Stanmore shrugs off hostile takeover bid, just keeping its promise with cash return

Pic: Thana Prasongsin / Moment via Getty Images

The head of cashed-up coal producer Stanmore Coal says his only motivation for giving back more cash to shareholders is to show the company does what it says it’s going to do.

Stanmore revealed on Friday it would pay shareholders 3c per share back in the form of a dividend, which equates to a total return of about $7.6m.

It is also undertaking a buyback of up to 10 per cent or 25.3 million of its shares.

“Our mantra in the business is if you’re going to do something, do it early and we were always going to do a dividend, so we did it early,” managing director Dan Clifford told Stockhead.

“It just happened within a takeover period.

“There will always be timing issues but there is nothing better when talking to your shareholders to match your rhetoric with action and that’s our motivation.”

Stanmore only started paying dividends at the end of the 2018 financial year.

This latest return is already a 50 per cent hike on the full-year dividend it paid in November last year and this is just an interim dividend.

Stanmore is currently being pursued by Indonesian company Golden Investments.

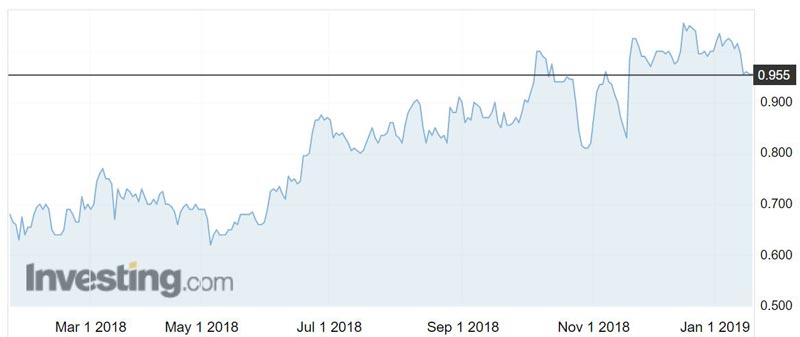

Since Golden Investments’ 95c takeover offer was announced in November, Stanmore’s share price has hit a peak of $1.08, and is currently trading around 95.5c.

Stanmore has urged shareholders to reject the 95c per share offer.

Golden Investments has so far only managed to attain just under 22 per cent.

And Mr Clifford is confident the hostile takeover won’t get off the ground.

“There was a transaction done before this takeover bid was launched of 19.9 per cent, if you look at where [Golden Investments] is now, six weeks into the bid period they’ve picked up 2 per cent, I’m not worried by that,” he said.

“More to the point for us, at 95c the offer really is a distraction on us running our business.”

- Subscribe to our daily newsletter

- Bookmark this link for small cap news

- Join our small cap Facebook group

- Follow us on Facebook or Twitter

Golden Investments’ play for Stanmore has put the junior in the “spotlight”, according to Mr Clifford, and interest in the company has picked up.

“This is the rough and tumble world of the capital markets and we’ve had a spotlight put on us from interest from one company that has elicited, as you can imagine, by default a lot of other interest in the business as well,” he said.

“I think as time unfolds, logically we will remain in one way, shape or form attractive to someone at some point.

“Our view here is whether we’re a target or not doesn’t matter, what we are doing is acting on behalf of all our shareholders and the only way we can act properly in that regard is maximising the outcome for our shareholders at any point in time.”

Stanmore picked up Vale’s closed Isaac Plains mine in Queensland in 2015 for a measly $1.

Last week the company upped its production target for FY19 for the second time to 2.15Mtpa, with costs estimated at $86 a tonne (excluding state royalties).

Coking coal shipped from Australia is fetching more than $US170 a tonne at the moment.

Stanmore said it upped its production guidance because the Isaac Plains mine continues to beat expectations.

The company estimates it will book between $140m and $150m in earnings before interest, taxes, depreciation and amortisation in FY19.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.