Guy on Rocks: What’ll it be … uranium or gold?

Pic: Via Getty

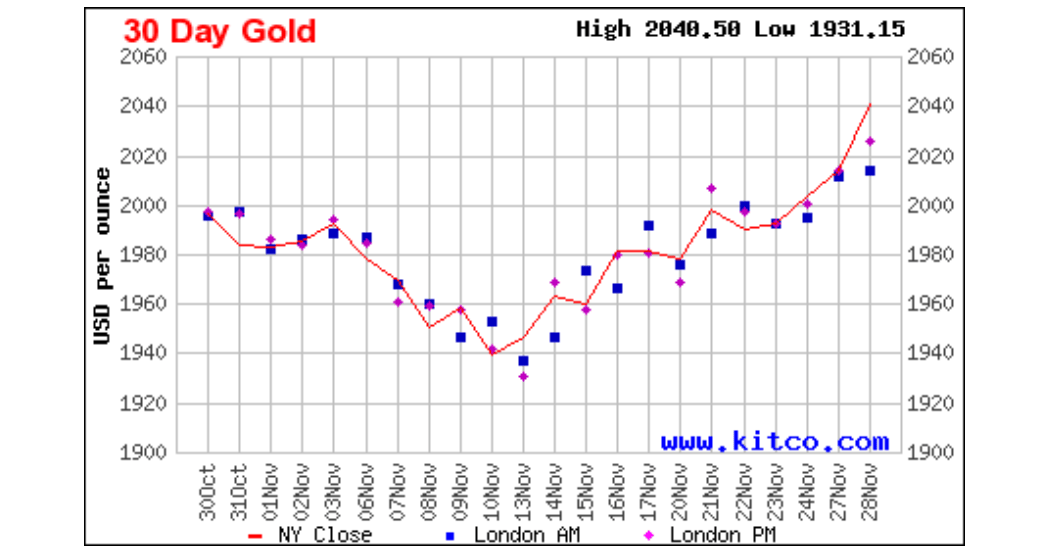

- Gold now approaching 12-month highs at US$2,047/ounce

- Star performer uranium broke though US$80/lb last week for 65% gain over the last 12 months

- Stock of the Week: Gladiator Resources (ASX:GLA)

‘Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Market Ructions: Gold breaks through US$2,000, uranium soars

Gold strengthened last week to finish up US$20 to US$2,002/oz on the back of continuing weakness in the USD which has been declining for the last two weeks.

By Wednesday, gold’s momentum continued and is now approaching 12-month highs at US$2,047/ounce. Securities commodities strategist Daniel Ghali, in a recent interview with Kitco News, noted last week that Chinese traders purchased around 17.5 tonnes of notional gold, extending a period of massive accumulation of gold even as the yuan halts its appreciation.

Ghali also pointed out the lack of Western investment demand, however he believes this will change if the US moves into a recession next year.

The DXY finished down 3% for the week to 103.38, moving lower by Wednesday to 102.56 with volatility levels remaining very low at 12.5, compared to long run median’s around 18.

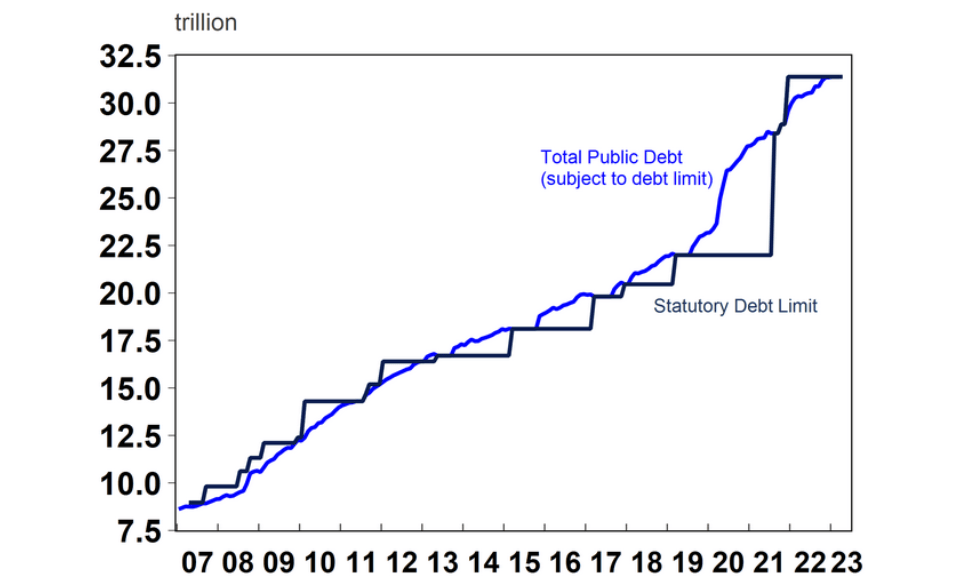

US 10-year Treasuries remained more or less flat at 4.47% before drifting further to 4.29% in early morning trading on Wednesday. Of note is the interest bill for the US Government which now stands at around US$1 trillion.

