Investment grade fixed income on comeback trail as higher yields offer competitive returns

Pic:Getty Images

- Yields that risk-free benchmark securities trade at important for valuation

- Strong yields on offer from investment grade fixed income

- Strong inflows into high grade fixed income and traditional fixed income assets

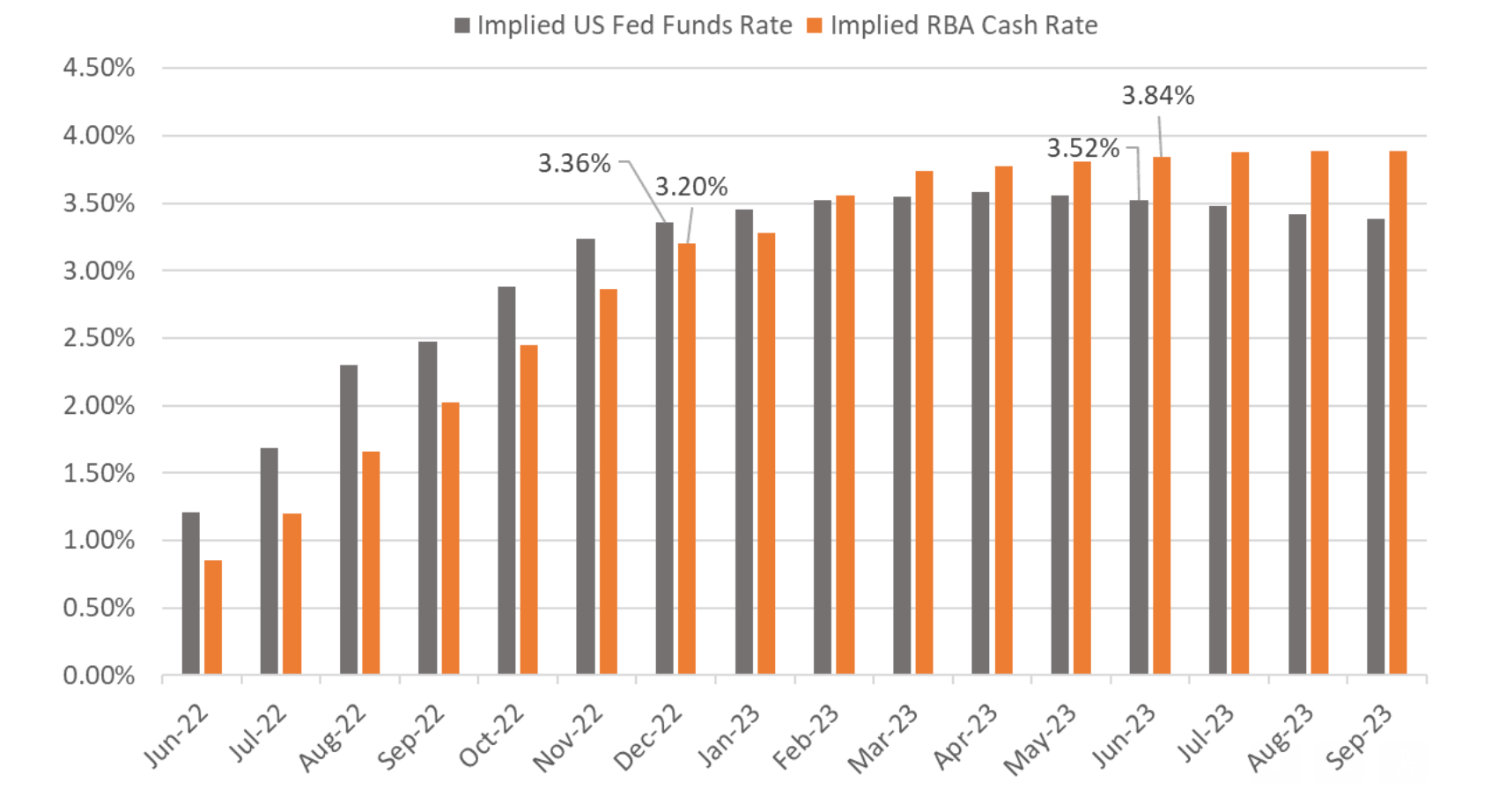

Aussie fixed income investors have had a rough ride in recent years with interest rates at record lows of 0.1%. But while the Reserve Bank of Australia (RBA) was saying there would be no interest rate rises before 2024, rising inflation has forced a tightening of monetary policy in 2022.

The 50-basis point increase we saw in June and the 25-basis point increase in May has pushed the official cash rate to 0.85%.

The RBA is essentially an inflation-targeting bank. Governor Philip Lowe forecast inflation could reach 7% by the year’s end, well beyond the target of 2-3%.

