Ground Breakers: Contractors bullish on mining as they eye multi-billion $$$ iron ore and lithium splurge

Pic: RyanJLane/E+ via Getty Images

- NRW toasts growth prospects in Australian mining industry as iron ore and lithium players plan billions in capex

- Rare earths giant Lynas hints at potential dividends at 2023 AGM

- Gold sub-index up over 4% as prices rose to US$2025/oz and beyond

Enthusiasm for the mining sector has been waning for much of 2023, with falling commodity prices — outside iron ore, gold and uranium — placing a question mark over growth plans across the sector.

While it has been a common refrain to talk about the need to find and develop critical minerals like lithium, nickel and copper, prices and bearishness about the broader economy amid rate rises and both global and Chinese economic uncertainty have hurt the market.

Among those concerns have been a more than 75% fall in a variety of lithium indices, with most of the producers down in 2023 so far.

At the same time margins remain strong even at prices below US$1600/t (compared to sales prices of around US$6000/t for spodumene concentrate early this year).

And those in the know say investments in new production will continue ahead of massive shortfalls of the lithium needed to meet EV sales targets later in the decade.

Contractors are among the cohort trying to capture and hold some of that value, with one giving an indication of the wall in capital to be spent on Australian mines in the coming years.

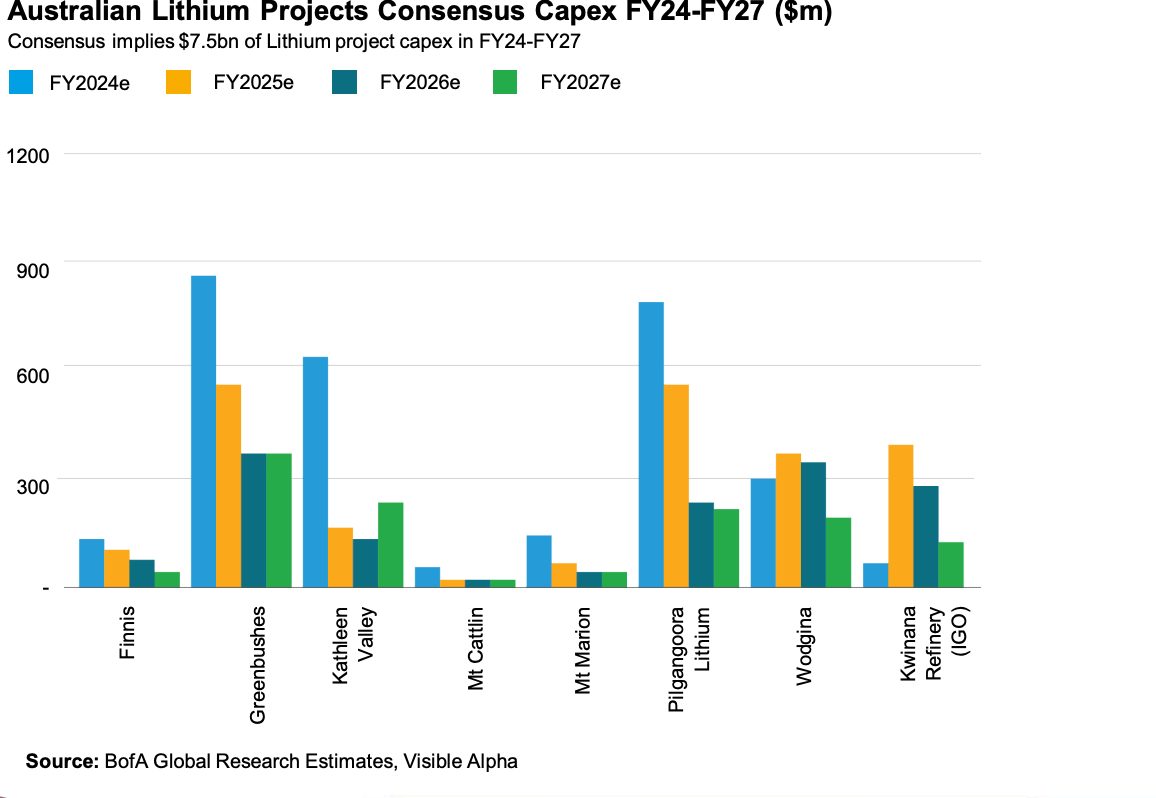

NRW Holdings (ASX:NWH) is presenting its AGM in Perth today, and there CEO Jules Pemberton is planning to wax lyrical on the opportunities coming up for mining services firms, including $7.5 billion of lithium project capex coming in the next four financial years.

