms – is forecast to ease from record highs reached in December 2021 over the course of this year – but will still sit five per cent above the five-year average (and 16 per cent above the pre-COVID five-year average) by the year’s end.

“Triple road trains, which are usually banned for freight transport between South Australia and Western Australia, will be allowed as an emergency measure to address supply-chain problems caused by a ‘one-in-200-year’ weather event.” https://t.co/7NWmF1QTGC

— Eliza Berlage (@verbaliza) February 2, 2022

Don’t forget about geopolitical tensions

The tight global market for agricultural commodities has shielded us somewhat from the impact of losing China as a buyer in 2021, but geopolitical tensions are still a challenge for global supply chains.

“As markets unwind, we expect Australia may need to work harder on diversifying into alternative destinations,” Dr Kalisch Gordon said.

And the report said there is also the potential for market fallout from current tensions between Russia and Ukraine, which could “deliver exaggerated volatility in markets ranging from wheat through to oil and fertiliser.”

The 2014 Crimean conflict saw CBOT #wheat prices rise 15% between late Feb & Mar. In early 2022, even prior to any conflict, prices are already 10% higher. If exports out of Ukraine are disrupted, Australia may see further increased demand for wheat from Asia in 2022 #agchatoz pic.twitter.com/IqgEQiSYOE

— Dennis Voznesenski (@Voz_Dennis) January 24, 2022

Production outlook is mixed

“Very favourable seasonal conditions in 2021 – and in some cases record rainfall – have provided a beneficial start to 2022 for cropping and pasture prospects, due to good soil moisture,” Gordon said.

“That said, at this point, we can’t expect a repeat of the record grain and oilseed harvest we’ve seen for the 2021/22 season.

“Although for livestock, we do expect year-on-year lifts in slaughter numbers for both cattle and sheep, given the extended period of good seasonal conditions we’ve seen in most regions that have enabled some rebuilding of stock numbers.”

The report also flagged that milk production was likely to lift, but only in the second half of the year.

And cotton production is on track to continue rising to an 85 per cent increase on last year.

But expect some inflation headwinds

While it’s a generally positive outlook, Rabobank reckons there’ll be some headwinds, mainly around the Omicron variant and also “the prospect of Rho, Sigma or Tau delivering the next blow.”

On top of this, Gordon said there’s the pervasive challenge of inflation, “which continues on one of the steepest rises in 30 years.”

“Additionally, we expect there will be global policy tightening around economic stimulus measures that have been in place during the pandemic, which will be designed to moderate demand,” she said.

“Getting the policy settings on reducing stimulus and managing inflation will be critical to maintaining economic growth and consumer demand in many economies, and failure to get this right could curb demand in some of our markets for some, especially more discretionary, purchases.”

How are agriculture stocks looking right now?

| Code | Company | Price | % Year | % Six Month | % Month | % Week | Market Cap |

|---|---|---|---|---|---|---|---|

| NUF | Nufarm Limited | 5.59 | 13% | 28% | 15% | 29% | $1,766,802,444.75 |

| WLD | Wellard Limited | 0.115 | 83% | 58% | 22% | 15% | $55,781,282.76 |

| BGT | Bio-Gene Technology | 0.22 | 57% | 42% | 7% | 10% | $35,390,069.82 |

| WOA | Wide Open Agricultur | 0.665 | -10% | -19% | -6% | 9% | $84,606,570.18 |

| NAM | Namoi Cotton Ltd | 0.46 | 59% | 18% | -2% | 8% | $79,167,905.78 |

| 1AG | Alterra Limited | 0.029 | -33% | -34% | 0% | 7% | $8,333,288.22 |

| AAC | Australian Agricult. | 1.495 | 33% | 8% | 1% | 5% | $895,108,619.30 |

| WNR | Wingara Ag Ltd | 0.078 | -43% | -41% | -13% | 4% | $13,692,315.31 |

| FSF | Fonterra Share Fund | 3.38 | -20% | -4% | -3% | 2% | $351,254,642.94 |

| GNC | GrainCorp Limited | 7.25 | 76% | 38% | -12% | 2% | $1,723,282,878.84 |

| CGC | Costa Group Holdings | 2.92 | -27% | -10% | -4% | 1% | $1,346,698,000.90 |

