Ground Breakers: ‘No solution without nuclear’ – Canadian giant Cameco ratchets up bullish commentary, ASX stocks move higher

Pic: Stockhead, Via Getty Images

- Cameco boss Tim Gitzel says there’s “no solution without nuclear” as green energy and Russian sanction put rocket up uranium market

- Aussie uranium stocks move higher on positive chatter

- Gold miners report as prices lift overnight despite 0.75% rate rise in the States

Uranium bulls were rejoicing today on the back of some very bullish commentary from global yellowcake giant Cameco.

The Canadian nuclear fuel behemoth released its quarterly results overnight in North America, and the response was almost instantaneous, sending pretty much every western uranium stock flying.

The company is relaunching its mothballed Macarthur River and Key Lake operations, planning to reinstate 15Mlbs of their 25Mlb capacity by 2024, but even bigger is the shift away from Russian production, which is providing more – ahem – fuel for the uranium bull case.

Russia is a big factor here, Cameco CEO Tim Gitzel says.

He thinks the outlook for nuclear power is strengthening as governments look to balance out their clean energy prerogatives with the need to accelerate the shift from Russian energy supply. In short, Gitzel says, there’s “no solution without nuclear”.

“Suffices to say we are seeing governments and companies turn to nuclear with an appetite that I’m not sure I have ever seen in my four decades in this business,” he said.

“Therefore, it is easy to conclude that the demand outlook is durable and very bright. But supply is quite a different picture.”

Russia’s invasion of Ukraine has the potential to increase chances of a supply shock.

“For some time now, we have said that we believe the uranium market was as vulnerable to a supply shock as it has ever been due to persistently low prices. Low prices have led to growing supply, concentration by origin, and a growing supply gap,” he said.

“And unlike in the past, we don’t have the same stock of secondary supplies to fill the gap.

“After years of drawing on these onetime sources, the secondary supply capacity is now declining significantly into the future and productive capacity is not poised to respond.”

Canary in the uranium mine

The canary in the coal mine is already being seen not in the supply of raw materials, but in the conversion market, where prices are at record highs.

Gitzel notes that the global nuclear industry relies on Russia for approximately 14% of its supply of uranium concentrates, 27% of conversion supply, and 39% of enrichment capacity.

Cameco believes uranium (its prices were already up 41% year on year in the June quarter) will follow.

“It is still early days, but we are already seeing some utilities beginning to pivot toward procurement strategies that more carefully weigh the origin risk. They are working their way through their fuel supply chains to determine, where there are vulnerabilities,” Gitzel said.

“As a result, we have temporarily seen their focus shift from securing uranium to the more immediate need in their supply chain for enrichment and conversion services, where Russian capacity plays a much bigger role.

“So make no mistake.

“We expect uranium will follow. After all, it is the product to which all services are applied.

“With more than 45 million pounds in new uranium contracts added to our portfolio since the beginning of the year 2022 has already been a contracting success, and we continue to have a significant and growing pipeline of contract discussions underway.”

Uranium stocks fire up

Cameco CFO Grant Isaac told analysts the power of western utilities meant western capacity would be sought and identified to fill the necessary supply in a “bifurcated market”.

It came amid reports Germany, which had previously planned to shutter its remaining nuclear power plants in 2022, is looking to expand production capacity to shift away from Russian coal and gas.

JUST IN – Germany could restart three more nuclear power plants, in addition to the three that are still in operation, within “a few months or weeks,” says the chief of the Technical Inspection Association (TÜV).

— Disclose.tv (@disclosetv) July 26, 2022

Cue a green rush for uranium stocks this morning.

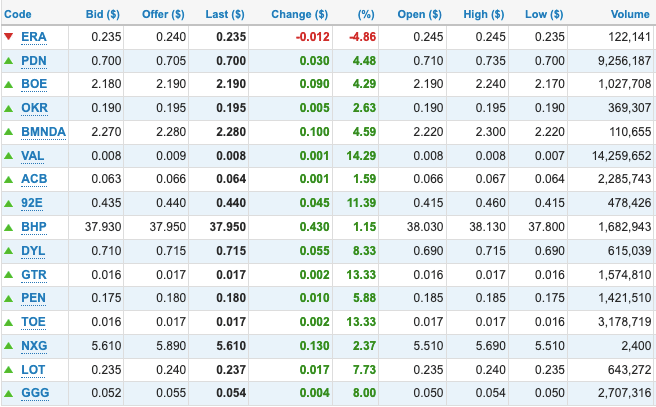

Here’s a grab bag of ASX uranium plays, including all the big boys.

Paladin Energy (ASX:PDN), Boss Energy (ASX:BOE) and Deep Yellow (ASX:DYL), which sealed its scheme merger with Vimy Resources yesterday, were all up.

Only Rio Tinto backed ERA (ASX:ERA), which is struggling to get shareholders to back a fundraising needed for the rehab of its Ranger uranium mine in the NT, is heavily in the red.

Spot uranium prices have recovered over the past few years from cyclical lows of ~US$18/lb to a tick under US$50/lb, encouraging Paladin and Boss to announce the restarts in recent months of the Langer Heinrich and Honeymoon uranium mines.

Uranium stocks share prices today:

Goldies and copper stocks report results

Gold miners were looking solid this morning as prices lifted towards US$1740/oz despite the US Fed announcing another 0.75% rate rise.

A handful had some results out this morning as the rush comes on for late quarterly reports.

Ramelius Resources (ASX:RMS) hit updated guidance of 258,625oz at all in sustaining costs of $1523/oz, after June quarter production of 67,418oz at $1564/oz despite the impacts of WA’s Covid outbreak.

RMS says it will produce 240,000-280,000oz at $1750-1950oz in FY23 including 150,000oz at Mt Magnet and 110,000oz at Edna May. Those costs seem like a big leap even in the current inflationary environment.

Meanwhile, it has delivered its first resource upgrade at the Rebecca mine acquired from Apollo Consolidated last year, increasing overall resources by 9% to 1.2Moz and indicated resources by 22%.

Gold Road Resources (ASX:GOR) was up after announcing record production at the Gruyere gold mine of 85,676oz at $1250/oz, setting it up well for its 2022 production guidance of 300,000-340,000oz at $1270-1470/oz.

Gold Road shares Gruyere in a 50-50 JV with South Africa’s Gold Fields.

Gold Road increased its cash and equivalents to $161.3m with record feee cash flow of $43.6m before dividends of $3.7m and $12.2m associated with its takeover of DGO Gold.

Copper miner Sandfire Resources (ASX:SFR) said its group production exceeded guidance at 98,367t of copper, 38,907t of zinc, 4102t of lead, 1.5Moz silver and 32,285oz gold at cash costs of US$1.27/lb copper.

That included five months at the MATSA copper operations in Spain of 30,628t Cu, 38,907t Zn, 4,102t Pb and 1.2Moz Ag and full year production at DeGrussa of 67,740t Cu, 32,285oz Au and 0.3Moz Ag.

That underpinned sales revenue of US$922.7m for FY22 and EBITDA of US$448m.

Sandfire expects to produce 81-89,000t of copper, 78,000-83,000t of zinc, 6-10,000t of lead, 10-12,000oz of gold and 2.2-3.2Moz of silver in FY23 at C1 operating costs of US$1.57/lb, as its DeGrussa mine in WA winds up and is replaced by MATSA in Spain as the main contributor.

Goldies share prices today:

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.