Resources Top 4: Lithium gun PMT’s board plays musical chairs in Quebec; NGX up on African graphite

Crumbling lithium prices were slowly morphing into an actual elephant in an actual room. (Pic via Getty Images

- Patriot Battery Metals’ Ken Brinsden is finally pulling up stumps… to move to Quebec and head the company from there

- Malawi-focused graphite hunter NGX is doing well today on good news regarding licensing of its flagship graphite project

- CuFe and Castile up on no fresh news

Here are some of the biggest resources winners in early trade, Thursday January 25.

Patriot Battery Metals (ASX:PMT)

Big gun lithium play PMT is up a very healthy 12% at time of writing, which is a more than decent intraday gain for a $428m+ stock.

What’s doin’? An international boardroom shuffle.

Another exciting chapter begins for $PMET: Board and Executive Update, Ken Brinsden to Transition to Quebec Based CEO / President https://t.co/a1XPoIqPu1

— Patriot Battery Metals Inc. (@Patriot_Battery) January 24, 2024

Essentially, PMT’s lithium-industry stalwart and (non-exec) chair Ken Brinsden is moving to where the big action is right now – Quebec, Canada – to head up the company from over there.

Specifically, he’s moving to Montreal, and his position changes from non-executive chair to CEO/president/managing director. The boss. The gaffer. Work as a team and do it my way, etc.

Pierre Boivin, who lives in Quebec, will step into the role of non-executive chair from non-executive director. Current CEO/president, Blair Way, will move into the COO (chief operating officer) role, retaining his executive board position.

Why the changes? The company report this morning notes that the intention is to increase Patriot’s senior leadership presence within Quebec, as the company’s Corvette project enters and moves through the development phase.

Speaking of which, last week, PMT announced that Corvette – the largest lithium drill campaign in Quebec – is now underway.

The 2024 drill campaign at the $420m company’s Corvette property is targeting a minimum of 45,000m over the January to April period – the winter program.

At least 10 drill rigs are lined up for spinning for the four months, which defines it as a large-scale undertaking.

How’s this work in the depths of a finger-freezing, organ-shrivelling Canadian winter? PMT reports the winter access road is fully operable at this stage, reducing the dependency on choppers, so the expectation is the per-metre cost shouldn’t be overly high.

Core assay results remain to be reported for more than 125 drill holes, including ~1.5km of prospective pegmatite trend across the CV5 and CV13 pegmatites.

An updated mineral resource estimate won’t be coming from PMT until later in the year, third quarter.

Situated in the Eeyou Istchee James Bay region of Quebec, PMT’s Corvette Property is Patriot Battery Metals’ flagship project.

Its CV5 Spodumene Pegmatite has an impressive MRE – 109.2 Mt at 1.42% Li2O and 160 ppm Ta2O5 (tantalum pentoxide) inferred.

PMT share price

NGX (ASX:NGX)

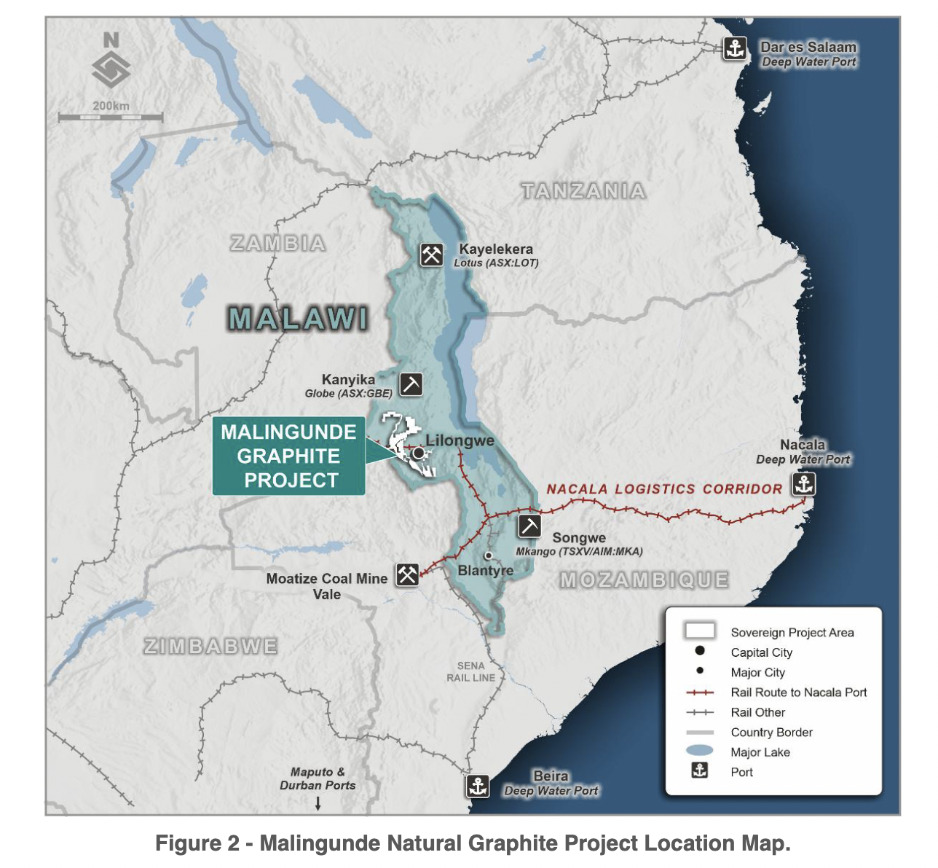

NGX – no, not the Nigerian stock exchange – the African graphite-focused, ASX-listed, $13.6m market capped explorer is making a move today on some good news.

