BARCELONA, SPAIN - OCTOBER 28: Mick Jagger and Ronnie Wood of the Rolling Stones are seen in attendance as FC Barcelona debut their limited edition match shirt featuring the Rolling Stones logo during the LaLiga EA Sports match between FC Barcelona and Real Madrid CF at Estadi Olimpic Lluis Companys on October 28, 2023 in Barcelona, Spain. (Photo by Eric Alonso/Getty Images)

I know, the ASX is overbought, but I like it, like it, yes I do.

So begins this week’s strategic appraisal of the stocks in Stockhead-land, brought to you by the head of investment strategy and chief economist at AMP, Dr Shane Oliver.

Now, I know little in the ways of investing, but to my innocent eye that seems a pretty fair assessment.

Those bullish, easy-to-trigger US traders have regained something of that familiar effervescent air about them again – one imagines that with but circa 15 sessions left in which to make good on decisions about inflation, cash rates, tax/loss selling and the tempting tradition of a Santa rally, equity markets could have an exciting remainder of 2023 ahead.

And Dr Oliver advises that enthusiasm should be tempered by a little realpolitik.

“The big rebound in shares has left them technically overbought and at risk of a further consolidation or short term pull back.

“However, further gains are likely into year-end and early next year as inflation continues to ease.”

He notes that share markets on Wall Street and in Europe rose modestly over the last week helped by more good news on inflation reinforcing confidence that global interest rates have peaked.

“The monetary policy environment is turning progressively less threatening, economic indicators remain consistent with a soft landing, geopolitical threats likely take a back seat for a while and positive share market seasonality remains in place with the Santa Rally normally kicking in later this month.

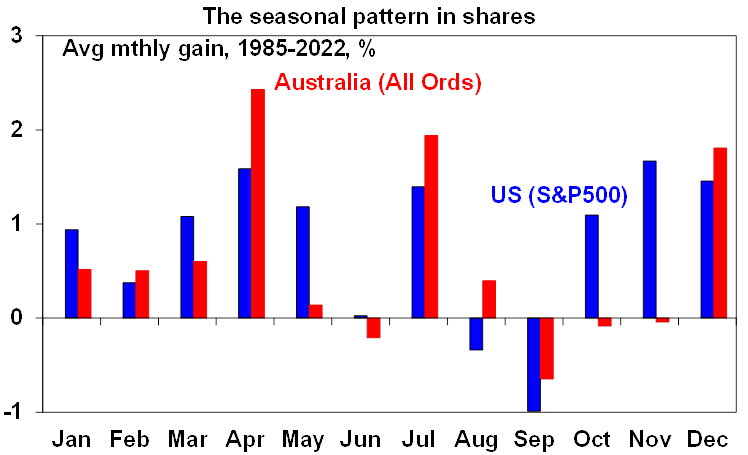

“In terms of the latter, its noteworthy that while November is strong for US shares, seasonal strength for Australian shares usually doesn’t kick in until December.”

Via AMP

“November saw US shares gain 8.9%, which is one of their best Novembers on record, global shares rose 8.1% and Australian shares rose 4.5%.”

A brief ASX all cap re-cap

Australia’s equity markets by contrast rose around 0.3% for the week with strong gains in IT, health and telco shares but falls in resources and utilities.

The good news on inflation resulted in 10-year bond yields falling another 10-20 basis points, Dr Oliver also notes. Oil prices were little changed despite a new OPEC+ oil production cutback as traders doubted that the voluntary cutback will be implemented.

Metal and gold prices rose but the iron ore price fell slightly.

The $A rose above $US0.66 even though the US dollar rose slightly.

The key catalyst for stocks will likely continue to be the expected trajectory of the Federal Reserve’s monetary policy.

Evidence of easing US economic growth has added weight to Wall St bets that the US central bank could wield the axe on rates over yonder as early as 1H next year, setting off the late season rally which has taken the US S&P 500 benchmark index ahead by circa +19.5% year-to-date, not to mention a few points away from a fresh closing high for the year on Friday.

Unflation

The good news on inflation continued over the last week, according to Dr Oliver.

Via AMP

Firstly, Eurozone CPI inflation for November dropped far more than expected to 2.4%yoy with core CPI inflation falling to 3.6%yoy.

