Ground Breakers: Iron ore up 20% in 3 weeks as experts say China’s ‘soft landing’ could create deficit in 2023

Pic: Kseniya Ovchinnikova/Moment via Getty Images

- Iron ore futures have sunk this morning on new Covid concerns in China

- But prices have risen 20% in the past three weeks, with ANZ now expecting a deficit on rising steel output expectations in the Middle Kingdom

- Poseidon Nickel posts feasibility study in plan to become next nickel sulphide producer

Iron ore prices are down this morning on the latest bad Covid news out of China, with tighter restrictions to cases in Beijing and the first death in six months in an 87-year-old man.

Despite the steam given to commodity markets from the unwinding of aspects of China’s Covid rules, China’s hardline policy remains in place.

Another factor is India, which could ship more iron ore into the seaborne market after its government responded to iron ore producers’ request to scrap an export tax on lower grade iron ore.

That said, measures designed to remove some of the strictures of the Covid Zero policy, like reducing quarantine times for overseas arrivals and mass testing, as well as policy support for property developers, have supported a rebound in the key commodity trade of iron ore.

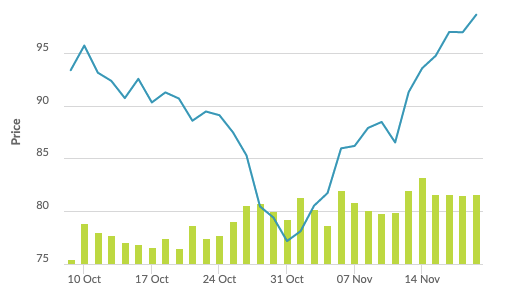

Check out this graph from the Singapore Commodity Exchange to peep the volatility. Iron ore is up around 20% since hitting their 2022 nadir at the end of October.

While the news today is bearish, with Fortescue Metals Group (ASX:FMG), BHP (ASX:BHP) and Rio Tinto (ASX:RIO) all in the red, and the Materials sector 1.37% lower, the longer term outlook may well be brighter.

Experts now say the iron ore market could flip into deficit next year, ramping up Chinese steel production expectations.

“The risk of a hard landing in the property sector was too great to ignore. This formed the basis of our estimate for China’s steel output in 2023 at 1,010Mt With the risks now tilted to a softer landing, we have revised up our forecast for steel production next year,” ANZ’s Daniel Hynes and Soni Kumari said last week.

“We now expect China’s steel production to rise 2.5% to 1,050Mt.

“This has big implications for the iron ore market. After previously expecting the market to return to surplus in 2023, we now see it remaining in deficit. That should support iron ore prices.”

Mill margins more positive

Iron ore prices have followed rebar pricing in the past three weeks, which have lifted from year lows and sent Chinese factories back into positive territory.

Commbank mining analyst Vivek Dhar says both hot rolled coil and rebar producers are generating profits for the first time since mid-August.

“The rebound in prices reflects an increase in China’s steel mill margins – a key driver of iron ore prices in the short term,” he said in a note this morning.

“The lift in China’s steel mill margins can mostly be attributed to a lift in steel prices in China, as demand hopes have lifted after policymakers in China eased some COVID‑zero rules and provided a rescue package for its property sector on 11 November.”

“HRC, which is used more in the manufacturing sector, has struggled to remain profitable this year. HRC margins have been in negative territory for ~58% of 2022 to date and indicates the demand pressure being faced by the manufacturing sector.

“And while demand hopes in China have boosted HRC steel prices, external pressures have been weighing on demand for China’s manufactured goods for some time.”

However, Dhar warned iron ore could be tested by rising case numbers and the Beijing death, saying continuing rollback in Covid-Zero measures would be needed to prop up recent gains.

Iron ore majors share prices today:

Poseidon aiming for title as Australia’s next nickel sulphide producer

15 years after Poseidon Nickel (ASX:POS) emerged from the shell of Niagara Mining with plans to revive the old Windarra nickel mine, it has laid out plans to become “Australia’s next nickel sulphide concentrate producer”.

If best laid plans come to fruition it will do so not at Windarra, the project at the centre of the Poseidon Bubble of the late 1960s, but at Black Swan, picked up from Norilsk in 2014.

A feasibility study today placed a $248 million pre-tax NPV and 103% internal rate of return on a plan to reopen the Black Swan mine and concentrator at a processing rate of 1.1Mtpa and current spot nickel prices of ~US$11.80/lb.

That would deliver 5Mt of feed over four years to produce 200,000t of concentrate and around 30,000t of contained nickel from within a reserve of 3.5Mt at 1% Ni for ~35,000t.

POS suggests it will cost only around $50 million to return Black Swan to production, including $38m for the refurbishment of the concentrator, located around 50km north-east of Kalgoorlie-Boulder, along with opex of US$4.90/lb (all in sustaining cost).

An FID is expected in the first half of 2023 with concentrate production to begin in early 2024, in a bid to take advantage of the current strong price environment for nickel.

It has become one of the key metals for the energy transition and a sought after M & A target, with RFC Ambrian projecting the need for class 1 nickel for electric vehicle batteries will grow by 0.7-1.1Mt a year by 2030.

A feasibility study on a larger scale 2.2Mtpa operation utilising the whole processing plant and producing a rougher concentrate with talc carbonate ore that has lower grades and higher magnesium compared to smelter specifications, but could be sold to a proposed pre-cursor refinery in Kalgoorlie or HPAL plants.

Poseidon Nickel (ASX:POS) share price today:

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.