High Voltage: Battery metal bears are out in force but ‘lithium demand is absolutely there’, says PLS boss

Pic via Getty Images

- Lithium prices continue to slump amid weak Chinese economic scene

- Albemarle quarterly profit comes in lower, while UBS downgrades EV demand outlook

- But wait… PLS boss is still upbeat on lithium demand, and MinRes grabs more of hot stock Wildcat

Our High Voltage column wraps the news driving ASX stocks with exposure to lithium, cobalt, graphite, nickel, rare earths, manganese, magnesium, and vanadium.

So then, what’s the general sentiment right now re the world of critical minerals that service the electric vehicle (EV market)?

It’s complicated, but battery metal bears are definitely out and about, leaving burn-out and donut marks behind as they tear around, flipping the bird from souped-up petrol-guzzlers.

“Spot price” action for lithium is certainly slumping and has been for the best part of a year. There’s no getting around that fact right now. (Or is there? See Joe “Mr Lithium” Lowry’s tweet further below.)

As Fastmarkets reported a couple of days ago, “Chinese lithium carbonate prices are down amid bearish sentiment and thin demand, with hydroxide prices flat”. Meanwhile, East Asian lithium prices are down on weak demand and consumer caution, and European and US lithium prices are also following the Asian downtrend, Fastmarkets continued.

So that’s not great.

2023-11-01#Lithium Carbonate 99.5% Min China Spot

Price: $22,848.23

1 day: $-139.32 (-0.61%) 📉

YTD: -69.00%#Spodumene Concentrate (6%, CIF China)Price: $2,100.00

1 day: $-10 (-0.47%) 📉

YTD: -63.95%Sponsored by @SiennaResources $SIE $SNNAFhttps://t.co/yFr8De2ixo

— Lithium Price Bot (@LithiumPriceBot) November 1, 2023

The weakness in global lithium prices has reportedly erased US$22 billion of market capitalisation at Ganfeng Lithium and Tianqi Lithium, two of China’s biggest lithium producers. “Their latest earnings reports suggest the rout may not be over,” reads an article by the South China Morning Post.

Then the multinational investment banking giant UBS had to come out this week and further rain on proceedings, issuing a research note that downgrades electric vehicle (EV) demand by between 5 per cent and 15 per cent through to 2030.

Basing that forecast on weaker-than-expected EV uptake in Europe and the US, UBS analyst Levi Spry said:

“We have seen these signals for quite some time now with sequentially declining monthly sales, shrinking backlogs and growing discounts.”

Annnd… then there was a Reuters article on the last day of October titled “Lower prices, oversupply to weigh on lithium miners”.

“Albemarle Corp, the world’s largest producer of lithium, is expected to report lower quarterly profit as prices of the silvery-white metal came under pressure due to concerns of falling near-term demand and oversupply,” wrote Reuters, adding:

“Lithium miners have had a tough year as weak electric vehicle (EV) sales growth led to high stockpiles and sent prices of the metal tumbling down.”

Update: the Albemarle quarterly profit has indeed come in lower.

Per Josh’s latest Ground Breakers column:

Albemarle has become the latest integrated international lithium producer to cop a hit — more than halving net cash forecasts for 2023 — as falling lithium chemical prices place the pressure on downstream producers.

The US giant said a mismatch between spodumene pricing and chemical pricing — part of its energy storage division — was partly to blame for a 61.9% year on year fall in adjusted EBITDA from US$1.19 billion to US$453.3m.

Its net income tumbled 66.3% YoY to US$302.5m, despite higher volumes leading to a 10.5% rise in net sales to US$2.31 billion.

That nexus saw adjusted earnings per share drop 63.5% to $2.74 a share, leading US$14.5bn capped Albemarle to a 3.01% fall yesterday.

Read more on that > here.

But… let’s give the bulls some airspace, too

Lithium expert Joe Lowry, who hosts The Global Lithium Podcast, however, reckons elements of that Reuters article were a “complete miss”, and references a more zoomed-out look at the lithium market’s price action:

“Yes, price is down but from the Chinese panic buying driven highs in 2022. Despite the drop, the China carbonate spot price is still >5X the 2020 lows.”

Great example of a complete miss by @Reuters on what is really happening in the #lithium market. Yes, price is down but from the Chinese panic buying driven highs in 2022. Despite the drop, the China carbonate spot price is still >5X the 2020 lows. https://t.co/RIgtVMVZsv

— Joe Lowry (@globallithium) October 30, 2023

And before we look at what’s been turning heads on the ASX in this sector, words from Pilbara Minerals’ (ASX:PLS) CEO Dale Henderson, who was answering questions this week in a recent investor call, pricked up a few ears here and there. (And yes we know, if anyone’s going to be a lithium bull it’s him, but still…)

Henderson alleviated concerns when asked if PLS had trouble selling spodumene on the spot market (just one part of the company’s overall strategy) in the most recent quarter:

“The demand is absolutely there for product,” he said. “It hasn’t been a case of, ‘We can’t move product’, and certainly none of our customers are not wanting product.

“It’s just been more a case of moderating pricing and contending with the question of, ‘What is the right price for the market?’. That’s where the shift has been.”

