Guy on Rocks: The case for a uranium double-boom and where the value still lies

Picture: Getty Images

‘Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Market Ructions

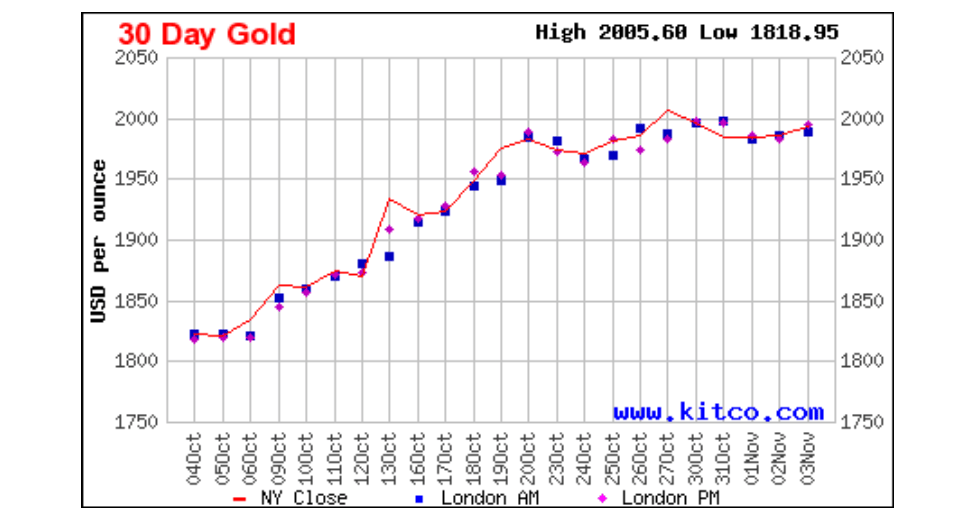

Gold (figure 1) and silver prices both moved higher last Friday, after a soft US economic report that has dampened previous views that the US economy is running too hard.

December gold was up US$14.30 at US$2,008/ounce before pulling back to US$1,992/ounce in late trading. Silver was up $0.244 to US$23.08/ounce on Friday.

October non-farm payrolls in the US came in at an increase of 150,000 compared to market expectations of a 170,000 rise. 297,000 non-farm jobs were added in September.

The US dollar index was softer last week close at 105.07 with 10-year treasury yields dipping following the jobs report to close at 4.57%, down over 30 basis points for the week.

There is no doubt Middle East tensions are keeping gold prices higher, however I suspect that falling bond yields will have a more profound impact.

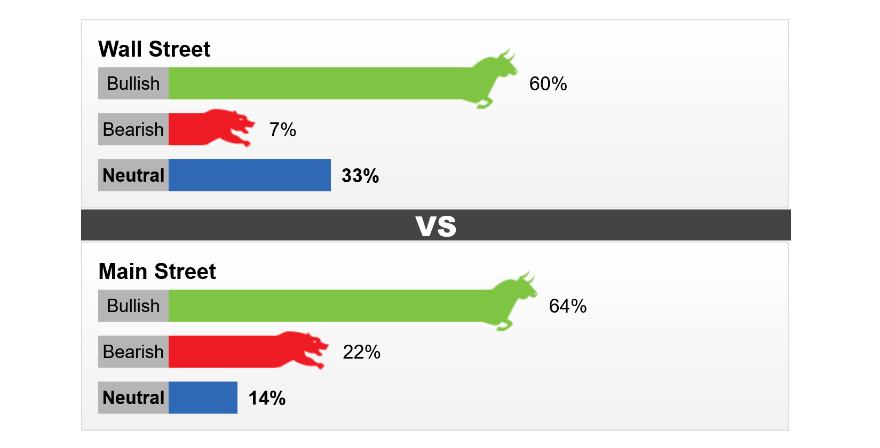

The latest Kitco News Weekly Gold Survey sees retail now evenly split between neutral and bullish.

Forexlive.com’s Alex Button believes that the soft non-farm payrolls report ensures that the Fed’s rate hiking cycle is over, and the fact that gold remains near US$2,000/ounce even as the safe-haven trade wanes is very bullish.

Button commented that we are likely to see more discussion on whether the Fed will cut rate cuts, with the only questions being when, and by how much.

“If you look over the last two weeks, we’ve gone from pricing in 50 basis points in cuts next year to almost 100. We’re at 97 right now,” he said.

