Guy on Rocks: Now who’d like a slice of this delicious North American yellowcake?

‘Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Market Ructions: Gold sets new record high (again). Dogs off leash in Middle East. DYX and Copper surge

Gold (figure 1) closed the week at US$2,343/ounce after touching yet another record high of US$2,410.

A trend emerging is a disconnect between the USD as safe haven buying of gold takes over.

I am getting the feeling that we can throw the rule book out the window for the rest of the year as Iran decided to let the dogs out over the weekend.

Silver was also strong finishing the week at US$27.92/ounce for a 2.3% gain.

Platinum had a solid week to close up US$50 to US$975/ounce while palladium closed above US$1,000/ounce for first time in five weeks to finish the week at US$1,032/ounce.

Higher than expected inflation numbers last week saw March CPI rise 0.359% month-on-month with higher medical services and auto insurance contributing to the elevated numbers.

Of note last week was the surge in the USD with the DXY up 165% basis points for the week to close at just over 106.

While there appears almost no chance of a rate cut at the next Fed meeting in a few weeks, it looks like the June meeting according to the CME FedWatch Tool is pricing a rate cut at only 27%.

I think Chris Joye from Coolabah Capital has been calling inflation correctly for the last year or so and he believes we are unlikely to see a rate cut any time soon.

So, I am going for a zero chance of a rate cut in June and close to zero for the rest of the year.

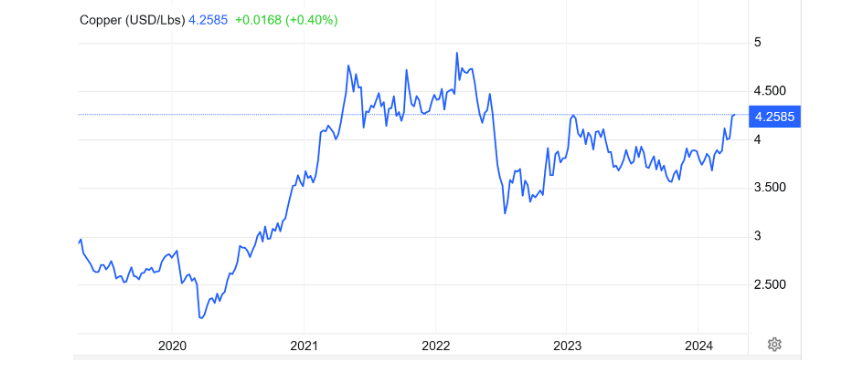

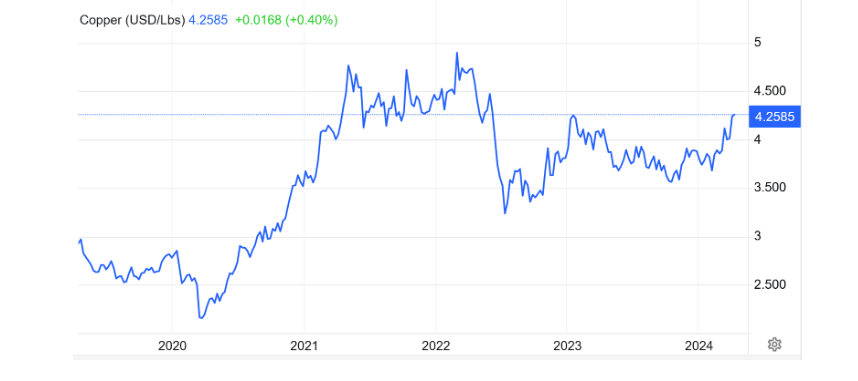

After spending much of 2022 and part of 2023 in backwardation, the tables appear to have turned with copper now in a strong 8 cent contango which according to Morgan Stanley (April 2024), is the widest on record.

Very bullish signs indeed.

In another excellent piece of research, Morgan Stanley (Metal & Rock, April 2024), are calling a “perfect storm” for copper with non-commercial COMEX net positioning pivoting from 35k lots short in mid-February to 20k lots long, representing the highest levels since April 2022.

Supply disruptions (figure 3) and production shortfalls are contributing to what Morgan Stanley believe will be a 700,000 tonnes deficit this year with Ivanhoe’s Q1 production coming in lower than expected on the back of power and heavy rainfall issues in the DRC.

