Picture: Getty Images

Guy on Rocks: Would you like a little gold with your near-term lithium play, ma’am?

Experts

Picture: Getty Images

Experts

‘Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

After a tough 1Q 2023 it seems like the punters are starting to dip their toe in the water again after a flight from risk assets over recent months.

It appears inflation came in much weaker than expected in January 2023, off -0.40% to 6.8% year-on-year (lowest since June 2022) after peaking at 7.40%. This probably contributed to a recovery in base metal prices with copper back in contango and up 5 cents for the week to close at US$4.08/lb despite mixed economic news from China.

January/February residential property starts in China were down 9% and rebar margins for BF-based steel producers around break-even. Figure 1 shows a wide divergence between Chinese construction and crude steel production which appears to remain stubbornly high and no doubt contributing to the prevailing high iron ore prices of US$125.2/tonne.

In February, Chinese net steel exports were also running at an annualised rate of ~66mtpa compared to ~49mtpa in September 2022. Macquarie have upgraded their near-term iron ore prices to US$130/t from US$110/t on rising Chinese demand and an increase in hot metal products and steel production.

The US dollar lost ground with the DYX at 102.57 for a 0.5% loss for the week. US 10-year treasuries closed at 3.46% for an 8 basis point gain. The VIX closed at 18.8 around the median with the DOW having a strong week closing at 33, 261.37 up 2.5% for the week.

Another leading indicator crude oil also had a good week closing up 9% for the week to US$75.57/bbl after the Saudis announced they are shutting down a number of pipelines in northern Iraq.

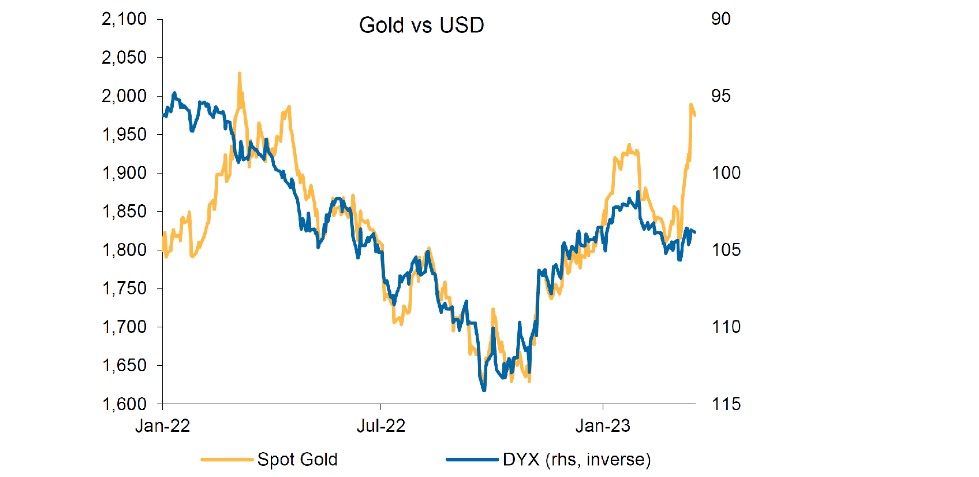

Gold was off US$6 for the week to finish at US$1,971/oz while other precious metals performed well with Palladium up 3.6% to US$1,412/oz and silver US$24.01 up almost 4% for the week. Platinum closed at US$990/oz up US$10 for the week.

It appears the perfect storm for gold is still well and truly alive with many sceptical about the health of a number of European and US banks. Gold has inversely tracked the DYX (figure 2) over the last year or so with Macquarie (Australian Resources, 29 March 2023) believing that gold appears to do better in the early throes of a crises than when real panic ensues.

I think the jury is out on that one given the unprecedent paper print has put global economies in unchartered territory.