| TSN | The Sust Nutri Grp | 0.15 | -65% | -59% | -25% | 0% | $19,297,021.60 |

| DBF | Duxton Farms Ltd | 1.705 | 28% | 20% | 13% | 0% | $73,881,840.20 |

| RIC | Ridley Corporation | 1.48 | 63% | 30% | -1% | -1% | $463,267,713.75 |

| SHV | Select Harvests | 5.46 | 3% | -32% | -12% | -1% | $679,699,887.25 |

| ELD | Elders Limited | 11.01 | 0% | -3% | -10% | -1% | $1,740,019,502.88 |

| AAP | Australian Agri Ltd | 0.028 | 0% | -13% | 4% | -3% | $8,542,785.33 |

| A2M | The A2 Milk Company | 5.26 | -50% | -13% | -4% | -3% | $3,963,689,294.24 |

| AHF | Aust Dairy Group | 0.054 | -11% | 0% | -8% | -4% | $28,844,756.58 |

| AHF | Aust Dairy Group | 0.054 | -11% | 0% | -8% | -4% | $28,844,756.58 |

| LGP | Little Green Pharma | 0.55 | -30% | -29% | -8% | -5% | $100,197,082.15 |

| RGI | Roto-Gro Intl Ltd | 0.018 | -67% | -50% | -10% | -5% | $6,166,670.35 |

Nufarm (ASX:NUF)

The global crop protection and seed technology company says revenues for Q1FY22 have increased 36 per cent compared to Q1FY21, supported by favourable weather conditions – particularly in Australia – and the continuation of strong customer demand.

However, Nufarm did flag that it’s experiencing upward pressure on costs due to raw material costs and global logistics challenges which is being offset by the increased revenues.

“While agricultural conditions and the outlook for soft commodity prices remain favourable, Nufarm expects earnings in FY22 will be heavily weighted to the first half of the financial year and is increasingly confident of revenue and earnings growth for the full FY22 financial year,” the company says.

Wellard Limited (ASX:WLD)

The livestock company reported cash flow of negative US$1.5 million from operating activities in the December quarter – which it said was impacted by the late payment of a US$4.0 million customer invoice which was due on 30 December 2021 but was received on 5 January 2022.

“Wellard continued to achieve excellent ship availability during the quarter, though utilisation came under pressure in late December as a result of the well-publicised decline in live cattle exports from northern Australia,” executive chairman John Klepec said.

“It has been a consistent theme over the past 12-18 months that the supply of breeding cattle out of southern Australia, New Zealand and South America has generated good demand for our vessels to service Northern Asian demand for dairy and beef breeder cattle, while shipping activity out of northern Australia continued to be depressed due to historically low cattle availability and the resultant record Australian cattle prices.”

He said the theme has continued this quarter, as freight rates ex-Australia “remain depressed and are under further pressure from attempts by some supply chain participants in northern Australia to reinvigorate their margins.”

But Klepec did note that trade in live cattle from South America to Turkey and the Middle East is showing encouraging signs with increased activity and forward enquiry.

Wingara Ag (ASX:WNR)

Wingara specialises in the processing, storage and marketing of agriculture produce for export markets, and enjoyed a solid December quarter.

The company reported operating cash receipts of $14.5 million, up 42% on Q3 FY21 and 19% on prior quarter, along with positive operating cash flow of $0.2 million at the end of Q3 FY22, up 28% on pcp and 44% on prior quarter.

But CEO James Whiteside said Omicron did impact business, with JT Tanloden production sales volume output of 21,675 MT up 43% on the pcpc but down 11% on the prior quarter – and the Austco Polar volume of 406k cartons down 4% and 19% on the pcp and prior quarter respectively.

“This has been reflected in cancelled work shifts, unavailability of key personnel and recruitment of new staff substantially compromised,” he said.

“In addition, substantial delays and cost increases in international sea freight have impacted margins and delays are being experienced in securing plant spare parts and consumables. The subsequent impact on revenue is putting significant pressure on EBITDA results.”