The company has been issued a Retention Licence for the Malingunde project in Malawi, which is a premium quality, low-cost natural flake graphite project.

According to NGX, based on a Pre-Feasibility Study (PFS), Malingunde has exceptional economic and environmental attributes. That PFS was previously completed by Sovereign Metals in 2018 and updated by NGX via prospectus in April 2023.

Why is it considered a “premium” project, then? Partly because it reportedly has a large, weathered saprolite component, which, in contrast to hard-rock deposits can result in lower expected energy inputs for mining and processing, keeping operating costs low and margins favourable.

Malingunde comprises a planned open cut mining and a beneficiation processing plant operation, treating run of mine ore to produce on average 52,000 tonnes per year of graphite concentrate at a purity of 97% TGC.

And it’s set to operate with excellent surrounding infrastructure, with graphite concentrate bagged and trucked to railhead at Kanengo, then bunged onto shipping containers and railed to Nacala port for exporting.

What next?

NGX says it will “immediately proceed to review the PFS to investigate whether the project can be optimised by focusing on supplying graphite concentrates to the feedstock market for lithium-ion battery anodes”.

And:

“In parallel with the ongoing PFS and downstream processing work, NGX will commence a comprehensive program of community and stakeholder engagement, continuing the social and environmental consent process,” said the company.

NGX share price

CuFe (ASX:CUF)

(Up on no news)

This emerging copper and iron ore explorer is up a goodly 33% on not much we’re seeing so far today.

Last time it did this, we guessed it might’ve had something to do with nearology based on the movements of WA1 Resources (ASX:WA1).

Something’s afoot with WA1, with issuance of 4m new shares regarding its big $40m capital raising share placement to advance the West Arunta project (gold, copper, niobium, rare earths – but mainly niobium of late).

WA1 shot through the roof in the final month of 2023 on a major upgrade from Canaccord Genuity, which lifted its price target on the niobium hopeful from $11.50 to $17.50.

All eyes are on the maiden resource for its Luni discovery, which is due around the second quarter of 2024.

WA1’s emergence as one of the ASX’s hottest exploration stocks has also sparked a renewed focus on the wider West Arunta region.

And well, that’s where CuFe comes into play.

Recently, the company noted it had significantly increased its landholding around its West Arunta project in WA – with tenure applications in progress for new ground adjacent and adjoining existing applications.

The area has similarities to the WA1 and Encounter Resources’ (ASX:ENR) projects and discoveries approximately 70km to the south.

And the tenure is adjacent to Lycaon Resources’ (ASX:LYN) Stansmore project, where magnetic trends have been identified that have the potential for REE-carbonatite mineralisation.

Plus, the new ground has not been historically explored for REEs and features magnetic anomalies that extend through this area that could be reflective of prospective carbonatites.

CUF share price

Castile Resources (ASX:CST)

(Up on no news, again)

Coper-gold project developer CST is surging again nothing of note as yet today.

In which, case, time to revert back to this – heritage approval granted to get drills spinning at CST’s lithium, niobium and REE Milgun project, some 150km north-northwest of Meekatharra in the Peak Hill mineral field in WA.

Heritage approval has been received ✔️for on-ground #exploration at #CastileResources' #Lithium, Niobium and REE Milgun Projects.

View the announcement here: https://t.co/kh1IXhdeFm#ASX pic.twitter.com/eomXre9gCD

— Castile Resources (@CastileRes) December 20, 2023

And the other day in this column, (Jan 22) Stockhead‘s Reuben Adams gave us the following:

In 2020, Top 10 Aussie gold producer Westgold Resources (ASX:WGX) spun its Northern Territory gold-base metal assets into Castile, which hit the bourse with a market cap of about $40m.

Gathering dust in the basement of Westgold’s portfolio for several years was Castile’s high-grade – but deep — Rover 1 iron oxide-copper-gold discovery.

According to a recent PFS, Rover 1 could churn out 28,700oz gold, 6,900t copper, 300t cobalt and 75,300t iron per annum for $225m in annual revenues.

The development has solid copper and gold equivalent all in sustaining costs (AISC) of A$7030/t and A$1330/oz, respectively. It would cost A$280m to build.

A BFS – the most advanced of all economic studies – is due sometime this year. Formal discussions with customers and financial institutions for project funding is also underway, with CST boss Mark Hepburn recently travelling to India as part of a trade delegation.

“From the meetings we attended it is obvious that India will require vast amounts of copper to meet their decarbonisation goals,” he said in December.

“Castile’s strategy of producing end-user 99% copper means we can negotiate directly with these large companies, securing maximum value for our product and our shareholders.”

CST share price

At Stockhead we tell it like it is. While CuFe is a Stockhead advertiser at the time of writing, it did not sponsor this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.