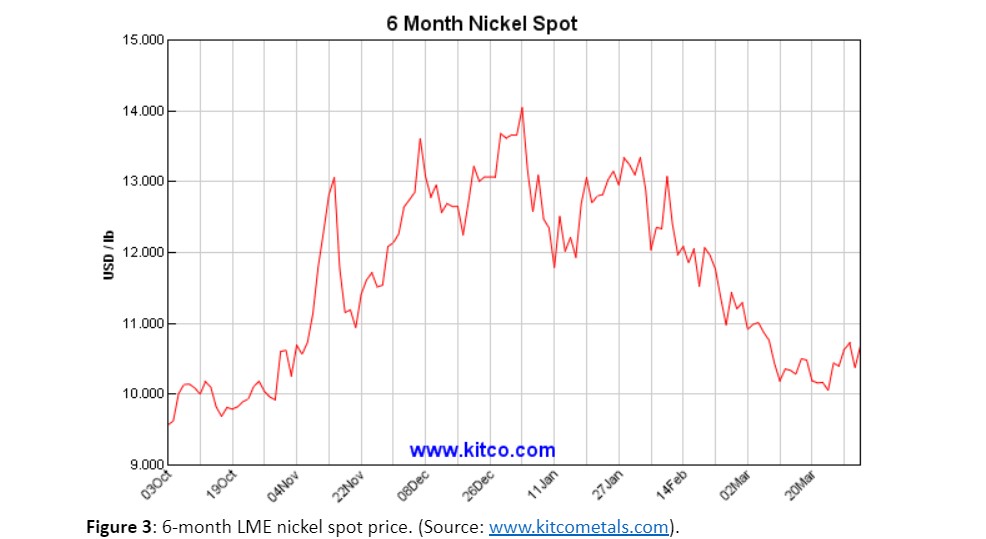

While spot copper prices have increased 2% in CY2023, nickel prices have underperformed and are off 17% in CY2023 to US$22,800/t as new High-Pressure Acid Leach (“HPAL”) projects propel Indonesia into a global force in Nickel and are likely to push the market into oversupply.

Indonesia is currently contributing around 30% of world nickel supply but many analysts are projecting this could double in the next five years. I anticipate nickel prices may well test US$20,000/tonne in the medium term if production ramps up as expected in Indonesia.

In other news the European union passed a law that envisions a total ban on the sale of new diesel and gasoline cars by 2035. The Eu considers the deadline is necessary because the average car’s lifespan is around 15 years. In order to switch to fleets that produces no carbon pollution by 2050, sales of combustion engine cars would have to end by 2035.

The big news last week of course was the $5.5 billion cash bid by for lithium developer Liontown Resources (ASX:LTR) by Albemarle Corp, the world’s largest lithium producer. LTR rocketed by around 70% on the news and closed the week at $2.58/share compared to the bid price of A$2.50/share.

I am thinking after the slump in lithium prices over CY 2023, Albemarle could be thinking the prices might turn around after spodumene concentrate prices have come off from over US$6,000/dmt to around US$4,380/dmt.

Lithium developer Red Dirt Metals (ASX:RDT) (figure 4), chaired by mining engineer David Flanagan, took a step further to production at its 100% owned Mt Ida Project (12.7Mt @ 1.2% Li02) (figure 5) with the lodgement of a direct shipping ore (DSO) Mining Proposal (and Mine Closure plan) with the WA Department of Mines, Industry Regulation and Safety (DMIRS).

We first covered RDT here in December 2022 ahead of its $55 million capital raising at 50 cents per share in January 2023. I did recommend an accumulate rather than buy so hopefully the Stockhead faithful have an average price closer to 40 cents.

Production of lithium concentrates will hopefully come online in late 2023. Drilling is in full swing with five rigs on site upgrading the JORC Resource category as well as targeting extensions along strike and down dip.

While the earnings potential from the pegmatites is significant, pegmatites are interspersed with gold resources (Inferred and Indicated Resources of 318,000 tonnes @ 13.8g/t gold for around 140Koz) that are likely to fall within the open pit. The company hasn’t said much about this opportunity, and I am a little curious as to how this is going to pan out.

The company is confident of commencing production in late 2023 and is hoping to reach final investment decision following the mines department approval of the mine plan (figure 6). The non-binding four-year MoU for off take of up to 45,000tpa of spodumene concentrate signed last year with Vietnamese based VinES Energy Solutions remains in place.

RDT also seems to be having some success at its 100% owned Yinnetharra Lithium Project (figure 5) in the Gascoyne region of WA which covers around 575km2. The company has identified over 50 pegmatites on surface with some impressive recent intercepts including YNRD005 with 55.6m downhole @ 1.12% Li2O.

Three drill rigs are on site with assays from over 50 holes outstanding.

At an enterprise value of just over $100 million and around $50 million in cash I remain optimistic on this spodumene +/- gold play. Given the recent money was set at 50 cents I am thinking 37.5 cents could be an attractive entry price.

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States. The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.