Has graphite got its groove back? 4 ASX stocks explain the impact of China’s export restrictions

Pic via Getty Images

China’s control over the graphite supply chain is nothing new.

As the world’s top graphite producer and exporter, China dominates every stage of the supply chain from feedstock material to active anode material production (AAM), accounting for more than 90% of the world’s graphite refining.

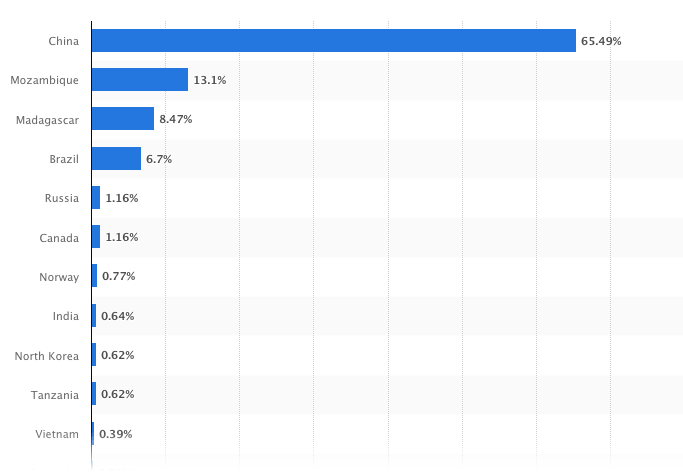

China’s output was estimated at 850,000t of graphite in 2022 (or almost 65.5%) according to Statista, making the other top countries like Mozambique (117,416t) and Madagascar (110,000t) look tiny in terms of natural graphite production.

The supply chain is so heavily concentrated that any move Beijing makes to weaponise its dominance has a trickle-down effect on graphite developers and explorers given there is currently nowhere else countries can get supply from.

While the US has realised this with the Inflation Reduction Act (IRA) to onshore supply chains, the problem with graphite is its complexity when it comes to manufacturing onshore.

To feed the burgeoning electric vehicle sector, graphite flakes undergo a micronising process before being further processed into spherical graphite for use in lithium-ion batteries.

Flake sizes of less than 150 micron (100 mesh) are preferred as larger flakes require a greater size reduction which incurs a higher cost.

Experts believe China’s move last month to introduce graphite export permits from December could potentially disrupt supply chains, raise costs, and affect production.

Others believe it presents an opportunity for countries outside of China to diversify their sourcing and reduce dependence on the Middle Kingdom.

But for so long now, graphite has been the forgotten commodity in the battery revolution.

With no significant supply disruptions for a decade, Benchmark Mineral Intelligence CEO Simon Moores says graphite has not had a price spike akin to lithium, cobalt and nickel and therefore slipped under the radar of battery makers, OEMS, and Western governments.

Has the turning point for the material finally come and if so, what makes this time different?

Stockhead sat down with four ASX graphite stocks to get their read on the situation.

Graphite stocks on the ASX

| CODE | COMPANY | PRICE | 1 WEEK RETURN % | 1 MONTH RETURN % | 6 MONTH RETURN % | 1 YEAR RETURN % | MARKET CAP |

|---|---|---|---|---|---|---|---|

| BAT | Battery Minerals Ltd | 0.042 | -11% | 50% | -60% | -72% | $5,023,388.92 |

| EVG | Evion Group NL | 0.038 | -8% | 12% | -21% | -62% | $13,146,449.10 |

| BKT | Black Rock Mining | 0.115 | -4% | 35% | -13% | -32% | $126,191,758.83 |

| GW1 | Greenwing Resources | 0.135 | 4% | 0% | -43% | -60% | $23,523,950.07 |

| EGR | Ecograf Limited | 0.215 | 21% | 58% | 21% | -39% | $97,307,253.60 |

| MNS | Magnis Energy Tech | 0.049 | -36% | -36% | -76% | -88% | $58,775.40 |

| MRC | Mineral Commodities | 0.032 | 0% | 8% | -26% | -51% | $27,529,798.43 |

| RNU | Renascor Res Ltd | 0.165 | 10% | 43% | -25% | -31% | $431,699,274.66 |

| SYR | Syrah Resources | 0.7625 | 11% | 66% | -18% | -71% | $513,682,274.80 |

| TLG | Talga Group Ltd | 1.09 | 3% | -7% | -27% | -23% | $393,222,047.00 |

| TON | Triton Min Ltd | 0.023 | -12% | 15% | -33% | -12% | $39,033,990.15 |

| WKT | Walkabout Resources | 0.165 | 32% | 50% | 65% | -5% | $110,014,583.00 |

| VRC | Volt Resources Ltd | 0.006 | -14% | -25% | -50% | -67% | $26,471,683.78 |

| AXE | Archer Materials | 0.41 | 3% | -10% | 6% | -37% | $103,213,040.27 |

| HXG | Hexagon Energy | 0.01 | 25% | 5% | -33% | -38% | $4,616,243.11 |

| LML | Lincoln Minerals | 0.0065 | -19% | -7% | -57% | -5% | $11,623,583.43 |

| KNG | Kingsland Minerals | 0.27 | 4% | 38% | 42% | 42% | $13,826,177.40 |

| ITM | Itech Minerals Ltd | 0.145 | 12% | 21% | -34% | -55% | $17,105,698.68 |

| SVM | Sovereign Metals | 0.465 | -9% | 21% | 11% | 17% | $261,796,581.00 |

| LEL | Lithenergy | 0.6 | -13% | 13% | -15% | -43% | $61,806,000.00 |

| EV1 | Evolutionenergy | 0.135 | -16% | -16% | -44% | -50% | $23,673,970.44 |

Companies in advanced stages of development to benefit

EcoGraf (ASX:EGR) is the only graphite stock looking to take advantage of oncoming graphite demand with three standalone businesses – mining, processing, and recycling.

