Ground Breakers: Coal price hits New Hope earnings as copper and iron ore snatch Chinese hope bump

Pic: Eugene Mymrin/Moment via Getty Images

- New Hope says Newcastle coal prices will be supported at current levels after earnings drop

- Materials stocks lift strongly as China emerges from New Year cocoon

- Greenbushes latest lithium mine to look at underground development

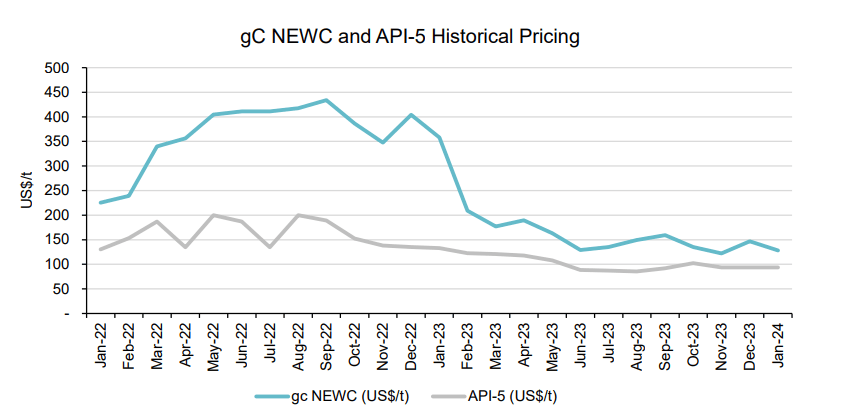

New Hope Corp (ASX:NHC) is confident Aussie thermal coal prices have found a floor as they converge with low energy coal pricing in China.

The New South Wales and Queensland focused coal digger saw underlying EBITDA fall 26.5% in the January quarter to $179.9 million on lower prices, with underlying EBITDA some 59.1% down for the first half to $424.8m.

NHC’s earnings eclipsed $1b as prices raged in the first half of FY23 following Russia’s invasion of Ukraine.

But two mild Northern winters have seen demand for thermal coal slide. First half saleable coal output from New Hope’s Bengalla in the Hunter, plus early tonnes from its New Acland mine in Queensland, came to 2.049Mt for the quarter and 4.093Mt for the half year, the latter number up 29% YoY.

But pricing slid from $211.40/t in the October term to just $180.64/t in January. That came as the GlobalCoal Newcastle benchmark dropped 10.6% to US$132.41/t, 64.2% down on the extraordinary prices seen at the same time a year prior.

However, New Hope says the convergence of 6000kcal Newcastle quality coal with lower quality ‘API-5’ pricing would support Aussie exports, with Bengalla capable of also switching between the two grades.

“A mild winter in the Northern Hemisphere has resulted in soft demand, placing downward pressure on coal prices,” NHC said in its quarterly report.

“High energy products have seen greater demand destruction compared to the API-5 price which has remained stable due to strong Chinese demand for lower energy coal supply.

“API-5 has created a floor for the gC NEWC and the expectation is that prices will stabilise at current levels. Bengalla Mine has the capability to alternate production between gC NEWC and API-5 with relative ease and we continue to optimise production and sales based on the margin rank determined from the changing pricing indices.”

New Hope’s shares fell into the red alongside other Aussie coal stocks, but it recorded a win on costs, which slid 4% to $80/t before State royalties.

The miner says it is on track to achieve cost guidance of $72-81/t as volumes increase in the second half.

Copper and iron ore see miners run higher

Copper, battery metals and iron ore companies led the ASX materials sector higher today, recording a 1.15% gain with Rio Tinto (ASX:RIO), South32 (ASX:S32), Pilbara Minerals (ASX:PLS) and MinRes (ASX:MIN) among the winners.

The run in big mining stocks came as China emerges from the Lunar New Year holiday, marking the end of a traditional slow period for commodity demand.

Production levels at industrial enterprises typically drop in the Chinese winter, with buying set to resume as inventories are wound down following the return to work.

Copper miners including Sandfire Resources (ASX:SFR) were also up strongly, with the ASX’s flagship red metal producer more than 3% higher.

“Copper recorded its biggest weekly gain in months as expectations of stronger demand in China rose. Construction activity should rise in coming weeks as the seasonal winter lull draws to an end,” ANZ’s Felix Ryan noted.

“Chinese markets reopen today following the week-long Lunar New Year holidays.

“Stronger consumption will be met by tight supplies, following a series of mine closures late last year. This has already seen smelter processing fees fall sharply in China.”

An exception was IGO (ASX:IGO), which fell back into the red after a massive gain on Friday as the Australian Government responded to the implosion of its nickel sector by placing the commodity on the critical minerals list, opening access to a $4 billion government grant facility and low cost loan programs.

The WA Government will also provide a 50% discount on nickel royalties for 18 months, in the hope a period of low prices sitting in the low US$16,000/t range can be seen off.

BHP (ASX:BHP) is expected to provide a fuller picture of its plans with the ailing Nickel West division in WA tomorrow in its half-year results, having already announced a US$3.5b pre-tax impairment which has placed the division and 3000 employees on notice with it now costing BHP US$300m to hold the assets on its books.

IGO also announced a 25% increase in mineral resources on a 6% spodumene concentrate basis at the Greenbushes mine in WA this morning. It holds 24.99% of the Talison JV alongside Albemarle and Tianqi — the world’s largest lithium asset.

The project now hosts 447Mt at 1.5% Li2O as of December 31, up from 347Mt at 1.5% Li2O at the same time a year earlier, an increase of 22Mt on an SC6 basis.

Reserves rose 4% from 171Mt at 1.9% Li2O to 179Mt at 1.9% Li2O, equivalent to around 2Mt of extra spod, after 1.43Mt was produced — sourced from 3.5Mt of ore at 2.71% Li2O from open pit mining and 1.8Mt at 1.38% Li2O from retreated tailings.

The mine’s owners are now considering whether they can take mining operations underground, following in the footsteps of other miners either operating or planning underground lithium mines including Liontown Resources (ASX:LTR), MinRes, Core Lithium (ASX:CXO) and Arcadium (ASX:LTM).

“Greenbushes is an exceptional asset with over 23 years of life defined by the current Ore Reserve at expanded throughput capacity,” IGO’s MD Ivan Vella said.

“The investment in the drilling to understand the potential of this deposit continues to return exceptional results, with mineralisation remaining open in all directions.

“With this improved understanding of the orebody coupled with underground mining studies will only continue to improve the status of this operation as the world’s best hard-rock lithium mine.”

Ground Breakers share prices today

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.