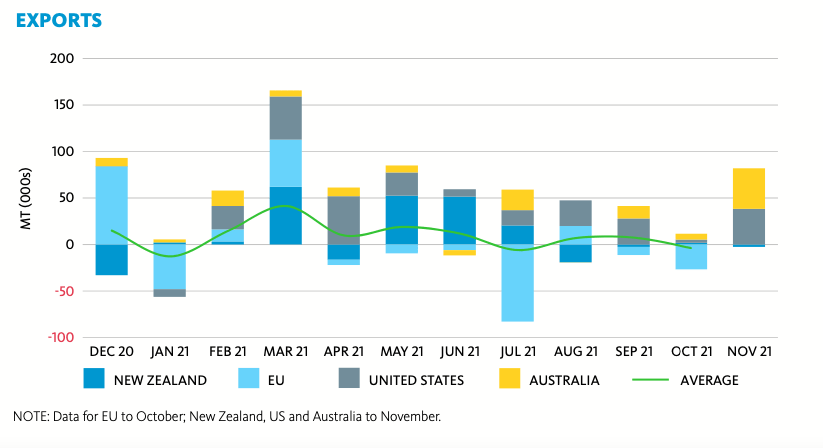

Fonterra (ASX:FSF)

The New Zealand-based dairy co-operative said last month that Australia and US monthly exports continued to grow while New Zealand and EU monthly exports declined.

And while China and Asia monthly imports declined, the Middle East and Africa, and Latin America monthly imports were up.

“Fonterra New Zealand milk collection for December was 173.4 million kgMS, down 5.3% on December the prior season,” the co-op said.

“Fonterra Australia milk collection for December was 11.3 million kgMS, down 0.6% on December last season.”

CEO Miles Hurrell said in general, demand globally remains strong.

“Overall, global milk supply growth is forecast to track below average levels, with European milk production growth down on last year and US milk growth slowing due to high feed costs,” he said.

The co-op is also keeping a close eye on growing inflationary pressures impacting on operational costs, the increased potential for volatility as a result of high dairy prices and economic disruptions from COVID-19 – particularly as governments respond to the rapid spread of the Omicron variant.

Australian Dairy Nutritionals Group (ASX:AHF)

This dairy group reckons its farms are on track for a second season of excellent weather conditions in southwest Victoria.

“Demand for organic milk also appears to be increasing after some softening of the market following the exit of Organic Dairy Farmers of Australia,” the company said.

The group is planning to launch an organic A2 fresh milk in selected Victorian Woolworths stores in mid-February under the Camperdown Dairy brand.

Duxton Farms (ASX:DBF)

Duxton says its crop harvest is expected to continue well into January 2022 given the delayed start and slower harvest conditions, but despite quality downgrades, it’s recording higher yields compared to last season and expects revenue this quarter of around $11m.

On the livestock side, the company saw reasonable pricing for the Merino wool portion during the December quarter, but lower pricing for crossbred wool.

“Sale of livestock is ongoing with good to exceptional pricing with additional livestock to be purchased as attractive pricing opportunities arise,” Duxton said.

Plus, the Australian Eastern Young Cattle Indicator (EYCI) rose substantially over the quarter finishing December at $11.64/kg – around 48% higher than the same time last year.

Lamb prices at the end of the quarter are approximately 11% higher than compared to the same time last year with the Australian Eastern States Trade Lamb Indicator (ESTLI) finishing the quarter at $8.54/kg.

Select Harvests (ASX:SHV)

The almond company released a crop update on Monday, with harvest expected in mid-Feb.

“Following the strengthening of global almond prices in the second half of 2021, pricing has recently returned back to similar levels as those reported last year,” the company said.

“Market pricing continues to remain volatile.”

SHV says continuing global shipping congestion is causing ongoing delays to customer deliveries leading to higher levels of physical stock holdings and that these factors have caused pricing to reduce to current levels.

“While global almond pricing has reduced in recent months, Select remains in a strong position given its lower quartile cost of production and investments in processing and value add technology,” MD and CEO Paul Thompson said.

“The macro for almonds remains strong and we expect pricing to improve in the short to medium term.”

The company also said that it continues to experience positive demand from export and domestic customers, with around 10% of its forecasted 2022 crop is committed to targeted export markets.

Australian Agricultural Projects (ASX:AAP)

Olive player AAP said in its December quarterly that it’s noticing the impact of COVID-19 on orchard operations by way of increased cost of agricultural supplies, especially fertiliser, extended delivery times and the well-published shortage of labour in regional areas.

“Management continues to monitor the impact of COVID-19 on operations and has adjusted its planning by allowing longer lead times on all projects,” the company said.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.