‘Peerless’: Danakali is building the best SOP project in the world

Pic: Getty Images

Special Report: Demand for Sulphate of Potash (SOP) is flourishing. In early 2021, Danakali (ASX:DNK)will ‘break ground’ at the remarkable Colluli SOP development.

SOP is a premium grade fertiliser ideal for ‘high value’ food crops.

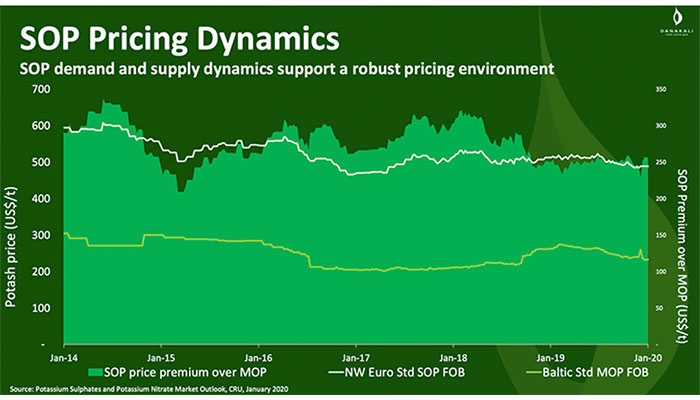

It’s a relatively small market, just ~7 million tonnes a year, but the price has been relatively steady over the past decade compared to other commodities, tracking between $US450 ($688) a tonne and $US600 ($917) a tonne.

By comparison, the more widely used Muriate of Potash (MOP) is a 60 to 70mtpa global market favoured for bulk crops such as wheat, oats and barley.

MOP is cheaper, trading between $US230 a tonne and $US310 a tonne:

SOP is favoured for high value crops because it doesn’t leave a ‘chloride’ taste like MOP.

Many crops are also chloride intolerant, and therefore using SOP is an investment to more production per hectare.

Regardless, the outlook for all fertilisers is extremely positive, says Danakali chief executive Niels Wage.

“We will have 9 billion people globally by 2050 – that’s significant growth in the number of mouths to feed,” he told Stockhead.

“Our analysis shows us there is going to be significant demand growth for SOP – 3 per cent CAGR going forward.

“That’s slightly higher than MOP demand, but in general fertiliser demand is growing. The fundamentals are very solid.”

Colluli: the world’s most attractive SOP development

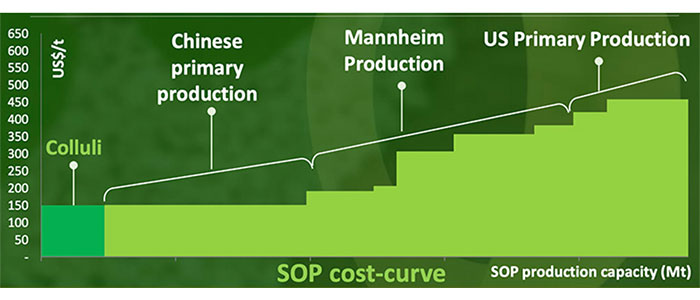

But large, high quality SOP deposits are rare. Around 50 per cent of global supply – about 3.5 million tonnes — is actually created though the expensive ‘Mannheim’ process.

That’s just one of the reasons Danakali’s flagship Colluli SOP development in Eritrea, a 50/50 joint venture with the Eritrean National Mining Corporation (ENAMCO), is in a league of its own.

The scale alone is quite unique, Wage says.

“It’s a big project – 1.1 billion tonnes of ore, which is about 203 million tonnes of product, or about 200 years of production,” he says.

And unlike other potash projects, mining and processing is simple and cheap.

Prior to joining Danakali, Wage was responsible for marketing, sales and supply chain for BHP’s mammoth Jansen MOP Project. That orebody is 1.0km below the surface.

The high grade Colluli orebody starts at just 16m from surface, which means a more cost-effective open cut mining development.

“Colluli can be mined as an open cut pit because it is basically a sea which, 5 million years ago, dried up and form beautiful layers of minerals in solid form,” Wage says.

Unlike other potash developments, the orebody is also geologically ‘simple’ which makes processing faster and cheaper.

“There are very few ‘faults’ in the geology which makes mining the solid salts straight forward,” Wage says.

“We also have a low strip ratio which means that the recovery of the ore from the resource is very high.”

For Danakali, mining and crushing, mixing and drying into a finished SOP product takes only a matter of a couple of weeks.

“Processing is very simple. We will use proven technology – something that we can just take off the shelf,” Wage says.

“Whereas other projects have to go through evaporation ponds, or solution mining – for them, the process is a lot longer and more complex,” Wage says.

Colluli is also very close to existing port infrastructure, providing unrivalled, and relatively cheap, access to global export markets.

All this culminates in a high margin fertiliser project at the very bottom of the global cost curve:

Crucially, Danakali has already secured a 10-year binding offtake with leading global fertiliser company EuroChem for ‘Module 1’ production.

It also has $250m of the required $322m funding in the bag for Module 1 development.

Module 1 development — ~472,000 tonnes a year – is now underway and will provide exceptional returns. Construction is expected to kick off next year.

Low Colluli mine gate costs of $US150/t will result in anticipated average cashflow to Danakali of about $US85m a year over the first 60 years of production.

Module 1 production is scheduled to kick off in 2022, the company says.

After that, Colluli has the flexibility to scale up production via ‘Module 2’ (and so on) to meet growing demand.

Upcoming milestones

Danakali kicked off development earlier this year and remains on track for first production in 2022.

“COVID-19 has had an impact on us, but we were lucky because a lot of the work we are doing is still confirming the FEED study and procuring ‘long lead’ items,” Wage says.

“The big milestone for us is closing the funding gap – we already have $250m committed, we need a small but important balance.

“That’s what we are currently working through.”

SOP is a product that is beginning to get a lot more investor attention, Wage says.

“And given the scalability, low costs, low complexity, and high quality we are one of the best — if not the best — project out there,” he says.

“Our size, at 472,000t, makes Colluli probably one of the biggest developments.

“Our capital intensity is one of the lowest – which is due to the way we can mine and our low-cost processing infrastructure.

“We are close to the target fertiliser markets. From Australia, it is a long way to target markets like Brazil, or north America, Europe. We are very well positioned.

“We got the $200m senior debt facility, we have government approvals. The offtake is there as well.

“And the stage we are at – we have de-risked the project significantly in the last 6-8 months and are now in development.”

This story was developed in collaboration with Danakali, a Stockhead advertiser at the time of publishing.

This story does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.