The Kitco News Gold Survey (figure 2) saw nine experts, or 60%, expecting higher gold prices this week, with only one analyst, or 7%, predicted a drop in price. The remaining five, or 33%, were neutral on gold for the coming week.

The sentiment from Kitco’s online polls saw 446 retail investors, or 64%, looked for gold to rise next week with 157, or 22%, expecting it would be lower. 98 survey participants (14%) were neutral on near term gold price movements.

In other precious metal news, a number of analysts surveyed last week by Reuters are lowering their price forecasts for platinum and palladium next year on the back of weaker auto production and concerns about a global economic slowdown.

The metals are primarily used in engine exhausts to reduce emissions. Platinum is also used in other industries, jewellery, and for investment.

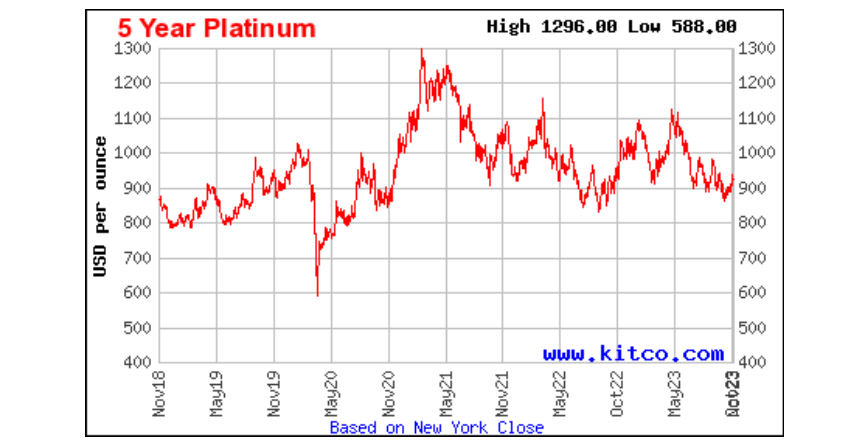

The median forecast from the Reuters survey of 24 analysts and traders were for platinum (figure 3) to average US$1,023/ounce next year, down from US$1,100 returned by a poll three months ago.

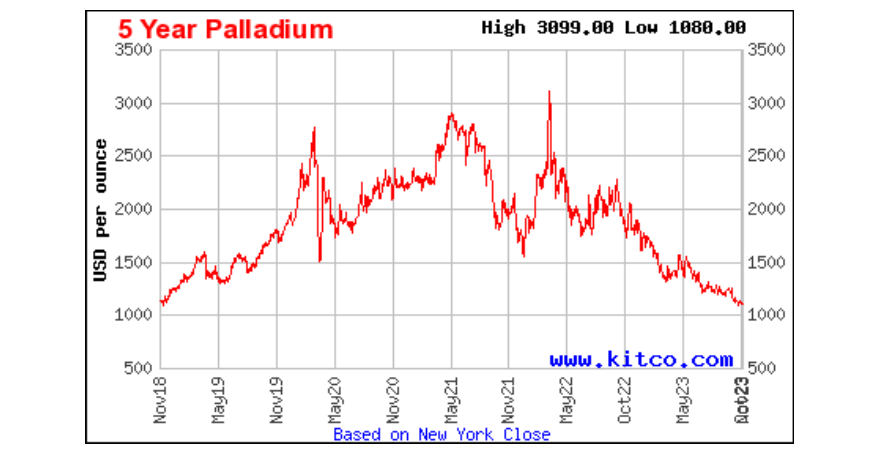

For palladium (figure 4), the poll forecast average prices of US$1,250 an ounce in 2024, down from a forecast of US$1,369 in the previous poll.

Palladium closed down US$5.50 to US$1,128.50/ounce and platinum was up over US$32 to finish the week at US$941/ounce.

Palladium has been the hardest hit this year and is down 38% after it recently touched a five year low of US$1,083/ounce in response to the increasing production of palladium-free electric vehicles and platinum for palladium substitution.

Platinum is down 14% this year after a rally in April-May when power outages and operational challenges in top producer South Africa inflated the risk of limited supply and gold was soaring.

Caroline Bain from Capital Economics commented last week that “Auto production has been softening recently, which has weighed on PGM (platinum group metals) prices and offset the positive impact on prices of falling output in South Africa”.