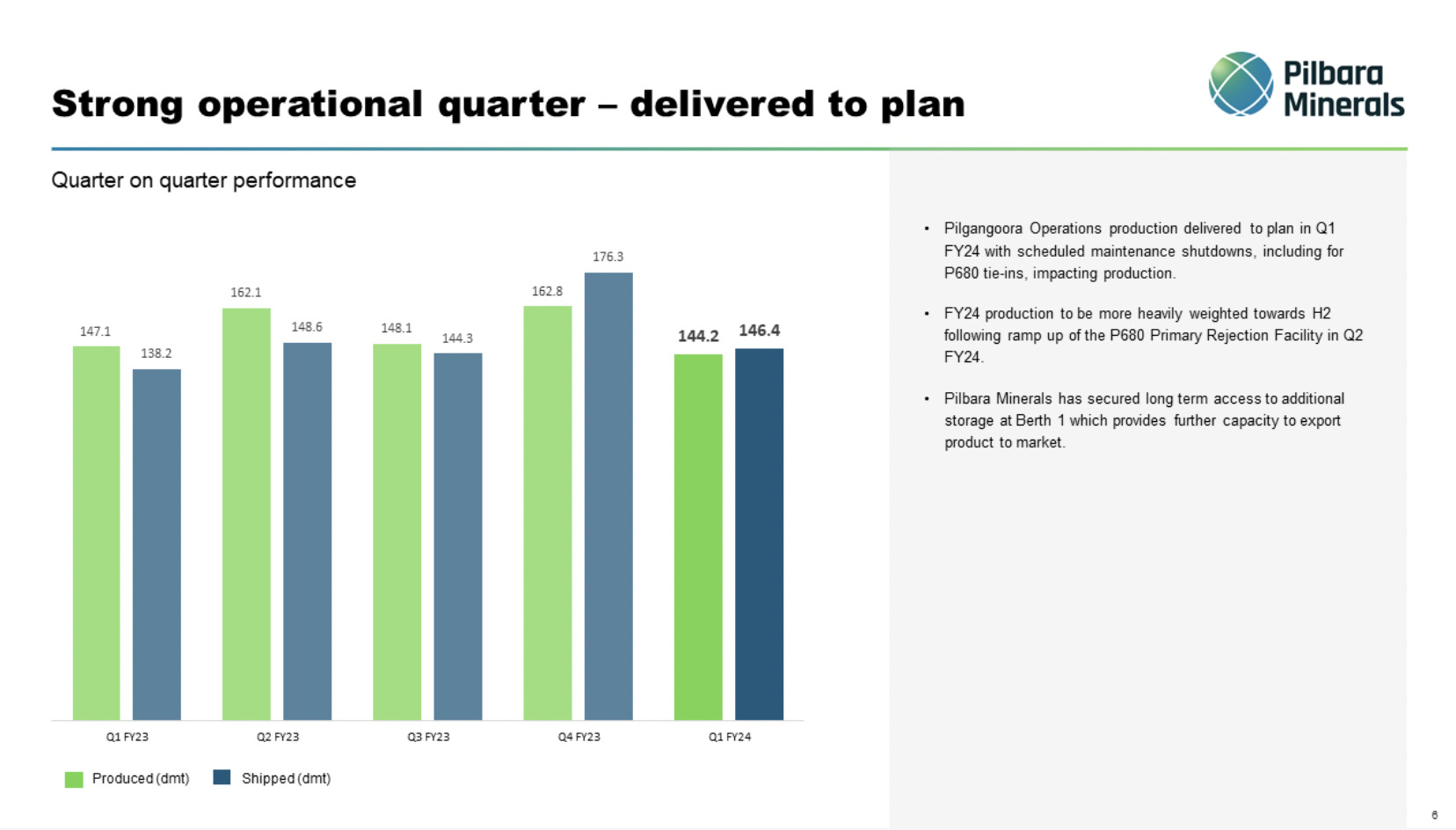

PLS has still been able to deliver a reasonably strong operational quarter again this time around…

… and the Aussie lithium gun maintains a solid cash position, too, with $3 billion. That’s down 9% from the June quarter but the overall trend is still up when you consider the cash balance figure is roughly $1.6 billion higher than this time one year ago.

Oh, another thing. We noticed this neat graphic from Visual Capitalist, too, which suggests that by 2030, the way things are potentially going, demand for lithium will outstrip supply by 46%.

Lithium is one of the world’s most critical natural resources and is central to our push toward sustainable energy ⚡️

Our sponsor @energyx asks: with over 350M EVs expected to be sold globally by 2030, can we meet tomorrow’s lithium demand?

Find out: https://t.co/u6IlifjAyU pic.twitter.com/TyAazAdSve

— Visual Capitalist (@VisualCap) October 27, 2023

After the recent Liontown Albemarle/Rinehart tussle, and after SQM’s major move for Azure Minerals, the ASX lithium M&A scene is still frothy, still front and centre. Mineral Resources has this week come in hot for stonking 2023 Pilbara lithium-hunting success story Wildcat Resources (ASX:WC8) .

So all that ought to tell you something about how highly prized WA’s lithium land is perceived.

The Chris Ellison-led mining giant has confirmed it’s now bought up almost a fifth of WC8, increasing its stake in the company to 19.85%. WC8 is now up about 13% as a result.

Per The Australian:

“Mr Ellison is also speculated to be a shareholder in Azure Minerals under 5 per cent, and some had suspected he may have been looking to amass more shares in the takeover target of which Mrs Rinehart recently raided, with the billionaire gaining about 18 per cent.

“Wildcat’s market value has soared on the back of promising drilling results of its Tabba Tabba lithium project near Port Hedland in Western Australia.”