That’s right: $7.5b in Australia alone.

“Outside of the iron ore capex cycle, the Australian Lithium sector is expected to continue to its capital expansion with A$7.5B of lithium project capex in the period FY24 to FY27,” he will say.

“Established lithium producers are planning to increase production capacity through expanding existing mining operations or transitioning underground.

“Capacity expansion creates surface mining/drill and blast opportunities for NRW,

together with process plant design and construction and operations and maintenance opportunities.”

Iron ore miners returning to major projects

That comes alongside a renewed boom in Pilbara iron ore operations, where Rio Tinto (ASX:RIO), BHP (ASX:BHP) and Fortescue (ASX:FMG) expect to expand output across the rest of the decade.

“Recently all of the three major Pilbara iron ore producers have announced very

significant growth and sustaining capital expenditure programs – which we believe

promotes a very positive outlook for NRW,” Pemberton noted.

NRW has diversified of late, but is targeting more work in the iron ore sector, expecting capex for BHP, Rio and FMG to rise at a CAGR of 6% from FY23 to FY26, with combined output from the Aussie giants expected to lift beyond 1Btpa later this decade.

“However, in the context of the group’s record FY23 results, what is interesting to note is the share of revenue that was derived from Pilbara iron ore projects.

“In FY21, over 20% of the group’s revenue – around $500m – came from Pilbara iron ore projects. However, in FY23 only 9% of revenue was derived from Pilbara iron ore projects.

“Again, this speaks to the success of the group’s diversification strategy, where we can deliver record financial performance but with greatly reduced reliance on a market that has historically been a key driver of the group.

“So, with the continuation of our diversification strategy and an iron ore sector that is commencing a major phase of multi-year capital development, NRW’s potential for growth over this next phase of Pilbara iron ore development is significant.”

NRW expects to hit $2.9 billion in revenue in FY24, with EBIT expected to be at the high end of the guidance range of $175-185m.

Director Peter Johnston retired as a director ahead of today’s AGM.

$1.25 billion NRW’s shares are down 2.15% YTD, but up over 3% today.

NRW Holdings (ASX:NWH) share price today

Dividends on the cards for Lynas Rare Earths?

Lynas Rare Earths (ASX:LYC), which made over $310 million in profit in FY23 and was sitting on $903 million of cash at the end of the last financial year, has flagged plans to introduce a capital management and potential dividend policy as it comes towards the end of the $730 million development of its Kalgoorlie cracking and leaching plant.

The firm has also been buoyed by a Malaysian backflip to remove licence conditions that would have prevented it importing lanthanide concentrate to its Kuantan plant as the cash rich miner, which has never paid a dividend, moves into a new phase.

It is also spending upwards of $500 million on an expansion of the Mt Weld mine, the largest source of rare earths outside China, as it looks to ramp up its concentrate feedstock equivalent of neodymium-praseodymium oxide to somewhere in the vicinity of 12,000tpa by 2025.

Speaking at its AGM in Sydney today, outgoing chair Kathleen Conlon said a plan for dividends was now in the works, with the 12-year director also handing over the chair to longstanding director John Humphrey today.

“Since 2021, we have been focused on employing capital on execution of major growth projects to ensure Lynas can retain its share in a growing market. As we bring our major projects in Kalgoorlie, Mt Weld and Kuantan to a close we will be announcing a revised capital management policy, including a dividend policy,” she said.

Despite stockpiling non-contracted material this year to hold out for higher prices, CEO Amanda Lacaze said prices were not bad by historical standards in FY23, though they did fall from FY22’s record highs.

NdPr demand, increasingly coming from EVs and wind turbines, has lifted 45% since 2019 according to Lynas, though growth rates have slowed in 2023 due to weakness in the Chinese economy.

“We see this trend continuing and of course that’s a reason why we are reinvesting in assets in the business to be able to meet demand as it continues to grow,” she said.

“In 2023, demand has been more moderated and that really has reflected in particular some of the economic situation … in China, but we expect the growth to accelerate right through to 2030.

“I can remember in 2015 dreaming of the day that we would have US$65 NdPr prices, so we as a business can operate efficiently and successfully when the price is lower. We just are more successful when it is higher.”

On the markets today, the materials sector lifted a mild 0.27%, but a gold bump was in full swing with Newmont (ASX:NEM) up over 5% and the ASX gold sub-index up 4.23% after suggestions the US Fed could begin rate cuts in 2024.

Gold hit US$2025/oz according to the LBMA yesterday, around $50 shy of the all time high.

Ground Breakers share prices today

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.