Using its HFfree purification technology, EGR plans to upgrade flake graphite to produce 99.95% battery anode material at its Product Qualification Facility (PQF) in Western Australia, which is expected to be commissioned in the first quarter of ’24.

The facility, jointly funded through the Commonwealth Government’s $48.8m critical minerals development program, will be the first of its kind outside China and will source high-purity graphite feedstock from the long-life Epanko graphite project in Tanzania. The company’s been around well before the last graphite boom went bust in 2017.

EGR managing director Andrew Spinks believes it’s been a long time coming but the graphite market is finally at a turning point.

“There’s been a level of comfort that comes with China having a huge endowment of graphite readily available,” he says in an interview with Stockhead.

“The issue for the rest of the world is it’s at low sustainable production levels and the EV manufacturers are now demanding high ESG requirements, which heightens the importance of new supply chains outside of China.

“Up until now, the world hasn’t given much attention to the anode supply chain but we’re going to see greater support now for alternate material,” he says.

With the effects of the IRA and EU Green Deal coming into play from 2025/2026, Spinks says China’s graphite curbs – similar to those imposed on gallium and germanium three months ago – will trigger interest from the EV and battery supply chain.

“This is a long-term gain, given the time it takes to fully transition from combustion motors to electric vehicles,” he says.

“And any company that is advanced to a development stage or is in production will be directly impacted by this move.”

Longer term picture: China to look outside borders for raw materials

Backed by Japan’s largest chemical corporation Mitsubishi Chemical, $419m market cap company Renascor Resources (ASX:RNU) is in the advanced stages of development at its Siviour project on South Australia’s Eyre Peninsula.

The company plans to integrate Siviour with a downstream manufacturing facility that will produce purified spherical graphite (PSG) that is used in the anodes of lithium-ion batteries.

While Sivour already holds the largest graphite ore reserve outside of Africa, recent resource expansion drilling increased resources some 25% to 123.6Mt at 6.9% TGC, or 8.5Mt of contained graphite, with 61% of that in the higher confidence Measured and Indicated categories.

RNU managing director David Christensen says most of the initial commentary on China’s graphite restriction centred on the possibility that this was a retaliatory action by China as part of larger trade issues, but this is likely partly true.

“The decision to focus on graphite is likely reflective of China having a larger demand for graphite than supply,” he says in an interview with Stockhead.

“Its dominance in the mid-stream processing of graphite has driven graphite prices down as Chinese companies jockey for market share at the expense of margin.

“By restricting graphite exports, Chinese companies will benefit from these temporary low prices,” he says.

“In the longer term as Chinese EV demand rebounds and more battery minerals like graphite are needed, China will need to look outside of its borders for raw materials.

“Much like the end of 2022, this should lead to increased graphite prices and make it easier for new projects outside of China to get started.”

An extra boost to the critical minerals sector

Kingsland Minerals (ASX:KNG) is prepping its Leliyn graphite project in the Northern Territory for an initial resource estimate in the first quarter of ’24 from an established Exploration Target of 200-250Mt grading 8% to 11% total graphitic carbon (TGC).

The target sits along 20km of graphitic schist, which co-hosts significant levels of gallium used in semiconductors and electronic equipment.

KNG managing director Richard Maddocks says the initial short-term impact of the restrictions so far has been increased interest in graphite, reflected in the share price surge of many ASX stocks.

“We’ve had a lot of interest with people ringing up,” he says.

“The situation has shone a light on how much China has a monopoly on the supply chain and it could help to promote funding into new graphite projects,” he says.

“Since the announcement, we’ve already seen the Federal Government come out with their Critical Minerals Fund – an extra $2 billion – which isn’t a direct result of the export controls but goes to show Australia is getting serious about supporting these projects.”

Graphite offtake agreements to come

iTech Minerals (ASX:ITM) is another near-term graphite play with an established battery-grade resource, permitted mining lease and resource expansion drilling program in full swing at its Campoona project on South Australia’s Eyre Peninsula.

ITM managing director Michael Schwarz says near-term producers of battery quality graphite products are likely to see a significant increase in offtake agreement enquiries.

“These agreements are essential to establishing the infrastructure to move up the supply chain from graphite concentrate to purified spherical graphite production,” he says.

“The Chinese Government has strongly signalled that the recent growth in supply from synthetic graphite producers in China is likely to be consumed within Chinese markets, leaving battery producers outside of China at risk of supply deficits.

“ASX companies with proven battery grade graphite projects with plans to build vertically integrated supply chains to supply battery anode material are likely to become a hot commodity for the ever expanding list of battery manufacturers outside of China.”

Graphite stocks share prices today:

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.