$MIN I'm a happy Mineral Resources shareholder with Mr Ellison placing blocking stakes in all the key WA lithium assets. Feel for shareholders of $WC8 $GL1 $DLI $ESS as MIN will squash future value growth in their Favour. pic.twitter.com/qJP2Ur4dxu

— Tony (@HookedOnLithium) October 31, 2023

Battery metals form guide

Here’s a snapshot of ASX stocks with exposure to lithium, cobalt, graphite, nickel, rare earths, magnesium, manganese, and vanadium are performing lately>>>

Battery metals stocks missing from our list? Shoot a mail to [email protected] or [email protected]

| Code | Company | Price | % Week | % Month | % Year | % YTD | Market Cap |

|---|---|---|---|---|---|---|---|

| PVW | PVW Res Ltd | 0.057 | -14% | -15% | -56% | -4% | $5,780,072 |

| A8G | Australasian Metals | 0.19 | -3% | -5% | -16% | 0% | $10,424,099 |

| INF | Infinity Lithium | 0.08 | -4% | 0% | -63% | -4% | $38,857,736 |

| LPI | Lithium Pwr Int Ltd | 0.53 | 1% | 47% | -6% | 9% | $330,349,719 |

| PSC | Prospect Res Ltd | 0.089 | -6% | 17% | -6% | -3% | $41,141,092 |

| PAM | Pan Asia Metals | 0.145 | -28% | -28% | -62% | -27% | $23,823,215 |

| CXO | Core Lithium | 0.3475 | -1% | -14% | -75% | -68% | $769,296,796 |

| LOT | Lotus Resources Ltd | 0.265 | 18% | -4% | 15% | 6% | $312,126,110 |

| AGY | Argosy Minerals Ltd | 0.1625 | -14% | -17% | -68% | -41% | $224,705,200 |

