Heavy rare earths prices are due some hefty gains in 2020, says Lynas

Pic: Tyler Stableford / Stone via Getty Images

Good news for our cabal of rare earths explorers – heavy rare earths (HREE) demand will continue to increase, driven by the nascent electric vehicle market.

$1.7 billion market cap rare earths producer Lynas (ASX:LYC) says market prices of dysprosium and terbium — used in clean energy tech — are increasing as the global supply of HREE decreases.

Companies often divide the 17 rare earths into HREE and light rare earths (LREE) based on atomic weight — but these are not formal groupings or applied consistently across the industry, according to Geoscience Australia. Just FYI.

In late 2018, so-called HREE dysprosium was labelled the “dark horse in the rare earth stakes” by New York investment bank Hallgarten and Company as the rapid growth in the EV market spurred higher projections for demand.

It’s used in the permanent magnets required for the motors in EVs, with each one containing roughly 100 grams of dysprosium.

“HREE supply has been reduced as the China central government reduced mining quotas for ionic clay (the main source of HREE in China) due to environmental concerns and the recent ban on imports of similar material from Myanmar,” Lynas says.

“As the future growth of the EV market is expected to translate into a sharp increase in demand for dysprosium and terbium, the market is anticipating this future shortage and most industry participants expect HREE prices to continue increasing.”

Meanwhile, Lynas says the Chinese LREE market is currently oversupplied with concentrate from the US and Africa, leading to continued weak prices.

But it’s not that simple, says Richard Brescianini, general manager of exploration and development at advanced explorer Arafura (ASX:ARU).

“There is oversupply of La [lanthanum], Ce [cerium], Sm [samarium], Eu [europium], Gd [gadolinium] and Y [yttrium],” he told Stockhead.

“The remainder are tight.”

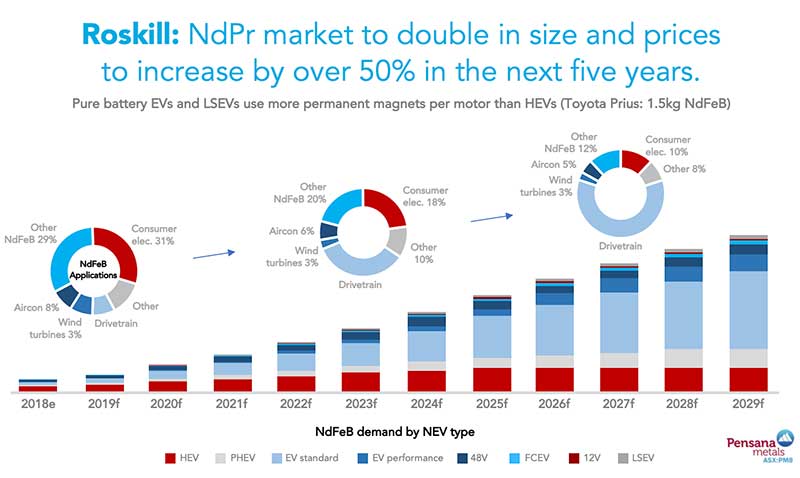

That includes LREE’s NdPr which, like dysprosium, are crucial to the EV thematic.

“Demand is surging for Nd and Pr [both LREEs] — as for Dy [dysprosium] and Tb [terbium] — both inside and outside China,” Brescianini says.

“All of these REEs find their main application in NdFeB permanent magnets.”

Globally, cumulative electric vehicle sales are expected to pass 10 million this year, 30 million by 2025, and 54 million by 2030, according to Argus Media.

Not all of these will use rare earths magnets but still, that’s a lot of looming NdPr demand.

And there’s a number of explorers positioning themselves to ride this wave.

Alongside Arafura’s NdPr-rich Nolans project in the Northern territory and Alkane’s (ASX:ALK) non-core Dubbo project in NSW are a slew of advanced WA players, including Hastings Technology Metals (ASX:HAS), Northern Minerals (ASX:NTU), RareX (ASX:REE) and Red Mountain Mining (ASX:RMX).

Overseas, there’s Pensana’s (ASX:PM8) low-capex, high-margin Longonjo NdPr project in Angola and Greenland Minerals’ (ASX:GGG) Kvanefjeld project in southern Greenland. Both are at advanced stages of pre-development.

READ: Rare earths play Pensana spikes 12pc on Longonjo NdPr project study

And then there’s former graphite explorer Hexagon Energy (ASX:HXG) which recently expanded into US downstream rare earth processing.

In October, Hexagon executed a binding agreement to acquire a 49 per cent interest in an advanced, proprietary low-cost downstream REE separation tech called RapidSX.

“With front-end engineering design work commencing in early January 2020, we intend to have a RapidSX-based commercial demonstration plant fully operational — in North America — in Q4 2020, with a planned production capacity of between 60 and 80 tonnes per annum,” managing director Mike Rosenstreich said in December.

NOW READ: Tim Treadgold — Rare earths could be another ‘buy the sector’ situation

At Stockhead, we tell it like it is. While Arafura Resources is a Stockhead advertiser, it did not sponsor this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.