Taking the profit on Pro Medicus? Nice one. You just broke the 1st Rule of Compounding Growth

Shhh. Via Getty

We miss Charlie Munger.

This was sent to me last week by Andrew Page, founder and managing director at the Strawman Index as we traded Mungerisms.

The strong right arm of Warren Buffett has loads of great quotes, but for an investment boffin like Pagey, this one is a standout for the simple fact people like me just don’t get it.

“The first rule of compounding: never interrupt it unnecessarily.”

— Charlie Munger

Yup. Charlie might be gone but his homespun wisdom retains all its original potency to make me feel less rich and more stupid.

I know what compounding is. But I usually associate it with problems, lies, weight gain and unpaid parking fines.

So, I asked Andrew to expound.

Which he didn’t have to do, but he has done so with great alacrity below.

So a quick thank you to him.

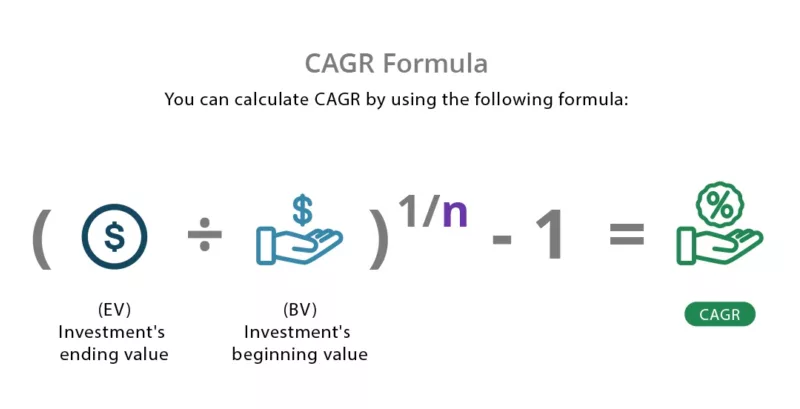

Getting your CAGR on

Before we start…

According to math:

The compound annual growth rate (CAGR) is the rate of return (RoR) that would be required for an investment to grow from its beginning balance to its ending balance, assuming the profits were reinvested at the end of each period of the investment’s life span.

Pagey says the math behind compounding “is easy enough, but the intuition is anything but.”

I would take issue with that first statement. But then I found a picture. So. …

Pagey says:

“If you can find an investment that compounds at 20% per annum… then the gain you make in year 10 is greater than the entire amount you started with and the total value has grown more than six-fold.”

Sure, he adds, investments like this don’t grow on trees – although not as rare as you might think – but “you only need one or two to make all the difference over your investing career.”

“Even if all the other decisions you make are just truly awful.”

Positive asymmetry

“In a recent podcast, investor and author Gautam Baid put it this way:

“Compounding is convex on the upside and concave on the downside. Positive asymmetry. Few understand this but the day you do, it will change your investing perspective forever.”

“The example he gave was an investor that bought one share that compounded at 26%pa and another that compounded at negative 26%pa. You could forgive someone for assuming the end result is a wash, but after 10 years you’d actually have compounded your money at over 17%pa,” Andrew says.

“What’s wild is that even if you’re wrong 75% of the time, you can still do well with just one big winner.”

“For instance, if our investor splits their money across four investments, one of which compounds at 26%pa, and the other three lose 26%pa, you still come out with a 10% average annual return after a decade.”

But, as our mate Charlie says, this only happens if you do NOT interrupt the compounding process.

Compoundus Interruptus

“Gautam illustrates this by assuming that our investor trims their winning position by 10% each year. In the first example, the average annual return drops from over 17%pa to just 8%pa.

“Over a decade, the dollar value difference is gigantic. Obviously, if you trim more, or your strike rate is lower, the difference becomes even more extreme.”

Pagey says, all of this is easier said than done, of course.

“The trouble is that, in these types of examples, you quickly find yourself with position weightings that would give any right-thinking portfolio manager a heart attack.