| AZS | Azure Minerals | 3.63 | 49% | 34% | 1513% | 341% | $1,555,717,697 |

| NWC | New World Resources | 0.025 | -7% | -17% | -22% | -1% | $58,805,293 |

| QXR | Qx Resources Limited | 0.025 | 14% | 4% | -59% | -2% | $26,537,468 |

| GSR | Greenstone Resources | 0.0075 | -12% | -17% | -71% | -2% | $10,240,623 |

| CAE | Cannindah Resources | 0.08 | -17% | -30% | -59% | -16% | $51,449,116 |

| AZL | Arizona Lithium Ltd | 0.016 | 7% | 7% | -80% | -5% | $51,115,035 |

| HNR | Hannans Ltd | 0.008 | 14% | 14% | -62% | -1% | $19,072,234 |

| COB | Cobalt Blue Ltd | 0.24 | 4% | -6% | -62% | -35% | $86,337,881 |

| ESS | Essential Metals Ltd | 0.5 | 9% | 3% | 9% | 18% | $135,278,382 |

| LPD | Lepidico Ltd | 0.009 | -14% | -10% | -53% | -1% | $68,744,772 |

| MRD | Mount Ridley Mines | 0.002 | 0% | 0% | -60% | 0% | $15,569,766 |

| CZN | Corazon Ltd | 0.015 | -12% | 25% | -12% | -1% | $11,080,762 |

| LKE | Lake Resources | 0.16 | -11% | -11% | -85% | -64% | $227,591,153 |

| DEV | Devex Resources Ltd | 0.275 | -5% | -26% | 2% | -1% | $113,151,334 |

| INR | Ioneer Ltd | 0.155 | -3% | -31% | -72% | -23% | $295,543,685 |

| AVZ | AVZ Minerals Ltd | 0.78 | 0% | 0% | 0% | 0% | $2,752,409,203 |

| MAN | Mandrake Res Ltd | 0.036 | 6% | -10% | 3% | 0% | $20,956,597 |

| RLC | Reedy Lagoon Corp. | 0.005 | 0% | -17% | -57% | 0% | $3,083,418 |

| GBR | Greatbould Resources | 0.062 | -6% | 13% | -30% | -3% | $32,493,551 |

| FRS | Forrestaniaresources | 0.031 | 3% | -31% | -83% | -11% | $3,375,953 |

| STK | Strickland Metals | 0.105 | -5% | 52% | 114% | 7% | $168,120,341 |

| MLX | Metals X Limited | 0.2725 | 5% | -9% | 7% | -11% | $254,034,499 |

| CLA | Celsius Resource Ltd | 0.011 | 0% | 0% | -15% | -1% | $26,952,620 |

| FGR | First Graphene Ltd | 0.077 | -1% | 43% | -33% | -4% | $47,639,682 |

| HXG | Hexagon Energy | 0.009 | 13% | 0% | -33% | -1% | $4,103,327 |

| TLG | Talga Group Ltd | 1.035 | -10% | -13% | -17% | -37% | $366,165,485 |

| MNS | Magnis Energy Tech | 0.062 | -16% | -16% | -83% | -31% | $71,969,889 |

| PLL | Piedmont Lithium Inc | 0.44 | -6% | -29% | -54% | -21% | $161,760,192 |

| EUR | European Lithium Ltd | 0.066 | -4% | -13% | -27% | -1% | $90,625,546 |

| BKT | Black Rock Mining | 0.12 | 0% | 41% | -25% | -2% | $126,169,501 |

| QEM | QEM Limited | 0.2 | 8% | 5% | 0% | 2% | $29,521,384 |

| LYC | Lynas Rare Earths | 7.1 | 4% | 5% | -15% | -75% | $6,583,399,113 |

| ESR | Estrella Res Ltd | 0.006 | -14% | -14% | -43% | -1% | $10,554,431 |

| ARL | Ardea Resources Ltd | 0.52 | 8% | -13% | -41% | -19% | $102,197,505 |

| GLN | Galan Lithium Ltd | 0.63 | -4% | -4% | -59% | -44% | $222,530,036 |

| JRL | Jindalee Resources | 1.28 | -6% | -27% | -46% | -61% | $76,046,287 |

| VUL | Vulcan Energy | 2.15 | -8% | -26% | -72% | -418% | $348,454,073 |

| SBR | Sabre Resources | 0.037 | 12% | 9% | -26% | 0% | $11,950,934 |

| CHN | Chalice Mining Ltd | 1.95 | 6% | -16% | -54% | -435% | $696,244,314 |

| VRC | Volt Resources Ltd | 0.007 | -7% | -7% | -67% | -1% | $27,575,967 |

| NMT | Neometals Ltd | 0.2275 | -16% | -39% | -79% | -57% | $118,961,206 |

| AXN | Alliance Nickel Ltd | 0.062 | 5% | -6% | -22% | -3% | $43,550,377 |

| PNN | Power Minerals Ltd | 0.27 | 13% | 8% | -44% | -26% | $20,726,206 |

| IGO | IGO Limited | 9.295 | -14% | -27% | -39% | -417% | $7,201,616,902 |

| GED | Golden Deeps | 0.051 | -2% | -9% | -54% | -4% | $5,891,640 |

| ADV | Ardiden Ltd | 0.0055 | 38% | 0% | -27% | 0% | $13,441,677 |

| SRI | Sipa Resources Ltd | 0.021 | -5% | 5% | -59% | -1% | $4,791,321 |

| NTU | Northern Min Ltd | 0.0305 | 5% | 5% | -27% | -1% | $189,151,336 |

| AXE | Archer Materials | 0.42 | 4% | -12% | -40% | -20% | $112,132,686 |

| PGM | Platina Resources | 0.027 | 17% | 0% | 42% | 1% | $17,449,049 |

| AAJ | Aruma Resources Ltd | 0.034 | 3% | -6% | -51% | -2% | $6,694,311 |

| IXR | Ionic Rare Earths | 0.021 | -5% | -9% | -52% | -1% | $83,078,203 |

| NIC | Nickel Industries | 0.78 | 2% | 4% | 7% | -19% | $3,192,928,361 |

| EVG | Evion Group NL | 0.04 | 0% | 11% | -59% | -3% | $13,838,367 |

| CWX | Carawine Resources | 0.118176 | 9% | -20% | 40% | 2% | $23,259,101 |

| PLS | Pilbara Min Ltd | 3.62 | -4% | -16% | -29% | -13% | $11,044,727,962 |

| HAS | Hastings Tech Met | 0.795 | 16% | 10% | -78% | -273% | $102,846,488 |

| BUX | Buxton Resources Ltd | 0.195 | -7% | -5% | 95% | 8% | $35,112,106 |

| ARR | American Rare Earths | 0.13 | 4% | -13% | -32% | -6% | $58,035,029 |

| SGQ | St George Min Ltd | 0.045 | 13% | 13% | -37% | -2% | $38,095,874 |

| TKL | Traka Resources | 0.005 | 0% | 0% | -17% | 0% | $4,376,646 |

| PAN | Panoramic Resources | 0.033 | -11% | -11% | -77% | -14% | $103,937,992 |

| PRL | Province Resources | 0.041 | 0% | 0% | -49% | -2% | $48,441,219 |

| IPT | Impact Minerals | 0.0095 | -5% | -21% | 36% | 0% | $27,214,687 |

| LIT | Lithium Australia | 0.031 | 2% | -9% | -34% | -1% | $39,110,134 |