US Government net interest soared to US$659 billion in fiscal year 2023 (year ending 30 September) up $184 billion (39%), from 2022 and almost double when compared to 2020. US debt now stands at over US$33 trillion on over US$100,000 per capita.

In July of this year, the Congressional Budget Office’s long-term projections suggest interest expenses could reach an eye-watering $1.4 trillion by 2033 and $5.4 trillion by 2053. By comparison, Australia’s debt of around US$900 billion equates to around $33,000 per capita.

Silver followed gold, closing at US$24.32/ounce for a four-month high and platinum and palladium recovered much of their ground from recent sell-offs. Platinum closed US$931/ounce up 4% on the week and palladium closed at US$1,054/ounce, up almost 3% for the week.

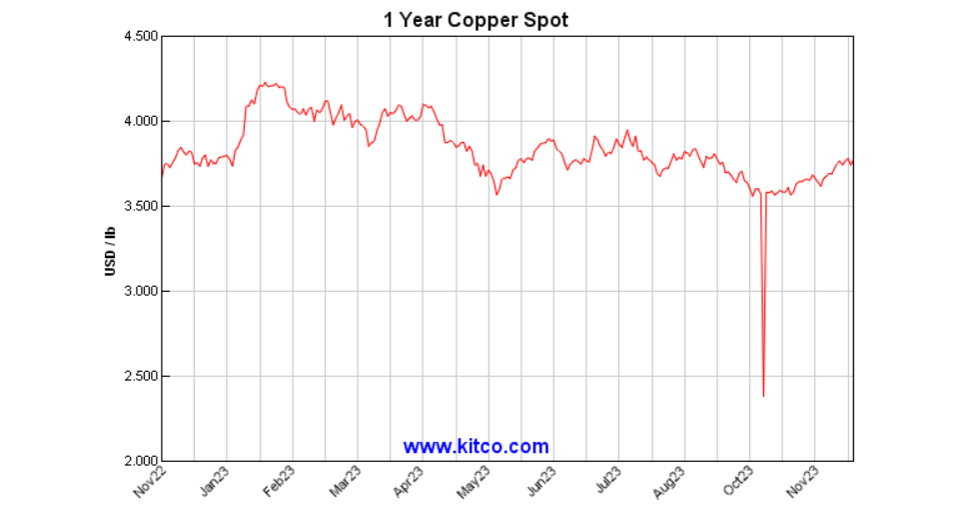

Copper also had a strong move up 8 cents last week in response to the weak USD as well as Chinese stimulus. Copper is trading at US$3.78/lb mid-week and remains in a strong contango.

While various market commentators are projecting a substantial deficit in the next five years or so, ranging from 5-10Mt, Mercenary Geologist (November 24) points out that over the last 15 years or so, copper has remained more or less in balance, varying from +/- 200-300,000 tonnes.

If you believe projected copper usage over the next five years and beyond however, the possibility of a large deficit is certainly real given current levels of copper exploration around the world.

In copper news Chinese miner MMG has agreed to purchase Cuprous Capital, the parent company of the Khoemacau copper mine (Botswana), for around US$1.88 billion. This equates to an enterprise value of around US$1.35/lb per reserves and US$0.13/lb for resources.

Khoemacau has reserves of 31Mt @ 2% copper and 450Mt @ 1.4% copper for 6,444t of contained copper. The mine produces approximately 50ktpa of copper.

No doubt we are going to see more merger and acquisition activity in the copper space given the supply-demand balance.

Ask any metal trader about copper and they will say it is all about Chinese demand. Morgan Stanley (November 23) recently lowered its 2025-2027 real GDP growth forecast (base case) by 40bps to 3.6% p.a., and anticipates growth to depend on China’s economic policies with Morgan Stanley tracking the “5R” policy carefully across:

- Reflating (aggregate demand via monetary/fiscal stimulus),

- Rebalancing (supporting consumption through social welfare and transfers),

- Restructuring (local government and property debt),

- Reforming (SOE productivity and capital allocation) and

- Rekindling (private sector confidence) as key strategies to get out of the debt-deflation loop.

In summary, the Morgan Stanley team consider that one quarter of this 5R strategy has been fulfilled with some improved confidence of further momentum being garnered from recent stimulus signals.

While China’s per capita GDP has doubled over the last 10 years there have been challenges with the 3D or debt, demographics, and deflation. The biggest near-term headache is of course the housing downturn, and associated deleveraging across the sector.

Oil losses were reversed on weak USD and rumours that OPEC is going to meet next week.

West Texas Intermediate finished the week at US$75.2/BBL for a 3% gain. Drilling rigs in the US picked up +4, production remains flat at 13.2MBOPD, inventories are sitting at just under 9MBBLS and imports are up slightly by 200,000 BOPD to 6.5m BBLS.

Despite talk of production cuts, oil continues to remain depressed.

