The White House: Cheap, dodgy and dangerous – China’s property stocks have a certain sex appeal

Via Getty

In this series, global equities portfolio manager James White from Lessep IM, ditches micro and macro and embraces “The Meta” perspective.

Lessep IM runs a core portfolio of 40-50 stocks that capture the opportunities in productivity trends and reflect investments in both the drivers of productivity and the beneficiaries of productivity. James also aims to run a long-tail of stocks that have the potential to capture a greater share of new or existing markets.

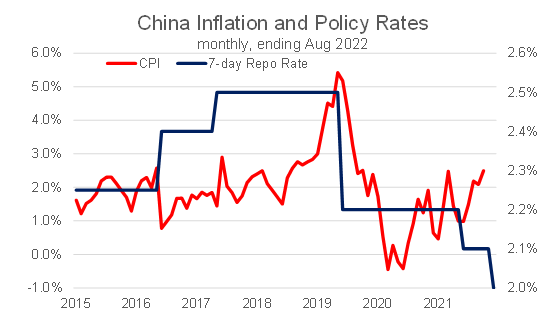

China’s central bank on Monday surprised, cutting benchmark loan rates in an attempt to boost an economy battered by the government’s strict zero-Covid policy and a slump in the property market.

The deeper cut to the mortgage reference rate underlines efforts by policymakers to stabilise the property sector after a string of defaults among developers and a slump in home sales hammered consumer demand.

China announced a cut in its policy interest rates, lowering the 7-day reverse repo rate, the rate at which it provides liquidity to banks, to 2.0% from 2.1%. The Medium-term Lending Facility was cut from 2.85% to 2.75%.

This was already an unexpected move. China has been cautious with its monetary policy, and despite global headwinds, has resisted aggressive stimulus.

The move reflected concerns that, despite inflation being likely to rise, the slowdown in economic activity was a more pressing concern.

By example, industrial production, retail sales, and Fixed Asset Investment, all decelerated in July from their June growth.

Investment Implications

While it may be too early to make sweeping predictions about the future pace of a Chinese recovery, are there palpable investment opportunities emerging as authorities look to increase the pace of growth?

Authorities in China have been sanguine, when compared to authorities in the West, as regards government support through the pandemic.

This also reflects concerns about the level of debt in the economy, and the political environment. But it’s worth considering the opportunities that might exist if growth is more aggressively supported.

China Assets

The China A50 Index is at pre-pandemic levels and a third lower than highs from the beginning of 2021.

Key component parts, such as banks and financial services, trade at high discounts, relative to history.

For instance, China Construction Bank trades at 0.4x Book, compared to an historic average of closer to 0.6x Book.

Cheap, a little dirty and rather attractive

A fan of the occasional crackdown, President Xi Jinping cracked down on China’s property sector mid-Covid and the country’s developers have been struggling ever since.

Projects are stalled, homebuyers who paid in advance are boycotting their mortgage repayments and the world – with Evergrande but a memory – is rubbing its hands in anticipation of carnage.

China’s real estate sector accounts for roughly a third of Chinese economic output, it’s connected to everything – domestically and, think of a country like Australia – even globally.

So yes, in hopes of turning things around, the country’s central bank slashed its 5-year mortgage rate by the equal-most on record, Monday.

That’ll tighten borrowing costs on new mortgages, which in turn might lift demand and even boost the sector.

But much importantly, Hong Kong’s Hang Seng Mainland Properties index lifted on Monday, after the Chinese government appeared to guarantee access to emergency loans in a bit of a blank cheque solution to helping get unfinished property projects over the line.

Here are some Gregor found on Monday for your viewing pleasure:

China demolishing unfinished buildings.. beautiful Keynesianism at work pic.twitter.com/y9LE4pYQUG

— Igor Schatz (@Copernicus2013) August 19, 2022

Real estate companies, a clear beneficiary of policy easing, are even cheaper than the banks that fund them.

China tech

China’s technology stocks offer substantial opportunity, relative to recent, past performance.

The Nasdaq China Technology Index is down 67% from its highs in early 2021.

This reflects a combination of the slowdown in the economy, concerns over government intervention in the sector, and a shift to Hong Kong listings.

Given the uncertainties, it’s not yet, from a risk-adjusted perspective, worth investing in these opportunities. More clarity over both the support for the economy, and likely regulatory moves, is required to make positive decisions.

Commodities

A simpler place to start will be commodities. An increase in monetary and fiscal support for the Chinese economy has led to an increase in commodity consumption and prices.

Of course, increased Chinese demand for commodities at a time when inflation has risen across the developed world will challenge markets.

Indeed, this will be the case, with or without, more aggressive policy responses. The IEA estimates China’s oil consumption will fall in 2022 as a consequence of lockdowns. This lower Chinese demand has been important for limiting developed world oil price rises. But as China opens up, regardless of price, and stimulus, demand will rise. A double whammy of opening up, and stimulus, would pose new problems for the global economy.

With mining stocks lower than their recent peaks, this might be a good place to participate in a more aggressive Chinese stimulus package.

It may be too early to make an assessment of the scale of China’s efforts to increase economic growth. But it does feel as though some opportunities may arise in the next six months, dependent upon risk appetite.

Even from a defensive perspective, global equity investors need to be thinking about the impact of increased resource competition on the global economy. A higher allocation to commodity producers may be sensible at this stage.

The views, information, or opinions expressed in the interview in this article are solely those of the writer and do not represent the views of Stockhead.

Stockhead has not provided, endorsed or otherwise assumed responsibility for any financial product advice contained in this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.