| AKE | Allkem Limited | 9.15 | -10% | -22% | -37% | -209% | $6,099,125,135 |

| ARN | Aldoro Resources | 0.088 | 0% | -2% | -71% | -7% | $12,116,137 |

| JRV | Jervois Global Ltd | 0.03 | -6% | -14% | -94% | -24% | $83,778,141 |

| SYR | Syrah Resources | 0.6775 | -4% | 33% | -72% | -138% | $449,471,990 |

| FBM | Future Battery | 0.091 | -3% | -21% | 65% | 4% | $45,891,539 |

| ADD | Adavale Resource Ltd | 0.008 | -11% | -33% | -73% | -1% | $5,842,954 |

| LTR | Liontown Resources | 1.565 | -12% | -47% | -17% | 25% | $3,872,103,716 |

| CTM | Centaurus Metals Ltd | 0.455 | -7% | -33% | -52% | -67% | $231,670,699 |

| VML | Vital Metals Limited | 0.01 | 0% | 0% | -69% | -1% | $53,061,498 |

| BSX | Blackstone Ltd | 0.1 | -9% | -20% | -38% | -4% | $49,737,335 |

| POS | Poseidon Nick Ltd | 0.016 | 7% | -16% | -64% | -2% | $59,330,842 |

| CHR | Charger Metals | 0.23 | 28% | 84% | -49% | -22% | $10,870,014 |

| AVL | Aust Vanadium Ltd | 0.0245 | -6% | -16% | -23% | 0% | $129,183,776 |

| AUZ | Australian Mines Ltd | 0.012 | -14% | -8% | -81% | -4% | $9,355,904 |

| TMT | Technology Metals | 0.22 | -8% | -21% | -37% | -13% | $58,485,776 |

| RXL | Rox Resources | 0.24 | 9% | 2% | 20% | 7% | $88,207,855 |

| RNU | Renascor Res Ltd | 0.1525 | 5% | 22% | -29% | -6% | $368,214,087 |

| GL1 | Globallith | 1.185 | -4% | -14% | -51% | -66% | $309,326,457 |

| ASN | Anson Resources Ltd | 0.1775 | 11% | 27% | -43% | -1% | $212,146,963 |

| SYA | Sayona Mining Ltd | 0.07 | -15% | -25% | -70% | -12% | $771,997,201 |

| EGR | Ecograf Limited | 0.195 | 26% | 77% | -43% | -3% | $104,096,132 |

| ATM | Aneka Tambang | 1.185 | 0% | 0% | 19% | 29% | $1,544,824 |

| TVN | Tivan Limited | 0.072 | 4% | -10% | -11% | 0% | $113,096,071 |

| ALY | Alchemy Resource Ltd | 0.011 | 0% | -4% | -67% | -1% | $11,780,763 |

| GAL | Galileo Mining Ltd | 0.325 | 2% | 10% | -72% | -56% | $62,251,852 |

| BHP | BHP Group Limited | 45.24 | 4% | 2% | 21% | -39% | $225,558,920,522 |

| LEL | Lithenergy | 0.705 | 22% | 18% | -36% | -7% | $73,137,100 |

| MMC | Mitremining | 0.225 | 7% | -17% | 25% | -6% | $10,203,773 |

| RMX | Red Mount Min Ltd | 0.004 | 0% | 14% | -20% | 0% | $10,694,304 |

| GW1 | Greenwing Resources | 0.13 | 13% | -4% | -61% | -15% | $24,395,207 |

| AQD | Ausquest Limited | 0.012 | -8% | -8% | -25% | -1% | $9,901,791 |

| LML | Lincoln Minerals | 0.0075 | -6% | 25% | 9% | 0% | $11,365,694 |

| 1MC | Morella Corporation | 0.005 | 0% | -17% | -75% | -1% | $30,693,279 |

| REE | Rarex Limited | 0.03 | 0% | -9% | -44% | -2% | $20,501,597 |

| MRC | Mineral Commodities | 0.032 | -11% | 8% | -52% | -3% | $22,818,046 |

| PUR | Pursuit Minerals | 0.0105 | 17% | 17% | -5% | -1% | $32,383,686 |

| QPM | Queensland Pacific | 0.057 | -5% | -17% | -65% | -5% | $114,712,661 |

| EMH | European Metals Hldg | 0.625 | -8% | -10% | -20% | -2% | $78,137,011 |

| BMM | Balkanminingandmin | 0.13 | 4% | -35% | -55% | -20% | $8,944,933 |

| PEK | Peak Rare Earths Ltd | 0.385 | 0% | 3% | -10% | -7% | $108,503,001 |

| LEG | Legend Mining | 0.023 | 10% | -4% | -32% | -2% | $63,898,498 |

| MOH | Moho Resources | 0.006 | -14% | -33% | -74% | -2% | $2,040,267 |

| AML | Aeon Metals Ltd. | 0.011 | -15% | -27% | -58% | -2% | $13,156,807 |

| G88 | Golden Mile Res Ltd | 0.02 | 5% | -33% | -17% | 0% | $5,929,011 |

| WKT | Walkabout Resources | 0.12 | -8% | 4% | -31% | -2% | $80,010,606 |

| TON | Triton Min Ltd | 0.029 | 12% | 32% | 32% | -1% | $40,595,246 |

| AR3 | Austrare | 0.195 | 3% | -11% | -40% | -21% | $28,520,703 |

| ARU | Arafura Rare Earths | 0.1975 | -10% | -24% | -33% | -27% | $390,972,468 |

| MIN | Mineral Resources. | 58.55 | 2% | -13% | -20% | -1865% | $11,273,968,081 |

| VMC | Venus Metals Cor Ltd | 0.105 | 5% | -16% | 20% | 3% | $19,921,512 |

| S2R | S2 Resources | 0.18 | -12% | 0% | 33% | 1% | $79,967,847 |

| CNJ | Conico Ltd | 0.005 | 0% | -17% | -62% | 0% | $7,850,475 |

| VR8 | Vanadium Resources | 0.046 | 5% | -18% | -29% | -1% | $24,756,104 |

| PVT | Pivotal Metals Ltd | 0.02 | 0% | 5% | -56% | -2% | $10,409,497 |

| BOA | Boadicea Resources | 0.039 | 3% | -3% | -61% | -6% | $4,800,522 |

| IPX | Iperionx Limited | 1.395 | 12% | -7% | 96% | 71% | $243,398,716 |

| SLZ | Sultan Resources Ltd | 0.017 | -11% | -19% | -82% | -7% | $2,519,231 |

| NKL | Nickelxltd | 0.059 | 9% | 4% | -62% | -2% | $5,181,095 |

| NVA | Nova Minerals Ltd | 0.25 | -6% | 2% | -64% | -43% | $54,831,390 |

| MLS | Metals Australia | 0.037 | 3% | 9% | -5% | -1% | $23,089,339 |

| MQR | Marquee Resource Ltd | 0.026 | 0% | -10% | -57% | -1% | $10,334,610 |

| MRR | Minrex Resources Ltd | 0.014 | -13% | 0% | -66% | -2% | $15,188,145 |

| EVR | Ev Resources Ltd | 0.011 | -15% | -15% | -50% | 0% | $10,392,578 |

| EFE | Eastern Resources | 0.007 | 0% | -30% | -79% | -2% | $9,935,572 |

| CNB | Carnaby Resource Ltd | 0.615 | -25% | -30% | -30% | -32% | $103,407,424 |

