India’s aggressive stance on pollution puts graphite in the spotlight

In the spotlight Pic: Adam Taylor via Getty Images

India is following China’s lead and has started shutting down polluting operations, which is driving graphite prices higher and seeing investors take another look at emerging producers.

Graphite stocks didn’t enjoy the same love as their battery metal counterparts, lithium and cobalt, during the battery metals run.

But with India now forcing the closure of a plant operated by one of its major manufacturers of synthetic graphite electrodes, coupled with a shortage of coal-based needle coke, propelling the price higher, graphite is suddenly looking attractive to investors.

Graphite India was told to halt operations at its Bangalore plant which, collectively with the two other plants the major operates in India, produces 80,000 tonnes each year.

The company also operates a plant in Germany that produces 18,000 tonnes each year.

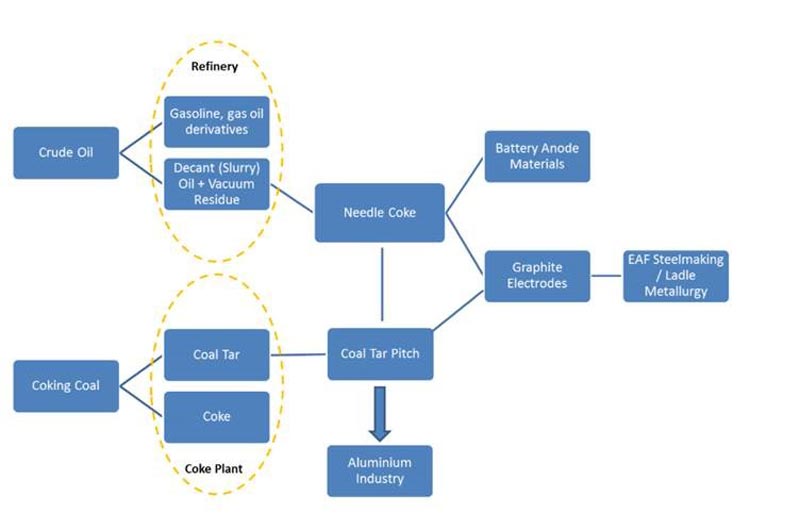

Meanwhile, the production of synthetic graphite is being impacted by an emerging shortage of needle coke thanks to new emissions reductions laws being introduced at the start of next year by the International Maritime Organisation.

Needle coke is mainly used to make graphite electrodes for the steel industry, but it is also used to produce synthetic graphite for use in the anode of a lithium-ion battery.

Natural graphite is also used in anode production.

In fact, you need more graphite in a lithium-ion battery than you do actual lithium.

“While cathode materials such as lithium, cobalt and nickel have received most of the press, graphite is the largest input material by volume into lithium-ion batteries,” Wood Mackenzie research director Gavin Montgomery and research analyst Milan Thakore said recently.

“For example, the Tesla Model S contains up to 85kg of graphite.”

Montgomery and Thakore said that while electric vehicle (EV) sales were still low, they expected the ongoing electrification of transportation to significantly lift demand for synthetic graphite and needle coke in the coming years.

Market forecaster Roskill sees demand for graphite in battery applications growing by 17-23 per cent each year between 2017 and 2027.

The price of graphite has already risen significantly since 2017 and the spread of pollution crackdowns from China to India, and other regions, is expected to see supply tighten even further.

Roskill said despite some downwards readjustment towards the end of 2018, graphite prices remained high.

“Prices for synthetic graphite electrodes increased by more than 800 per cent between January and October 2017 and remain inflated by 2-3 times as of April 2019,” Roskill said.

“Prices for natural flake graphite increased by an average of 45 per cent between September 2017 and February 2018, and still average 15 per cent higher.”

“So far, pollution controls have been focused mainly on the Chinese industry, but Graphite India’s closure suggests that controls in other regions may also have an increasing impact on global supply going forward.”

- Subscribe to our daily newsletter

- Join our small cap Facebook group

- Follow us on Facebook or Twitter

Rising prices incentivise new projects

Higher prices have prompted players outside of China to forge ahead with new flake graphite projects.

Adelaide-based junior Renascor Resources (ASX:RNU) has shored up financial support from a European government agency for its Siviour mine in South Australia.

The company has received in principle support from Atradius, the official Dutch Export Credit Agency, for up to 60 per cent of the estimated $108m capital spend to build its initial graphite production facility.

Renascor says Siviour is Australia’s biggest graphite deposit and one of the largest reported graphite deposits in the world.

Backing from Atradius, which seeks to promote Dutch exports, provides the potential for Renascor to secure favourable debt arrangements.

China also wants more flake graphite, with numbers suggesting the Asian powerhouse imported roughly 60,300 tonnes last year compared to just 5,500 tonnes in 2017 – that’s nearly a 1000 per cent increase in just one year.

Most of the extra graphite came from Africa, according to Roskill.

And that’s because Africa has some pretty large, high quality graphite deposits.

Syrah Resources (ASX:SYR) began production from its Balama project in Mozambique in November 2017.

But the company has faced some hurdles in hitting its production goals, meaning it is not supplying what it expected to the market.

Syrah’s latest figures indicate Q2 will see lower production of 45,000 to 50,000 tonnes, revised down from between 50,000 and 55,000 tonnes previously.

Another 1.1 million tonnes of annual capacity is being developed in Madagascar, Malawi, Mozambique, Namibia and Tanzania.

About 14 of the projects that are closest to starting production are in those countries.

Other ASX small cap players in Africa include Kibaran Resources (ASX:KNL), Triton Minerals (ASX:TON), Walkabout Resources (ASX:WKT), Graphex Mining (ASX:GPX) and Black Rock Mining (ASX:BKT) – all of which have witnessed share price appreciation since the start of the year thanks to the bullish graphite outlook.

Things in Tanzania looking up

The legislative uncertainty that was facing miners in Tanzania looks to be coming to an end, which has also been good for miners in the east African country.

In July 2017, the government introduced amendments to the Tanzanian Mining Act 2010 including potential renegotiation of agreements, a required 16 per cent government ownership of mining projects and the right to acquire up to 50 per cent of mining companies under certain conditions.

Kibaran, which is working to finalise funding so it can start construction of the 60,000-tonne-per-annum Epanko graphite mine in Tanzania, has rallied over 61 per cent since February.

Graphex has climbed 51.5 per cent since January.

The company revealed late last week that the Tanzanian government had confirmed its free carried interest will be set at 16 per cent for all mining licences.

Graphex is advancing its Chilalo project towards production.

“This is an important step forward for Graphex as we seek to obtain the certainty in Tanzania’s legal and regulatory framework required to secure construction financing with Castlelake,” managing director Phil Hoskins said.

Black Rock Mining owns the Mahenge graphite project in Tanzania and is aiming to start construction

The company’s share price has jumped over 143 per cent since January.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.