Monsters of Rock: Supply struggles foreshadow a price surge for copper, US fundies Goehring and Rozencwajg say

Looking for copper? Get it wherever you can find it say US experts. Pic: Guido Mieth/DigitalVision

- Why copper prices could surge according to US fundies Goehring and Rozencwajg

- Base metals inventories are down 90% since 2013

- Miners fall ~0.5% in aftermath of Chinese Two Sessions meeting

Copper is one of the hot commodities of the moment, and while an iffy global economic outlook and disappointing Chinese economic growth target have kept prices in check, the long term outlook is bullish.

That is based on expectations of rising green demand for the red metal, expected to lead to major deficits as the needs of modern green technologies outrun supply of the commonly traded red metal.

But even ‘pessimistic’ outlooks for supply growth could be over-optimistic, warn US fund managers Goehring and Rozencwajg, who think the world is walking into a structural deficit of copper bound to propel prices higher.

“In previous letters, we have stressed how metal intensive the coming renewable power investment cycle will be. Last summer, S&P Global’s Commodity Insights paper “The Future of Copper: Will the looming supply gap short-circuit the energy transition?” received significant press attention The study warned of an “unprecedented and untenable” copper shortfall of 10Mt as suppliers grapple with copper demand that will double by 2035. We believe even S&P’s “pessimistic” copper supply outlook is still too optimistic,” they said in a note.

“For years, we have been warning that copper was slipping into a “structural deficit.”

“The S&P study confirms this—including the under-appreciated copper metal intensity of renewable investment.

“Given that inventory of exchange copper adjusted for consumption has now reached the record low levels of 1990 and 2005 and that we are only now seeing the structural gap emerge between copper demand and supply, we believe that the copper market will become the first base metals market to display severe shortage characteristics.”

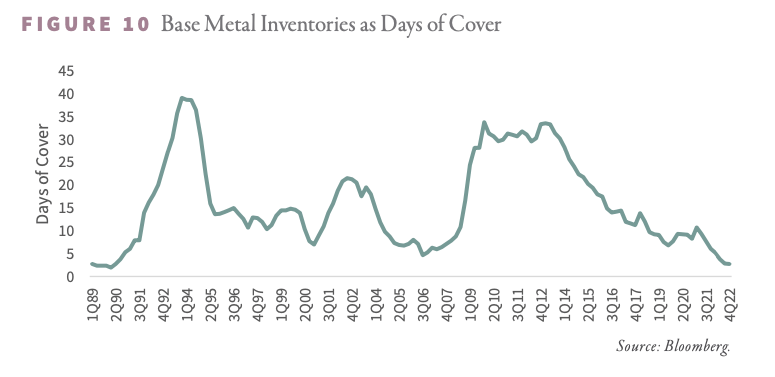

35 year low

At just 2.7 days of consumption, base metal inventories across the London, Comex and Shanghai exchange warehouses were at their lowest levels since 1988 and 1989.

Down 90% from levels in excess of 9Mt in 2013 to under 1Mt today, total metal inventories have slipped to similar levels as the late 1980s before the dissolution of the Soviet Union sent material flooding into the market and almost half the five days of consumption reported in 2005 and 2006 as the Chinese urbanisation boom took off.

Goehring and Rozencwajg noted that as inventories fell below 1Mt to under 5 days of consumption in the mid 2000s copper, nickel, lead and zinc prices surged between 300-400%.

“Today with exchange inventories sitting slightly below 1Mt, these inventories cover only 2.7 days of consumption,” they said.

“In global base metals markets, we are well past the former tightness levels experienced in 2005 and 2006. Given the strength of worldwide demand and supply constraints, we believe it’s only a matter of time before shortages in various metals reach detectable levels, with potentially tremendous resulting upward price pressure. (Emphasis. Ours.)

“Investors over the last year have become convinced the world will become gripped by several global recessions, driven by rising interest rates and continued real estate-related problems in China—both of which will produce noticeable impacts on global base metals demand.

“However, investors are missing the vast new sources of demand now embedded in international base metals demand figures.”

Copper tumbled 0.7% to US$8921/t on Monday after China’s disappointing Two Sessions meeting.

But if Goehring and Rozencwajg are right a price surge could be on the cards at some point in the future. That is heightened by more than two decade long lead times to bring many “economically robust” discoveries into production amid rising and contradictory ESG pressures on both supply and demand, falling head grades and productivity at mega mines like Escondida in Chile and rising nationalism causing civil unrest and sovereign risk at mines in Chile, Peru and Panama.

“Copper demand is now running significantly above copper mine supply, further drawing down exchange inventories. Inventories are now at levels last seen in 2005, just before copper surged nearly three-fold,” they said.

“China is reopening, which will likely result in a surge in copper consumption. The copper market is in a structural deficit, and inventories are dangerously low. We believe copper could see a massive surge in 2023, similar to the period between 2005 and 2006.”

Copper miners share prices today:

Miners fall

It was an expectedly poor day for most of the big miners, with only Fortescue (ASX:FMG) and coal miners up as sentiment faded on China’s bearish congress.

Materials stocks were down a tick over 0.5%, with few commodities standing out. Iron ore miners also weathered more complaints about prices from China’s state planner, which doesn’t think China’s steelmakers should be paying what they’re obviously happy to pay.

There was respite in the futures space though, with Singapore’s 62% Fe contract up 2.09% to US$126.90/t today.

Monstars share prices today:

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.