| BNR | Bulletin Res Ltd | 0.175 | 67% | 122% | 35% | 8% | $46,974,576 |

| AX8 | Accelerate Resources | 0.04 | 18% | 60% | 33% | 2% | $17,242,081 |

| AM7 | Arcadia Minerals | 0.085 | -6% | -19% | -70% | -12% | $9,269,259 |

| AS2 | Askarimetalslimited | 0.1475 | -18% | -20% | -66% | -29% | $12,288,034 |

| BYH | Bryah Resources Ltd | 0.013 | -7% | -13% | -40% | -1% | $4,661,869 |

| DTM | Dart Mining NL | 0.02 | 7% | -3% | -70% | -3% | $3,683,066 |

| EMS | Eastern Metals | 0.032 | 3% | -3% | -72% | -4% | $2,637,640 |

| FG1 | Flynngold | 0.068 | 5% | 13% | -32% | -3% | $8,046,573 |

| GSM | Golden State Mining | 0.019 | -14% | -47% | -47% | -2% | $3,439,589 |

| IMI | Infinitymining | 0.11 | -8% | 0% | -51% | -17% | $9,343,166 |

| LRV | Larvottoresources | 0.16 | 60% | 28% | -3% | 0% | $10,760,756 |

| LSR | Lodestar Minerals | 0.005 | 0% | -17% | 0% | 0% | $10,116,987 |

| RAG | Ragnar Metals Ltd | 0.021 | -9% | -9% | 16% | 1% | $10,427,581 |

| CTN | Catalina Resources | 0.004 | 0% | 0% | -43% | -1% | $4,953,948 |

| TMB | Tambourahmetals | 0.165 | 27% | -18% | 18% | 6% | $9,538,141 |

| TEM | Tempest Minerals | 0.0075 | 7% | -17% | -74% | -2% | $3,579,684 |

| EMC | Everest Metals Corp | 0.095 | -10% | -17% | -5% | 2% | $13,061,745 |

| WML | Woomera Mining Ltd | 0.011 | 5% | 0% | -19% | -1% | $8,605,751 |

| KZR | Kalamazoo Resources | 0.09 | -3% | -14% | -53% | -12% | $15,262,538 |

| LMG | Latrobe Magnesium | 0.048 | -2% | 9% | -36% | -3% | $82,491,484 |

| KOR | Korab Resources | 0.017 | 0% | -6% | -39% | -1% | $6,239,850 |

| CMX | Chemxmaterials | 0.068 | -9% | -24% | -62% | -12% | $3,619,814 |

| NC1 | Nicoresourceslimited | 0.31 | 2% | -23% | -34% | -30% | $32,517,227 |

| GRE | Greentechmetals | 0.41 | 17% | 3% | 173% | 27% | $22,163,266 |

| CMO | Cosmometalslimited | 0.05 | 0% | -6% | -69% | -9% | $1,734,833 |

| FRB | Firebird Metals | 0.145 | -3% | 12% | -33% | -1% | $13,371,175 |

| S32 | South32 Limited | 3.315 | 3% | -2% | -8% | -69% | $15,057,457,526 |

| OMH | OM Holdings Limited | 0.445 | -2% | -3% | -29% | -25% | $343,459,852 |

| JMS | Jupiter Mines. | 0.1875 | -1% | -4% | -4% | -3% | $372,208,296 |

| E25 | Element 25 Ltd | 0.385 | 5% | -10% | -64% | -50% | $82,661,527 |

| EMN | Euromanganese | 0.115 | -8% | -18% | -57% | -24% | $28,120,200 |

| KGD | Kula Gold Limited | 0.014 | 8% | 8% | -56% | -1% | $5,224,967 |

| LRS | Latin Resources Ltd | 0.2375 | -5% | -3% | 107% | 14% | $679,264,019 |

| CRR | Critical Resources | 0.026 | -4% | -32% | -53% | -2% | $48,001,958 |

| ENT | Enterprise Metals | 0.004 | 0% | 0% | -56% | -1% | $3,197,884 |

| SCN | Scorpion Minerals | 0.051 | -7% | -7% | -27% | -2% | $17,682,016 |

| GCM | Green Critical Min | 0.008 | 0% | 14% | -33% | -1% | $9,092,680 |

| ENV | Enova Mining Limited | 0.006 | -14% | -14% | -54% | -1% | $3,845,576 |

| RBX | Resource B | 0.11 | 0% | -21% | 28% | 3% | $9,508,716 |

| AKN | Auking Mining Ltd | 0.044 | 0% | -31% | -63% | -5% | $7,755,941 |

| RR1 | Reach Resources Ltd | 0.012 | 9% | -17% | 140% | 1% | $38,403,565 |

| EMT | Emetals Limited | 0.007 | 0% | -13% | -42% | 0% | $5,950,000 |

| PNT | Panthermetalsltd | 0.073 | -3% | 4% | -60% | -12% | $4,525,100 |

| WIN | Widgienickellimited | 0.18 | -3% | -9% | -36% | -15% | $55,119,835 |

| WMG | Western Mines | 0.3 | -5% | 5% | 161% | 14% | $18,140,321 |

| AVW | Avira Resources Ltd | 0.002 | 33% | 0% | -33% | 0% | $4,267,580 |

