Oil giant Saudi Aramco denies making gas-powered move into Bitcoin mining

Saudi Aramco, a multi-billion-dollar company and the biggest producer of oil on the planet, has refuted reports it’s embarking on Bitcoin-mining ventures.

Rumours the oil giant is planning to use its gas by-products to generate electricity for Bitcoin mining began circulating over the weekend, via various media outlets.

The reports possibly arose after comments from Raymond Nasser, Head of Mining Operations at digital asset management firm Wise&Trust, appeared in a TrustNodes article.

Nasser reportedly said: “We are negotiating with Aramco. All black liquid [oil] that comes out of the desert belongs to this company. All the flared gas they’re not using, and that’s public information, I can tell you, it’s enough to ‘power up’ half of the Bitcoin network today from this company alone”.

In a statement on its website, the Saudi oil company debunked the reports: “With reference to recent reports claiming that the company will embark on Bitcoin mining activities, Aramco confirms that these claims are completely false and inaccurate.”

In a tweet today, Nasser has now made it clear that there are “no formal official talks” taking place between Wise&Trust, the Saudi oil barons and other crypto-mining parties.

There are no formal official talks between Arthur Mining/Wise&Trust and Aramco at the moment.

— Raymond Nasser 🇮🇱 (@RayNasser123) August 1, 2021

Not just a lot of hot air?

Despite denying the Wise&Trust connection, Saudi Aramco has, however, shown particular interest in leveraging blockchain technology for improving its operations. According to Cointelegraph reports, the oil company has a history of investing in blockchain-related firms.

Aramco first caught the attention of the cryptoverse when it announced in early 2020 that it had invested US$5 million in the blockchain-based oil-trading company Vakt, which is headquartered in London.

The Saudi company is also linked in a US$6 million deal with Data Gumbo Corp. to develop a commercial blockchain network to improve oil and gas supply-chain efficiency. Data Gumbo is a US technology company based in Houston, Texas – a state with increasing ties to Bitcoin-mining operations.

Bitcoin’s increasing green scene

Converting gas by-products to electricity is a potentially sustainable and profitable way to mine Bitcoin. The major green implication is that it can supposedly contribute to reducing harmful greenhouse emissions such as methane, much of which is flared wastefully into the atmosphere.

Colorado’s Crusoe Energy Systems, for instance, has set up data centres at shale-oil sites across the US, harnessing surplus gas into electricity to mine the no.1 digital asset. The company has backing from large crypto-investment players Winklevoss Capital and Coinbase.

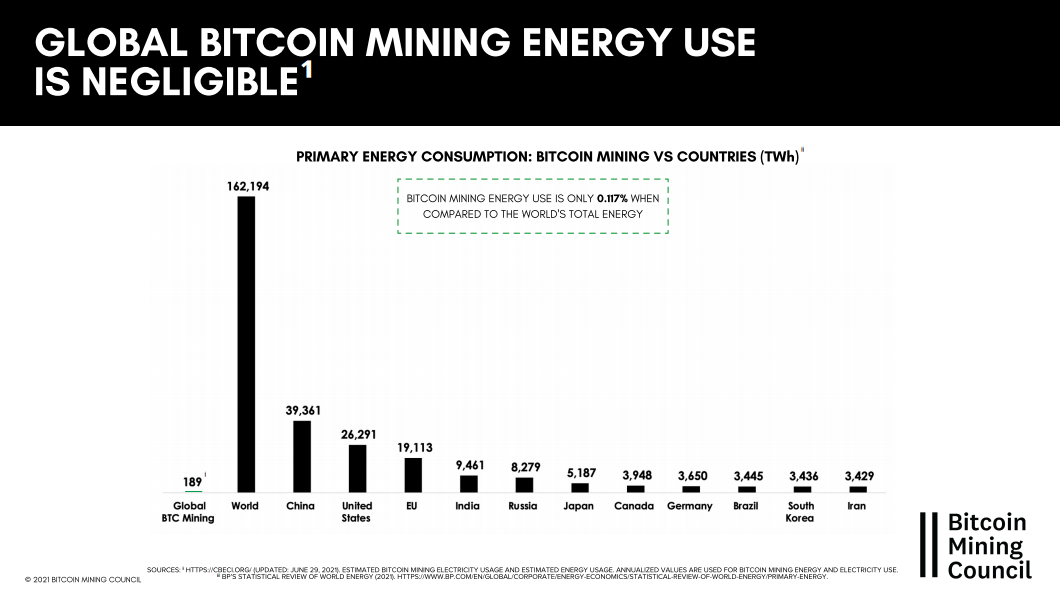

And sustainable Bitcoin mining is taking hold everywhere, if a Bitcoin Mining Council report released on July 1 is to be taken at face value.

“Bitcoin is powered by a higher mix of sustainable energy (56%) than any other industry or major country,” reads a section of the report.

The council, established in May by MicroStrategy’s Michael Saylor, with support from several US crypto mining companies, seeks to “shape the narrative” around Bitcoin – with data such as this:

With the continued exodus of Bitcoin mining operations from China, dispersing into regions including Kazakhstan, Russia and the USA, plus the likes of Michael Saylor and Elon Musk regularly adding to the discourse, the Bitcoin-mining space is worth keeping an eye on.

It’s unsettling that one tweet-happy technology billionaire can have such influence on Bitcoin’s price movements, but it won’t surprise if Musk’s Twitter account reveals some chart-rocking news again before the end of the year.

The Tesla CEO has more than once publicly taken the position that Tesla will resume accepting Bitcoin as a payment option when it’s proven that the asset is more than 50% mined using renewable energy.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.