“In our examples, it only takes a few years before your winning stock becomes close to 90% of your total portfolio. Could you really have enough conviction to hold so much of your wealth in just one basket?

Amateur Medicus

“As someone who repeatedly sold down their holding in ProMedicus (ASX:PME) — a position that would be otherwise closing in on a 100-bagger at this point — I (try to) find some solace in this.

“And I try to remind myself that had I not sold other ‘winners’, I’d be in a far worse situation now — selling down my Pointerra (ASX:3DP) shares as they went from 4c to 90c was absolutely the right thing to do.”

So things won’t ever be as clear cut in the real world. But, according to Andrew, the point here remains valid.

Specifically, don’t sell down your winners just because you’re sitting on a profit — even a large one.

“Yes, by all means trim back your position if the price is just plain silly, and not justified by genuine and significant improvements in the underlying business.

“But if you’re seeing strong sales traction for a business that has a significant market opportunity, is able to self-fund growth AND generate good free cash flows along the way, you want to think very, VERY carefully about locking in any profits.

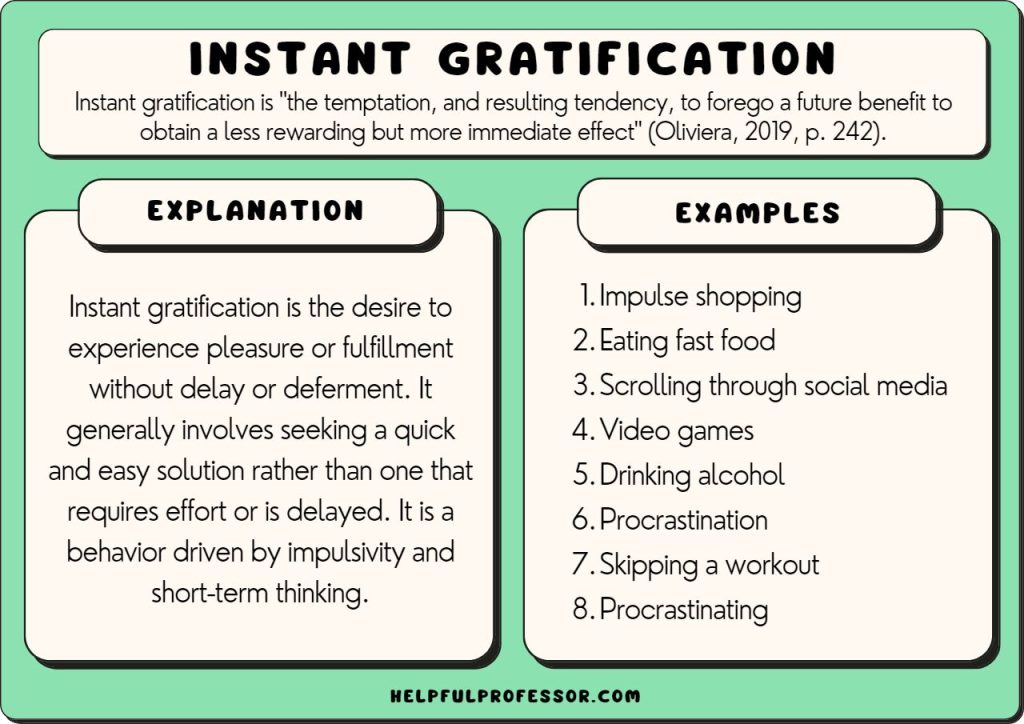

“It’ll feel good at the time, but it could be something you later regret,” Andrew says, having apparently forgotten the first law of instant gratification:

It’s so much more fun!!

Andrew Page is the founder and managing director at the Strawman Index.

The views, information, or opinions expressed in the interview in this article are solely those of the broker and do not represent the views of Stockhead.

Stockhead has not provided, endorsed or otherwise assumed responsibility for any financial product advice contained in this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.