| CAI | Calidus Resources | 0.19 | 23% | 23% | -45% | -8% | $118,996,216 |

| GT1 | Greentechnology | 0.41 | 4% | -2% | -56% | -42% | $88,385,672 |

| KAI | Kairos Minerals Ltd | 0.017 | -15% | -23% | -40% | 0% | $41,934,595 |

| MTM | MTM Critical Metals | 0.021 | -5% | -43% | -83% | -6% | $2,185,416 |

| NWM | Norwest Minerals | 0.0305 | -5% | 2% | -29% | -2% | $8,770,870 |

| PGD | Peregrine Gold | 0.285 | 1% | 14% | -34% | -10% | $15,194,955 |

| RAS | Ragusa Minerals Ltd | 0.045 | 32% | 22% | -80% | -7% | $5,418,754 |

| RGL | Riversgold | 0.009 | -10% | -31% | -78% | -2% | $9,036,984 |

| SRZ | Stellar Resources | 0.0085 | -15% | -29% | -29% | 0% | $9,883,678 |

| STM | Sunstone Metals Ltd | 0.017 | 13% | 0% | -47% | -2% | $55,475,728 |

| ZNC | Zenith Minerals Ltd | 0.082 | -14% | -25% | -71% | -18% | $31,361,899 |

| WC8 | Wildcat Resources | 0.745 | 11% | 67% | 2469% | 72% | $733,798,901 |

| ASO | Aston Minerals Ltd | 0.033 | -13% | 10% | -55% | -5% | $38,851,928 |

| THR | Thor Energy PLC | 0.027 | 8% | -29% | -61% | -3% | $4,761,086 |

| YAR | Yari Minerals Ltd | 0.017 | 13% | -6% | -32% | 0% | $8,200,083 |

| IG6 | Internationalgraphit | 0.18 | 9% | -3% | -41% | -9% | $15,127,979 |

| LPM | Lithium Plus | 0.45 | 18% | -4% | -20% | 8% | $31,674,336 |

| ODE | Odessa Minerals Ltd | 0.007 | 0% | -44% | -59% | -1% | $7,576,895 |

| KOB | Kobaresourceslimited | 0.07 | 4% | -13% | -59% | -7% | $7,379,167 |

| AZI | Altamin Limited | 0.06 | 2% | -8% | -29% | -2% | $23,111,288 |

| FTL | Firetail Resources | 0.1 | 0% | 1% | -38% | -6% | $16,379,611 |

| LNR | Lanthanein Resources | 0.007 | 17% | -13% | -76% | -1% | $7,851,029 |

| CLZ | Classic Min Ltd | 0.001 | 0% | 0% | -94% | -1% | $12,357,082 |

| NVX | Novonix Limited | 0.76 | 2% | -8% | -72% | -71% | $329,811,881 |

| OCN | Oceanalithiumlimited | 0.13 | -13% | -42% | -72% | -22% | $7,696,093 |

| SUM | Summitminerals | 0.095 | 2% | -17% | -47% | -5% | $4,241,484 |

| DVP | Develop Global Ltd | 3.29 | 11% | -5% | 25% | 11% | $664,545,410 |

| XTC | Xantippe Res Ltd | 0.001 | 0% | 0% | -76% | 0% | $17,528,005 |

| OD6 | Od6Metalsltd | 0.15 | -23% | -9% | -25% | -19% | $8,252,324 |

| HRE | Heavy Rare Earths | 0.09 | 64% | -1% | -45% | -3% | $5,443,914 |

| LIN | Lindian Resources | 0.17 | -8% | -21% | -17% | 2% | $184,307,558 |

| PEK | Peak Rare Earths Ltd | 0.385 | 0% | 3% | -10% | -7% | $108,503,001 |

| ILU | Iluka Resources | 7.26 | 6% | -5% | -16% | -227% | $3,084,473,866 |

| ASM | Ausstratmaterials | 1.4 | 9% | -4% | -29% | -4% | $235,153,083 |

| ETM | Energy Transition | 0.032 | -14% | -22% | -36% | -3% | $46,095,296 |

| VMS | Venture Minerals | 0.009 | -10% | -10% | -57% | -1% | $17,550,117 |

| IDA | Indiana Resources | 0.05 | 0% | -14% | -18% | -1% | $30,009,416 |

| VTM | Victory Metals Ltd | 0.28 | 30% | 51% | 47% | 6% | $20,224,914 |

| M2R | Miramar | 0.0215 | -37% | -39% | -76% | -5% | $3,424,000 |

| WCN | White Cliff Min Ltd | 0.01 | -17% | -9% | -47% | 0% | $12,570,186 |

| TAR | Taruga Minerals | 0.0105 | 5% | 17% | -67% | -1% | $7,060,268 |

| ABX | ABX Group Limited | 0.069 | -9% | -13% | -54% | -5% | $16,479,175 |

| MEK | Meeka Metals Limited | 0.039 | -7% | -15% | -33% | -3% | $47,438,357 |

| RR1 | Reach Resources Ltd | 0.012 | 9% | -17% | 140% | 1% | $38,403,565 |

| DRE | Dreadnought Resources Ltd | 0.033 | -8% | -30% | -71% | -7% | $110,622,250 |