Codelco’s Q1 output was also at its lowest levels since 2019. Looks like the locals are restless again in Peru with protesters blocking the Las Bambas mine (around 300,000 tonnes of copper per annum, accounting for 2% of global copper production) after negotiations again broke down.

Morgan Stanley are calling copper to US$10,500/tonne by 3Q 2024.

I just thought I would blow my trumpet here (there is a first time for everything) and remind the Stockhead faithful of my number one base metal pick this year, American West Metals (ASX:AW1) (figure 4) with exploration getting underway in northern Canada (Nunavut) this week.

The stock has moved from 12 cents hitting cents last week since my last mention in early March. Watch this space.

Oil (figure 5) was volatile last week and traded above US$88 before closing US$86.80/BBL up 10 cents for the week.

Exploration rigs in the US were -3 last week with domestic production flat at 13.1M BOPD.

US oil imports came in at 6.4M BOPD down 200,000 BBLs for the week. Refineries were flat at 15.8M BOPD below long run averages of around 16M BOPD.

Gasoline prices were steady at US$3.63/gallon however West Texas gas is trading at negative values due to the increase oil in the pipeline and is now worth -US$2 MBTU.

That is, producers need to pay the pipeline to take the gas away. It is now cheaper to burn natural gas than coal for energy.

Uranium closed at US$89.50 up 50 cents for the week and appears to be stabilising.

New Ideas: North American Uranium developer

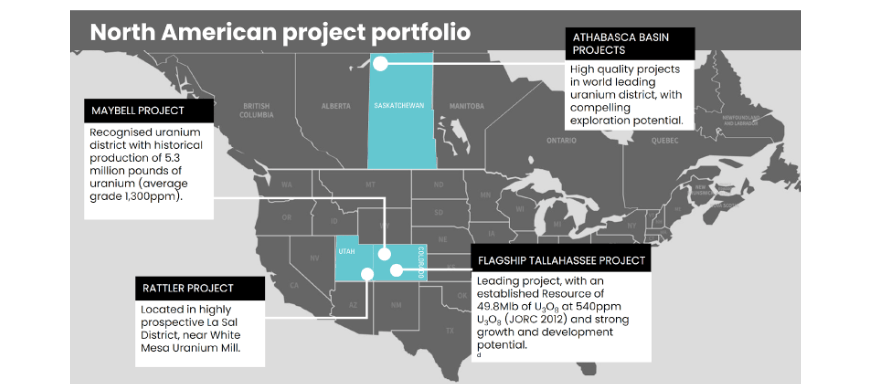

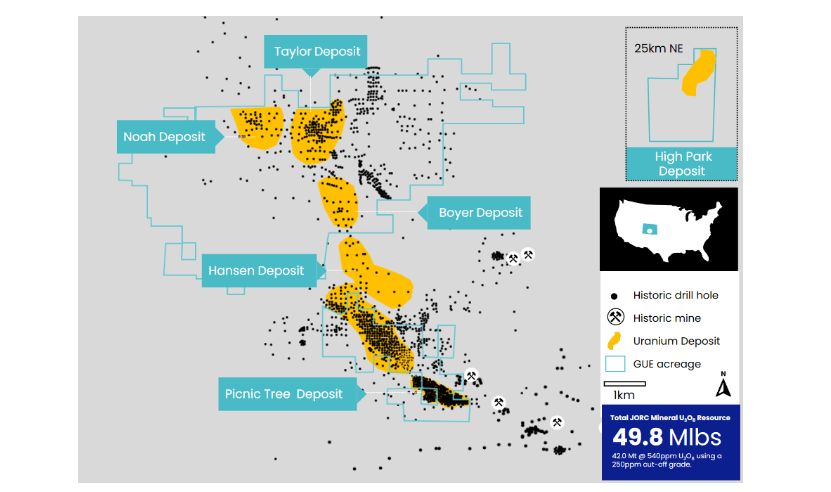

Global Enrichment and Uranium (ASX:GUE; OTCQB:GUELF), headed by metallurgist and capital markets specialist Andrew Ferrier, is one of a handful of listed uranium developers listed on ASX with a portfolio of projects in North America (figure 7).