Economists predict further rate rises in coming months, including another bumper 50 basis point hike in July, which would leave the cash rate sitting at 1.35% as the RBA moves to bring inflation under control.

Broad sell-off across asset classes

While inflation and associated interest rate rises has seen a broad sell-off in equity markets, there has also been a broad sell-off in bond markets at the same time pushing yields higher.

It is an unusual phenomenon to see both bonds and equities fall simultaneously. Basic economic theory teaches there’s an inverse relationship in bonds and share markets.

When there’s prolonged price declines in equities, bond prices generally rise as investors seek a safe haven, but this hasn’t been happening during the latest market drawdown.

BetaShares senior portfolio manager Chamath De Silva told Stockhead that while bonds have historically been a good diversifier for a portfolio, the inverse relationship didn’t always hold.

“The exception to the rule is when inflation is a dominant concern and that has definitely been the case in the past 6 to 12 months,” De Silva said.

He said when inflation is a main concern for market participants and dominates the investment narrative then the focus turns to what central banks will do to curb inflationary pressures.

“As a result, we’ve seen bond yields reprice higher to reflect the more aggressive policy outlook for central banks globally,” he said.

De Silva said anticipation of rate hikes has also weighed on equity markets, primarily through the valuations channel.

“If you think about government bond yields being the foundational valuation building block, the risk-free component and then moving out across the risk spectrum you attach a risk premium on top,” he said.

De Silva said whether for yields on corporate bonds or required rates of return on equities, the yields that the risk-free benchmark securities trade at are very important for valuation across asset classes.

“That has been the prime reason that bonds and equities have both fallen – bonds have fallen on the repricing higher of yields and equities have underperformed largely on the back of compression in multiples associated with the repricing higher in benchmark yields.”

He said this is likely to continue until inflation comes back under control.

Central banks can only do so much to control inflation

De Silva said while cost-push inflation due to supply shortages is also having an impact, central banks have greater influence on demand-push inflation.

“Even if the inflation pressures we’ve seen are caused by supply side factors central banks can only really respond by controlling demand in order to anchor longer term inflation back to their target,” he said.

“At a certain point they will be successful in easing demand and maybe even destroying demand and at that point the market narrative will shift away from inflation fears more toward growth and recession concerns.”

Bonds shine when focus shifts to growth

De Silva said once the narrative shifts from inflation to growth it’s in that sort of environment bonds and equities diversify each other well.

“Once you move away from inflation to growth bond yields tend to fall with expectations of falling nominal GDP, while equities can be challenged by corporate earnings tending to roll over as the economy slows down,” he said.

He said there are signs we are almost at that shift including commodity prices trading with a heavy tone in recent weeks.

“Commodity prices are sensitive to global business cycles and especially if we do see a deterioration in demand, we could see commodity prices roll over that impact inflation expectations,” he said.

“Once that happens, we will see market pricing of interest rate hikes be removed and that will support bonds.

“At the same time if concerns start to impact corporate earnings, that could see equities take another leg lower.”

Signs bonds sell-off slowing

There are signs the bond sell-off could be slowing with investors appearing to be adding more bonds to their portfolios with markets already pricing in much of the rate hikes.

With figures from the US pointing to a not so soft landing as the US Federal Reserve hoped, with slowing growth and forecasts of a recession, there are signs rates may not hike to levels previously forecast.

Co-head of IAM Capital Markets James Shillington told Stockhead interest rates have risen dramatically this calendar year, largely driven by inflationary expectations.

“We are looking at the best part of 10-year highs in government bond yields which have pushed up the entire fixed income yield curve,” he said.

“For the first time in around 10 years you can now buy good quality investment grade bonds with 6% plus yields.

“After Australian Sovereign and Semi-Government bonds, Investment grade corporate bonds are probably the lowest risk sub-sector of the traditional AUD fixed income market.”

Investment grade fixed income making a comeback

Shillington said with strong yields on offer from investment grade fixed income, it is starting to make a return to portfolios.

“It’s been somewhat of an unexciting asset class in the low-rate environment we’ve just been through,” he said.

“But fixed income is now back on the map for self-managed super funds and income seeking investors given where yields are now.”

Shillington said fixed income is moving back to its historical role as a solid incoming producing asset class for investors.

“It’s always been a traditionally reliable asset class for income generation but with the low yield environment we’ve experienced in the last three years it’s made it less attractive,” he said.

Shillington said with investment grade bonds, which are the lowest risk subsector of the credit market, generating returns of 5 to 6%, it’s now worth consideration.

“The mid part of the bank capital structure which is subordinated debt or tier 2 is offering around 6% yield to expected maturity for five years, so you could generate quite an attractive return in our opinion.

Shillington said household names like Transurban Group (ASX:TCL), Lendlease Group (ASX:LLC), Macquarie Group (ASX:MQG) and Australia’s largest private rail freight company Pacific National are offering value and security with competitive corporate bonds.