| KFM | Kingfisher Mining | 0.14 | -7% | -24% | -74% | -34% | $8,057,250 |

| AOA | Ausmon Resorces | 0.0035 | 17% | 17% | -42% | 0% | $3,524,498 |

| WC1 | Westcobarmetals | 0.07 | 6% | -18% | -61% | -10% | $6,799,356 |

| GRL | Godolphin Resources | 0.038 | 6% | 3% | -58% | -4% | $6,092,713 |

| DM1 | Desert Metals | 0.039 | -7% | -7% | -90% | -16% | $2,829,102 |

| PTR | Petratherm Ltd | 0.044 | -14% | -20% | -27% | -1% | $10,338,552 |

| ITM | Itech Minerals Ltd | 0.125 | -11% | -6% | -58% | -14% | $14,662,027 |

| KTA | Krakatoa Resources | 0.025 | 32% | 14% | -61% | -2% | $10,437,550 |

| M24 | Mamba Exploration | 0.029 | -17% | -38% | -77% | -12% | $1,890,483 |

| LNR | Lanthanein Resources | 0.007 | 17% | -13% | -76% | -1% | $7,851,029 |

| TKM | Trek Metals Ltd | 0.046 | 0% | -16% | -27% | -3% | $24,882,004 |

| BCA | Black Canyon Limited | 0.15 | 0% | 25% | -38% | -9% | $9,846,657 |

| CDT | Castle Minerals | 0.01 | -9% | 0% | -57% | -1% | $11,757,430 |

| DLI | Delta Lithium | 0.575 | -2% | -23% | 6% | 10% | $312,252,304 |

| A11 | Atlantic Lithium | 0.4 | -10% | -16% | -44% | -22% | $229,590,623 |

| KNI | Kunikolimited | 0.275 | 4% | -15% | -59% | -24% | $20,617,504 |

| CY5 | Cygnus Metals Ltd | 0.175 | 46% | 9% | -63% | -21% | $55,108,101 |

| WR1 | Winsome Resources | 1.32 | 11% | -11% | 184% | 9% | $234,374,828 |

| LLI | Loyal Lithium Ltd | 0.48 | 14% | -27% | 9% | 19% | $33,789,764 |

| BC8 | Black Cat Syndicate | 0.21 | 14% | 0% | -29% | -15% | $64,659,771 |

| BUR | Burleyminerals | 0.215 | 13% | 19% | 10% | -1% | $21,272,319 |

| PBL | Parabellumresources | 0.345 | 0% | 0% | -23% | 1% | $18,879,263 |

| L1M | Lightning Minerals | 0.125 | -7% | 4% | 0% | -4% | $5,090,633 |

| WA1 | Wa1Resourcesltd | 9.33 | 76% | 81% | 652% | 794% | $361,034,703 |

| EV1 | Evolutionenergy | 0.155 | -9% | -6% | -39% | -7% | $28,058,039 |

| 1AE | Auroraenergymetals | 0.1 | 2% | -38% | -50% | -5% | $14,965,451 |

| RVT | Richmond Vanadium | 0.38 | 4% | 0% | 0% | 15% | $32,758,966 |

| PMT | Patriotbatterymetals | 1.09 | -6% | -12% | 0% | 34% | $413,876,571 |

| PAT | Patriot Lithium | 0.21 | 20% | 20% | 0% | -6% | $13,416,375 |

| BM8 | Battery Age Minerals | 0.21 | -2% | -22% | -58% | -29% | $18,718,746 |

| OM1 | Omnia Metals Group | 0.078 | 10% | -9% | -48% | -8% | $3,786,192 |

| VHM | Vhmlimited | 0.475 | 1% | -3% | 0% | 0% | $73,879,740 |

| LLL | Leolithiumlimited | 0.505 | 0% | 0% | -19% | 2% | $498,553,663 |

| SRN | Surefire Rescs NL | 0.016 | 14% | 14% | 23% | 0% | $26,478,958 |

| SRL | Sunrise | 0.705 | -10% | -8% | -65% | -122% | $65,414,936 |

| SYR | Syrah Resources | 0.6775 | -4% | 33% | -72% | -138% | $449,471,990 |

| EG1 | Evergreenlithium | 0.2 | -2% | -29% | 0% | 0% | $13,776,350 |

| WSR | Westar Resources | 0.0165 | -8% | -23% | -65% | -3% | $3,151,078 |

| LU7 | Lithium Universe Ltd | 0.038 | -7% | -27% | -5% | 1% | $14,375,310 |

| MEI | Meteoric Resources | 0.24 | 4% | 7% | 1900% | 19% | $475,828,496 |

| REC | Rechargemetals | 0.13 | -7% | -35% | -19% | -1% | $14,475,757 |

| SLM | Solismineralsltd | 0.26 | 21% | 8% | 300% | 19% | $18,651,409 |

| DYM | Dynamicmetalslimited | 0.18 | 13% | -12% | 0% | 0% | $5,775,000 |

| TOR | Torque Met | 0.18 | 13% | -48% | -3% | 0% | $23,531,627 |

| ICL | Iceni Gold | 0.061 | -9% | -20% | -13% | -2% | $14,631,286 |

| TMX | Terrain Minerals | 0.005 | 11% | 0% | -29% | 0% | $6,767,139 |

| MHC | Manhattan Corp Ltd | 0.005 | 0% | -29% | -29% | 0% | $14,684,899 |

| MHK | Metalhawk. | 0.1 | 18% | 5% | -46% | -7% | $8,664,811 |

| ANX | Anax Metals Ltd | 0.032 | -3% | -11% | -42% | -2% | $15,046,637 |

| FIN | FIN Resources Ltd | 0.031 | 41% | 158% | 35% | 1% | $19,252,096 |

| LM1 | Leeuwin Metals Ltd | 0.275 | -5% | 10% | 0% | 0% | $12,315,875 |

| HAW | Hawthorn Resources | 0.091 | 0% | -1% | 8% | -2% | $31,826,483 |

| LCY | Legacy Iron Ore | 0.017 | -6% | 6% | -6% | 0% | $108,916,045 |

What’s hot:

The week’s biggest gains

Bulletin Resources (ASX:BNR) +67%

Heavy Rare Earths (ASX:HRE) +64%

Larvotto Resources (ASX:LRV) +60%

What’s not:

The week’ s biggest falls

Miramar Resources (ASX:M2R) -37%

Pan Asia Metals (ASX:PAM) -28%

Carnaby Resources (ASX:CNB) -25%

OD6 Metals (ASX:OD6) -23%

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.