The Tallahassee Creek Uranium Project in Colorado already hosts a JORC Resource of just under 50Mlbs of U3O8 while the Maybell Uranium Project, also in Colorado, has previously produced 5.3 Mlbs U308.

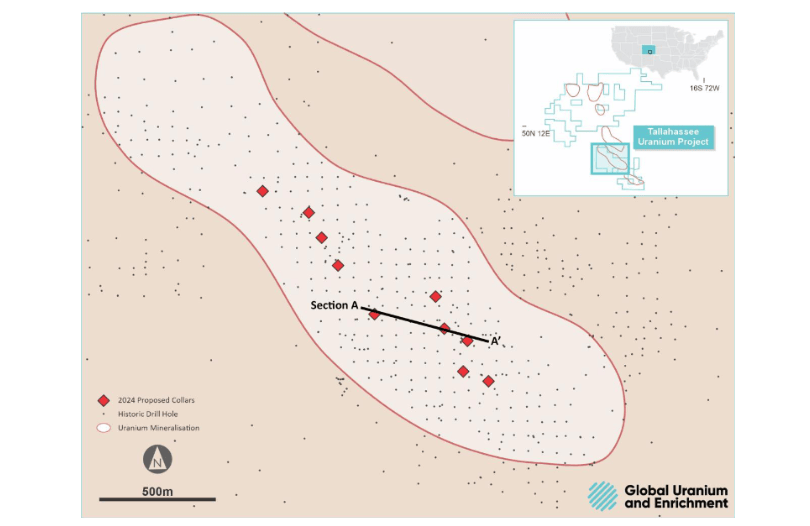

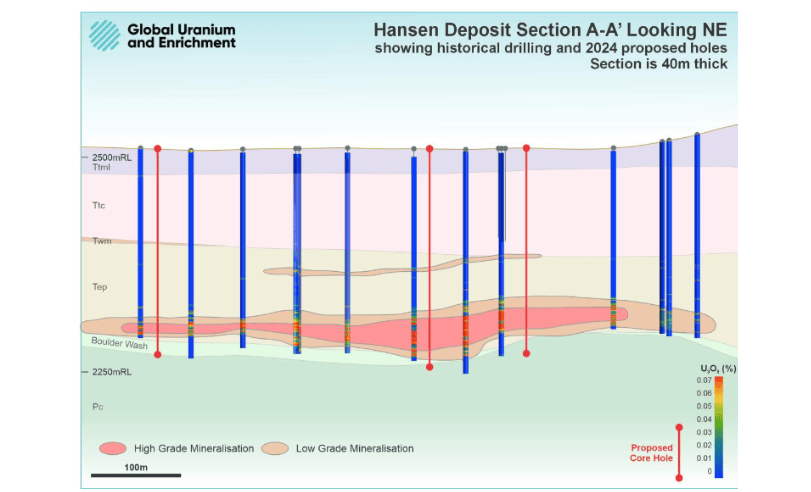

A 10-hole infill diamond drilling program, aimed to gather further metallurgical data, is due to commence in May at the Hansen deposit ahead of a proposed Scoping Study to be commenced in 3Q this year.

Drilling also likely to commence at Maybell in July this year with an exploration target of 3.3 to 5.3Mlbs @ 587 to 1,137ppm U3O8 for a JORC Resource target of 4.3-13.3Mlbs.

The company also has a 20% interest in unlisted Australian based company Ubaryon.

There isn’t a great deal of information available on the technology however it relates to more efficient enrichment processes as well as addressing waste management and material recycling issues.

According to an October ASX release by GUE, Ubaryon is also investigating the technology’s application to isotope separations deployed in nuclear medicine.

I think this is a watching brief pending the outcome of metallurgical testwork to the Tallahassee deposits amenability to either insitu leaching or whether a conventional acid leach is required.

Given the depth of mineralisation, it is highly likely that ISL processes will be required to make the project economics work.

Certainly, looking at other ISL projects such as Peninsula Energy’s (ASX:PEN) Lance Project in Wyoming, the grades are high enough on a first pass review.

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States.

The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.