Aussie bank bonds create opportunities to join The IAM 6% Club

Income Asset Management (ASX:IAM) is a fixed income specialist and funds management incubator, which specialises in showing fixed income investors that bonds, cash, debt capital markets, treasury management, and asset management solutions can offer better returns than a boomerang.

The goal of The IAM 6% Club endeavour is to showcase how to achieve a fixed income of 6%, just like it says on the tin.

- Uptake in bonds as investors search for low-risk income opportunities amid market volatility

- Aussie banks offering low-risk Aussie banks offering bonds with 6-7% yield to maturity

- Strong businesses, capitalisation, and investment-grade ratings put banks in favour

Growing inflation, hawkish central banks, slowing economic growth and supply shortages continue to be chorus line for global finance markets in 2022.

Equity markets remain topsy-turvy and while they’ve had a good run in July, pulling back some losses from earlier in the year, it doesn’t take much to spook investors.

Income Asset Management (ASX:IAM) credit strategist Matthew Macreadie said bond investments are becoming an increasingly popular investment as investors search for low-risk income opportunities amid continued economic and market volatility.

“Whether you believe inflation and yields have peaked or not, it’s sensible for investors to have a core fixed income allocation,” he said.

Fixed income valuations

Macreadie said the fast uptake in bonds was due to recent rate rises to combat rising inflation.

Inflation in Australia has reached a level not seen in decades, with new data from the Australian Bureau of Statistics (ABS) showing the consumer price index (CPI) rose by 1.8% in the June quarter, with the annual inflation rate increasing to 6.1%.

It’s the highest inflation rate since 1990 when Bob Hawke was PM and the country entered what then treasurer Paul Keating famously described as “the recession Australia had to have”.

That recession more than 30 years ago followed the stock market crash of 1987, an international recession and rising rates which hit ~17%.

Fast forward to 2022 as concerns of another recession play on investors’ minds Macreadie said bond markets are experiencing a resurgence from broader sell-offs.

“Fixed income valuations are substantially better than they have ever been and you’re getting very decent income yield levels on investment-grade credit,” he said.

Options to join 6% Club

Macreadie said for fixed income investors wanting to join The IAM 6% Club many Aussie investment-grade bonds are offering a 6-7% yield to maturity.

“Over the life of the bond, rates and prices change but the bond delivers the expected return assuming it doesn’t default, which in an investment-grade world is highly unlikely,” he said.

However, he said credit selection will become very important, especially in the high yield credit market.

“The USD high yield credit market, for example, is pricing a default rate of around 4-5% when yields are around 8%, based on the ICE BofA US high yield index,” he said.

“Amidst inflation and recessionary concerns, credit spreads have pushed considerably wider, especially in the subordinated banking space.”

A credit spread is the difference between the quoted rates of return on two different investment products.

The products are usually of different credit qualities but similar maturities. A credit spread is used as an indication of risk premium for one investment over another.

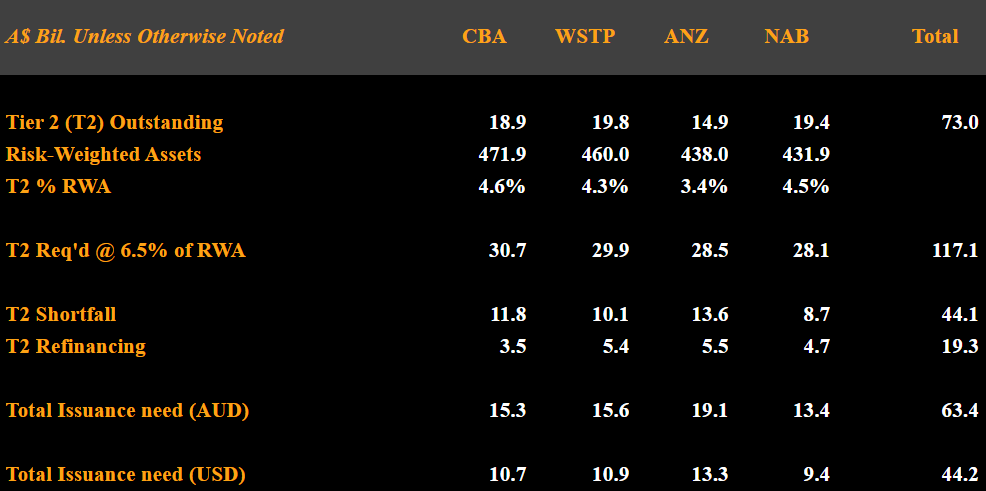

Value in Tier 2 space

In the Australian debt capital structure, Macreadie sees the best value currently in the Tier 2 major bank space.

“Value in the additional Tier 1 space is not as good versus those more senior layers of capital, including Tier 2,” he said.

He said the most recently issued Tier 2 is the National Australia Bank (NAB) subordinated bond with a maturity of 2032. It is callable in 2027, which means can be redeemed before its maturity at the issuer’s discretion.

The floating and/or fixed rate bond comes at 290bps above three-month BBSW/SQ ASW representing what Macreadie describes as “good relative value”.

A couple of more definitions. BBSW stands for ‘bank bill swap’ and it’s the primary short-term rate used in financial markets for pricing and valuation of Australian dollar securities and as a lending reference rate.

“The fixed NAB subordinated bond translates into a yield of 6.3%,” Macreadie said.

“In early June 2022, NAB issued an additional Tier 1 security (NABPI) with a margin of BBSW+3.15%, currently trading a discount margin of 320bps.

“This is callable in 2029 and is at the bottom of the capital structure.”

Macquarie and CBA Tier 2s outperform

Macreadie said fixed rate bonds of the recent Macquarie and Commonwealth Bank of Australia (CBA) subordinated Tier 2s have both outperformed identical floating rate bonds.

“This makes a primary fixed look attractive especially given the current interest rate environment,” he said.

Macreadie said the advantage of fixed rate bonds is that they capture and lock in market expectations even though they have not yet eventuated.

If a bond does as currently priced, then an investor will receive a return in line with the market and if not, then an investor will still get the higher income as the coupon is fixed.

There may also be price appreciation in the bond itself based on the inverse relationships between bond prices and interest rates. When interest rates fall, bond prices rise and bond yields fall.

“We like the Aussie major banks for their strong businesses, capitalisation, and investment-grade ratings down the capital spectrum,” Macreadie said.

“Asset quality will also be helped by low unemployment, careful macroprudential measures, pre-payments of mortgages, and a 40-50% of mortgage stock in fixed rate format.”

This story was developed in collaboration with Income Asset Management, a Stockhead advertiser at the time of publishing.

This story does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.