“High quality corporate bonds, also look attractive compared to the ASX listed hybrid market which appears expensive now versus wholesale over-the-counter securities,” he said.

De Silva said going forward performance of bonds will depend on what hikes are currently priced in and what the RBA does in the future.

“If we feel the RBA will struggle to deliver on the 300-basis point hikes still priced in over the next 12 months then bonds could see a rally,” he said.

“There are reasons to believe the RBA could face headwinds in its ability to hike rates because even though inflation is running quite hot now, if we expect the global economy to deteriorate quite materially Australia won’t be completely immune.”

De Silva said a slowing economy could impact the RBA’s ability to hike as aggressively as has been priced into markets and it may be a good time to look at fixed income assets.

“If you do expect the global economy to slow down, then historically that has always been a pretty good backdrop for fixed income,” he said.

“We are seeing fixed income offer competitive yields even compared to other asset classes like equities for the first time in 10 years and that’s a conversation we are starting to have with our investors.”

He said a lot of investors historically might have been using fixed income as a portfolio balance and volatility suppression building block.

“Now that yields are so competitive, they are starting to look at investment grade credit as their prime income generating building block,” he said.

Bank term deposit rates higher

IAM head of cash products Bianca Burt said the changing cash market has seen banks increase interest in taking deposits from middle market and institutional clients, such as non-for-profit organisations, local governments, associations, schools, and universities.

“What I’ve witnessed over the past three years even before covid-19 is banks were not really interested in taking the middle market and institutional type clients,” she said.

“In the last two to three months we’ve seen a reverse and are wanting to quote on larger parcel institutional type clients.”

She said banks tend to view SMSF and term deposits as more stable funding, but banks are seeking funding.

“The easiest way for them to get large ticket sizes is by issuing term deposits or negotiable certificates of deposits (NCD’s) to the larger end of town,” she said.

“You can get a 12-month deposit now for around 4% and three months ago you were lucky to get 2% so in a short amount of time that has picked up significantly.”

She said IAM has a mix of clients from financial advisors who then have SMSF and individuals to middle market, and institutional clients.

“We’ve seen them take advantage of those higher longer dated deposits so over the past 12 months most clients would roll for three months unsure of what is happening,” she said.

“But now because there is a big range between that three months to six, nine and 12-months clients are taking advantage of higher rates and locking their funds out for longer.”

Franklin Templeton makes case for fixed income

US global investment firm Franklin Templeton chief market strategist and head of Franklin Templeton Institute Stephen Dover is also bullish on fixed income.

“Income is an effective tool to lower the volatility of an investment in this uncertain environment by providing steady cash flow as principal value is fluctuating,” he said.

“Income opportunities exist for investors willing to broaden the potential sources of yield.”

In a recent analysis, Dover shares how high inflation, rising interest rates and a growing risk of a significant economic slowdown underscore the importance of casting a wider net for income generating assets.

He notes while dividend-paying stocks remain an important source of income if inflation remains elevated and central banks respond with higher-than-expected rate increases, investors should consider using short-duration instruments to mitigate interest rate risks.

“High-yield bonds and floating rate notes are good candidates in this environment given their higher nominal yields, low duration and relatively lower volatility,” he said.

“These instruments have better quality and stronger fundamentals than in the past, and unless economic growth falls dramatically, there is likely to be a low rate of defaults.”

Dover said if inflation and rate increases do not rise above current market expectations, there is a case for longer-duration instruments.

“If inflation slows and the economy does not fall into recession, the diversification effect (ballast) of longer-duration government bonds could return.”

Dover said active management will be more critical going forward with higher volatility providing an opportunity to reset allocations.

“Achieving a diversified portfolio will likely include a more creative re-allocation of traditional assets and a wider array of alternative assets,” he said.

“Re-allocating toward your long-term targets can help maintain balance in portfolios.”

Uptick in government bond ETF

De Silva said BetaShares has seen a moderation of flows into equity markets and ETFs with investors becoming more cautious in their asset allocation.

“We’ve seen a paring back of flows into broad equities and thematics with the tech sell off, lingering inflation and growth fears dissuading many investors from some of these more higher beta equity exposures,” he said.

“On the flip side we have seen strong inflows into high grade fixed income and traditional fixed income which has been pretty neglected the past 18 months or so.

De Silva named the Australian Government Bond ETF (ASX: AGVT) as one of BetaShares’ most popular funds of the year.

The fund which invests in a portfolio of high-quality Australian government bonds has seen around $255 million of net flows into AGVT this year, helping push funds under management to $415 million in the Fund.

At Stockhead, we tell it like it is. While IAM Capital Management is a Stockhead advertiser, it did not sponsor this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.