“Then US core personal consumption (PCE) inflation fell to 3.5%yoy in October following the earlier reported fall in CPI inflation – which happens to be below the Fed’s 3.7%yoy forecast for year end! In Europe, this is down from peaks of over 10% and 5% respectively,” Dr Oliver notes.

“This is providing increasing confidence that major central banks have reached the peak in interest rates and that rates will be cut next year, which we expect from around mid-year.

“Fed speakers over the last week remained cautious but most were consistent with the Fed leaving rates on hold this month. In fact, normally hawkish Fed Governor Waller flagged the possibility of rate cuts if the decline in inflation continues for ‘several more months’.”

Markets are even betting that the European Central Bank (ECB) boss Christine Lagarde is now more than likely to relax her grip on the bank’s current guidance for annual inflation, implying even the ECB is done with raising the rate flag again for the whole of next year.

That said, Dr Oliver warns… ‘there’s still significant risks’ at play.

Here are the risks AMP is watching:

Sticky services inflation means there is still the risk of more rate hikes or “high for longer” rates

The risk of recession remains high

Uncertainty remains high regarding the Chinese economy and property sector

Geopolitical threats could flare up again

How can we forget US shutdown risk from January 19?

Ongoing risks around a flare-up to involve Iran in the Israel/Hamas war

Numerous elections next year – most notably in Taiwan (which could affect China/Taiwan tensions)

The US Presidential election back-end 2024

And then, of course there’s always a potential surprise visit from the hawks at the global central bank menagerie.

“The risk of another rate hike is perhaps the greatest in Australia and so this could see Australian shares remain a relative underperformer for a while yet,” according to Dr Oliver.

“So, shares are still likely to remain volatile.

“But our base case remains that global and Australian shares can trend up as easing inflation takes pressure of central banks and any recession is likely to be mild. But expect lots of bumps along the way.”

Dr Shane’s Outlook for Investment Markets

“The next 12 months are likely to see a further easing in inflation pressure and central banks moving to get off the brakes. This should make for reasonable share market returns, provided any recession is mild. But sticky services inflation, still high recession risk, China worries and geopolitical risks are likely to ensure a few significant bumps along the way.

“Bonds are likely to provide returns above running yields, as growth and inflation slow and central banks become dovish.

“Unlisted commercial property and infrastructure are expected to see soft returns, reflecting the lagged impact of the rise in bond yields on valuations. “Commercial property returns are likely to remain negative as ‘work from home’ continues to hit space demand as leases expire.

“With the lagged impact of high interest rates appearing to get the upper hand again we now expect national average home prices to fall around 5% in 2024. The supply shortfall should prevent a sharper fall and we expect a wide dispersion with prices still rising in Adelaide, Brisbane and Perth but sharper falls in Sydney and Melbourne.

“A deep recession and sharply higher unemployment would risk pushing prices below their January 2023 low.

“Cash and bank deposits are expected to provide returns of around 4-5%, reflecting the back up in interest rates.

“A rising trend in the $A is likely into next year, reflecting a downtrend in the overvalued $US and the Fed moving to cut interest rates before the RBA.”

Finally, in the immortal words of Keith and Mick (to make of which, what you will):

… I said I know it’s only rock ‘n’ roll but I like it

I said I know it’s only rock ‘n’ roll but I like it

I know it’s only rock ‘n’ roll but I like it, yeah

I know it’s only rock ‘n’ roll but I like it, like it, yes, I do

Oh, well, I like it, I like it, I like it, I like it

I like it, I like it, I like it (only rock ‘n roll’) but I like it

(It’s only rock ‘n’ roll) but I like it (only rock ‘n’ roll) but I like it

(Only rock ‘n’ roll) but I like it (only rock ‘n’ roll) but I like it

(Only rock ‘n’ roll) but I like it (only rock ‘n’ roll) but I like it

(Only rock ‘n’ roll) but I like it (only rock ‘n’ roll) but I like it

(Only rock ‘n’ roll) but I like it (only rock ‘n’ roll) but I like it

(Only rock ‘n’ roll) but I like it, yeah, but I like it

Oh and I like it, ooh yeah I like it

share

Link copied to clipboard

SUBSCRIBE

Get the latest Stockhead news delivered free to your inbox.

It's free. Unsubscribe whenever you want.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.