She sees a modest lift in prices next year as interest rates start to fall globally.

Nymex crude oil prices were firmer on Friday and trading around $83.50 a barrel.

Uranium prices continue to hold up above US$74/lb with the EIA (Energy Information Administration) and ESA (Uratom Supply Agency) recently highlighting the risks around Russian supplies, which has prompted utilities to increase buying and stocking up. The US and EU currently has around 190 reactors operating or around half of the world’s nuclear production capacity.

The US remains heavily reliant on Russian enriched uranium with utilities buying around a third of their requirements from Russia. Rosatom is also supplying 31% of enriched uranium and 21% of converted product to Europe.

There are also noises coming out of the White House that their longer-term objective is to ban the import of enriched uranium products from Russia.

With the US Nuclear Fuel Security Act of 2023 enacted earlier this year as well as National Defense Authorization Act which is authorised to purchase US$3.5bn over 10 years for nuclear fuel security, I can see another uranium boom, not dissimilar to the current lithium boom, just around the corner…

With over 90% of European utilities sourcing uranium from Kazakhstan (27%), Niger (25%), Canada (22%), and Russia (17%) I anticipate there will be a concerted effort to explore and develop uranium mines in stable jurisdictions which leaves Canada, Australia, and Namibia as the preferred destinations.

New Ideas

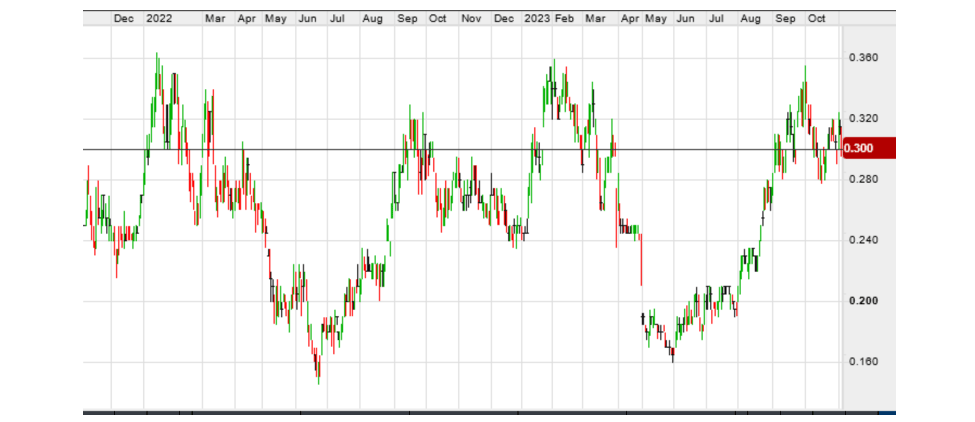

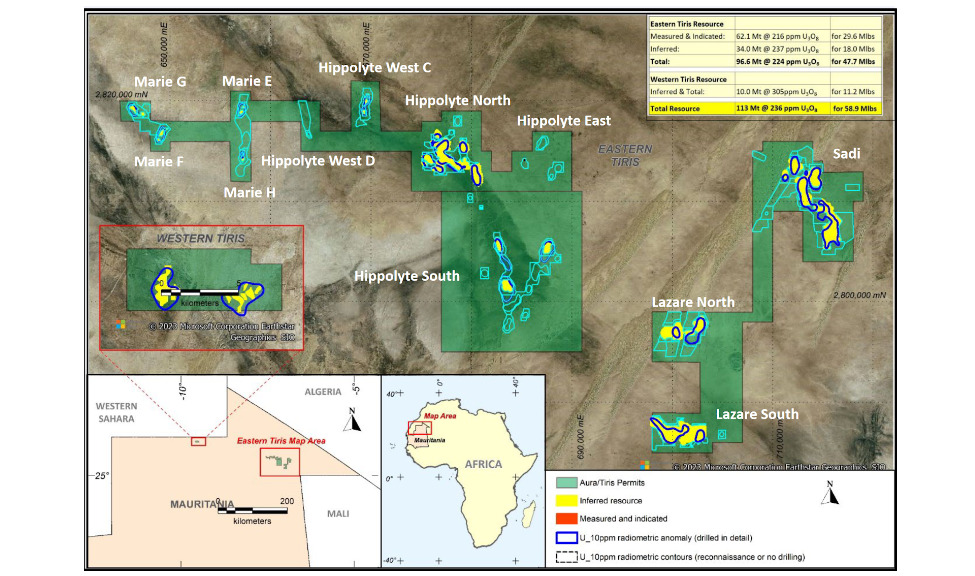

Aura Energy (ASX: AEE) (figure 6) is primarily focussed on its 85% owned Tigris Project situated in northern Mauritania in West Africa (figure 7).

