Musgrave no wallflower with ‘optionality abounds’, Argonaut says

Pic: Tara Moore / Stone / Getty Images

Musgrave Minerals has certainly caught Argonaut’s eye, with the stockbroker swooning over the WA-focused gold explorer’s “enviable position” that allows it to either go it alone or pick up a partner for its high-grade Cue project.

Argonaut analyst Royce Haese believes Musgrave Minerals (ASX:MGV) has hit that “sweet spot” with its high-grade oxide ore, three under-utilised mills within trucking distance and JV partner with deep pockets.

This prompted the broker to initiate coverage on Musgrave with a “speculative buy” and valuation of 38c – a 62% increase over the current share price.

“Optionality abounds for Musgrave Minerals,” Haese said in a recent research report.

“With a resource approaching critical mass for a development decision Musgrave is in an enviable position; go it alone or develop in partnership.

“Either scenario will provide significant upside for shareholders, and there is plenty of search-space for further high-grade ounces.”

Musgrave is well advanced down the path to boosting the Cue project’s resource to over 1 million ounces following continued drilling success that has resulted in numerous high-grade hits.

Most recently, Musgrave discovered new, high-grade gold along the Waratah trend east of one of Australia’s highest-grade undeveloped near-surface deposits, Break of Day. This new trend is interpreted to extend for over 4km.

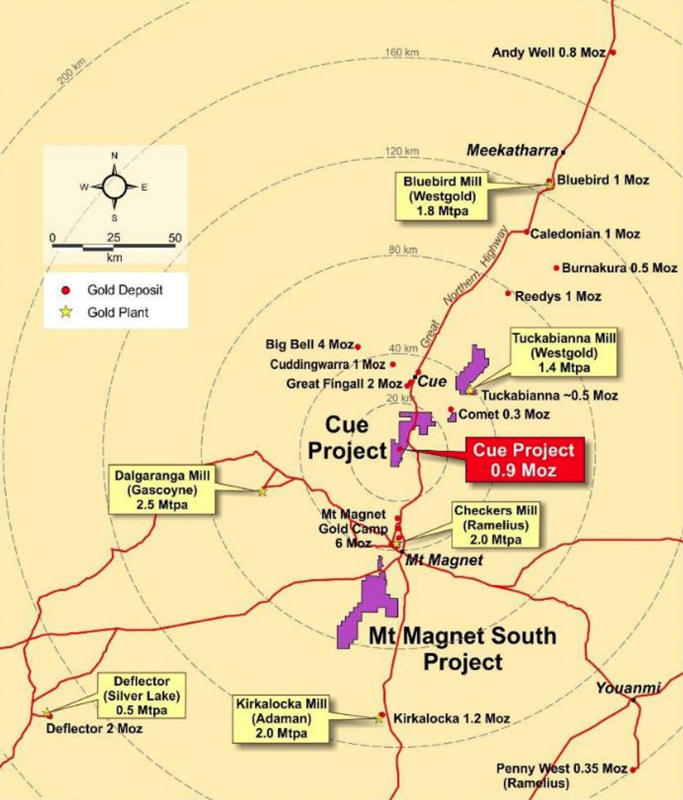

The total resource inventory for Cue right now stands at 12.3Mt at 2.3g/t for 927,000oz of contained gold.

That includes the Break of Day High-Grade Trend, which hosts 982,000oz at 10.4g/t for 327,000oz, and the Moyagee Western Trend containing 9.8Mt at 1.7g/t for 541,000oz.

High-margin, low-cost

Haese noted that these were high-grade lodes essentially to surface, which meant when mined, hits like 14m at 191.1 grams per tonne (g/t) from a depth of just 4m would provide high-margin ounces with limited strip.

“Flashy headline exploration results don’t always flesh out to mineable high-grade projects, poor repeatability/continuity or depth can make follow-up drilling cost prohibitive, the grade of the Cue deposits and proximity to surface puts this project in rare air,” he said.

Meanwhile, Haese views the Lena and Big Sky deposits as near-surface bulk tonnage deposits more akin to the standard WA goldfields pit project, most likely profitable in their own right.

“If MGV plans to run a standalone operation, these higher tonnage projects will provide consistent baseload mill feed,” he said.

“Plus, on prior form, as infill/extensional drilling continues at these prospects there’s every chance further high-grade shoots will be intersected.”

Argonaut’s “back of the envelope” estimates arrived at a $204m valuation for the Cue project, envisaging a 500,000-tonne-per-annum base case, low start-up capex, pit mining/toll treating operation with “plenty of uncaptured upside”.

This assumes trucking of the Cue ore to Gascoyne Resources’ (ASX:GCY) Dalgaranga processing facility, a distance of about 125km by road.

“We’ve selected Dalgaranga as the most likely destination due to it having the largest annual throughput, lowest current head grade, and cheapest operating cost, even when factoring in transport charges,” Haese noted.

Argonaut estimates early works and pre-production capex will amount to about $35m.

Musgrave is currently completing pre-feasibility level studies on a standalone development.

This article was developed in collaboration with Musgrave Minerals, a Stockhead advertiser at the time of publishing.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.