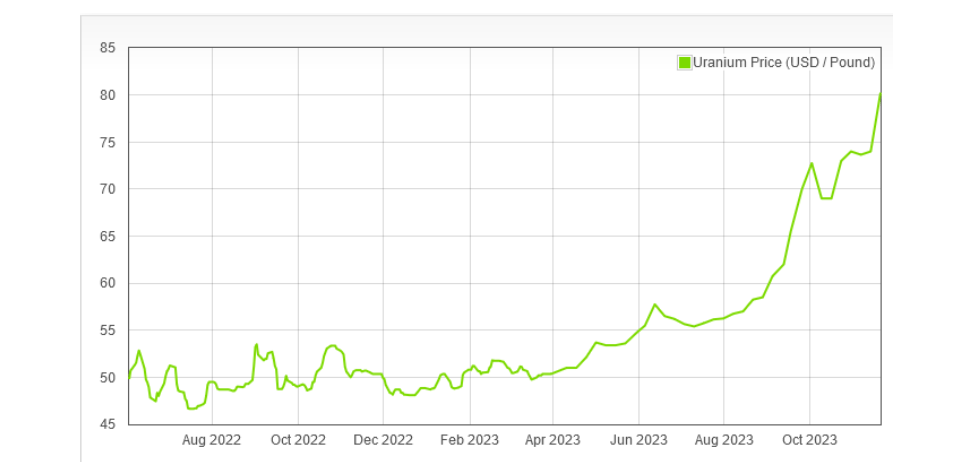

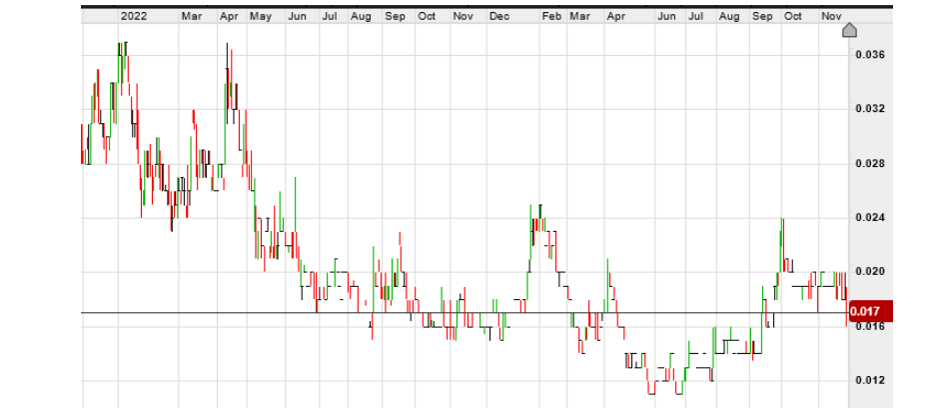

The star performer, uranium (Figure 4), broke though US$80/lb last week for a 6.5% increase or 65% over the last 12 months.

As the risk-on environment rolls out it was somewhat encouraging to see the TSX-V also moving up to 532, up 13 points for the week on slightly better volumes above 20m shares per day, after hitting a pre-pandemic low of 510 a few weeks ago.

A busy week coming up with consumer confidence in US, preliminary Q3 GDP, an OPEC meeting on Thursday, new home and pending home sales, CPE, the Federal Reserves’ preferred gauge of inflation, and manufacturing PMI on Friday.

New Ideas

The RIU Resurgence conference last week featured a few sessions that focussed on Uranium with some of the usual suspects such as Deep Yellow (ASX:DYL), NextGen Energy (ASX:NXG) and Bannerman Resources (ASX:BMN) presenting.

While Australia is holding around one-third of the world’s uranium resources, much of the activity appears to be focussed offshore, particularly in Southern Africa.

One company that wasn’t presenting at the conference was Tanzanian uranium explorer Gladiator Resources (ASX:GLA), which has been consolidating an interesting package of ground, predominantly in southern Tanzania (figure 6).

After a board refresh in the middle of last year, the company is focussing in on its Mkuju Project in southern Tanzania (figure 7).

The Mkuju tenements, previously held by Uranex, Western Metals and Mantra Resources, cover approximately 680km2 (of a total tenement package covering over 1,800km2 in Tanzania) and include some fairly extensive anomalies such as Grand Central, Likuyu South and Likuyu North, situated not far from Uranium One’s 125mlb U3O8 Nyota deposit.

A number of the radiometric anomalies remain untested (figure 7) with next year’s drilling program likely to focus on the Mtonya SWC trend, then expanding to Likuyu North which already has a JORC Resource of 4.6Mlbs U3O8.

Previous drilling at the SWC target back in 2008 also produced encouraging results that will no doubt be followed up in next year’s drill program, including:

- MRSA04: 5m @ 700ppm U3O8 from 7m including 2m@ 1,300ppm

- MRSA06: 7m @ 440ppm U3O8 from surface including 2m@ 675ppm

- MRSA12: 8m @ 1,273ppm U3O8 from surface including 2m@ 3,825ppm

- MRSA07: 5m @ 1,200ppm U3O8 from 2m@ 2,705ppm

- MRSA13: 7m @ 494ppm U3O8 from 3m@ 803ppm

Based on the September Quarterly cash balance of around $500K the company will no doubt be raising money in the short term, but at a market capitalisation of around $10 million and with plenty of targets (many left untested since the Fukushima incident in 2011), this is definitely one to put on the watch list next year.

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States. The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.