The project, led by mining engineer David Woodall, has total JORC Resources of 59Mt @ 100pm with 30Mt U3O8 @ 100ppm in the measured and indicated category.

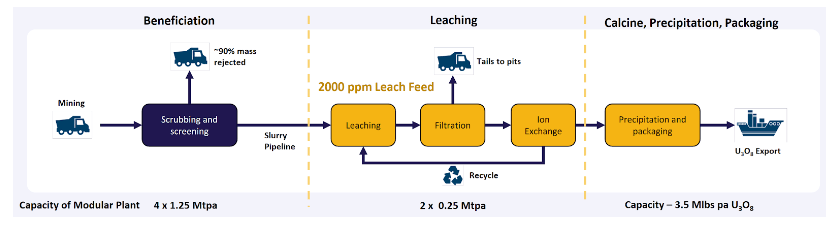

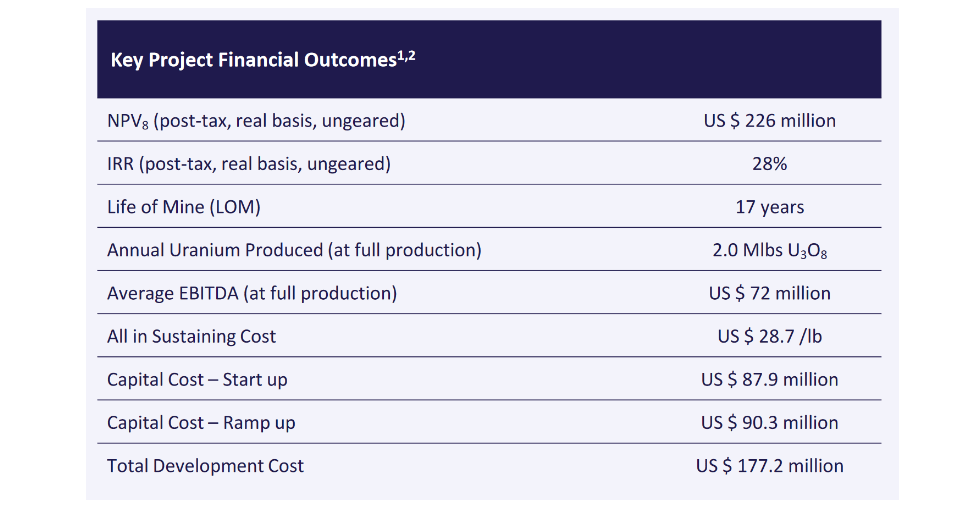

The resource is low grade but more importantly can be beneficiated to around 2,000ppm with the March 2023 Definitive Feasibility Study (“DFS”) contemplating a 2Mtpa operation over a 17-year mine life using a fairly convention beneficiation, leaching, calcine and precipitation flow sheet (figure 8) with the capacity to scale to 3.5Mlb per annum.

The DFS returned a post-tax NPV8 of US$226 million based on a total capital cost of US$177 million (table 3) assuming a US$64 uranium price and all in sustaining costs of around US$29/lb.

AEE represents one of the few opportunities on either TSX-V or ASX to gain exposure to near term production. The company may require further equity as part of the capital costs to start up the project, however at a diluted market capitalisation of around A$220 million the company represents excellent leverage to further uranium price increases.

The caveat here, other than the elevated country risk associated with Mauritania, is of course the 87 million options exercisable at 5.2 cents which fall due in June next year.

One should bear in mind however that medium to longer term offtake agreements are likely to be undertaken at a significant premium to spot prices which gives project valuations plenty of scope to move higher.

Let’s hope the growing unrest in West Africa doesn’t spread to Mauritania and ruin what is shaping up to be an interesting uranium play.

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States. The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Related Topics

Related Stories

SUBSCRIBE

Get the latest breaking news and stocks straight to your inbox.

It's free. Unsubscribe whenever you want.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.