EY survey highlights the biggest risks facing the mining sector

Here are the top risks as voted on by global mining executives Pic: Getty Images

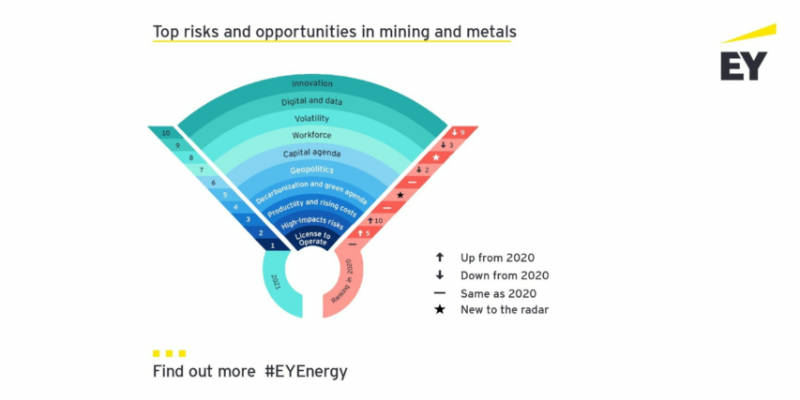

The global COVID-19 pandemic has altered the perception of the biggest risks facing the mining sector in the next 12 months, though the top risk has remained unchanged for a third year in a row.

In its ‘Global mining and metals Top 10 Business Risks and Opportunities – 2021’ survey of 250 global mining executives, consultancy EY noted that licence to operate remained the top risk for the third year in a row.

High-impact risks along with productivity and rising costs were named as the second and third greatest risks for the industry, a change from last year’s workforce future and digital and data optimisation concerns.

EY says the change reflects how COVID-19 has disrupted commodity demand and prices and prioritised different risks.

It added licence to operate, disruption, environment and geopolitical risks were all becoming more prominent as social responsibility and broader stakeholder demands intensified.

“The industry has dealt with the impact of the COVID-19 pandemic extremely well, leading a prompt and effective response that allowed many mines to continue operating,” EY Global Mining & Metals Leader Paul Mitchell said.

“However, maintaining business continuity has come at a cost, with mines facing added expenses relating to new procedures and protocols, the introduction of health testing equipment and ensuring that the workforce is supported appropriately.

“At the same time, the pandemic has heightened stakeholder expectations around how miners prepare for, manage and monitor all high-impact risk exposures.”

Greater geopolitical risks

The study also found that geopolitical issues are a top concern as the shifting balance of power between the world’s largest economies changes industry dynamics.

It also highlighted concerns about how a rise in domestic protectionism in the wake of COVID-19 could affect miners’ ability to operate in key markets.

“Mining is a global industry and it requires a global mindset to excel. We’ve already seen some governments move to impose tariffs or even export bans to protect domestic producers,” Mitchell noted.

“Fifty six per cent of the survey respondents expect to see royalties and taxes increase as governments seek to raise revenue in response to the pandemic.”

The digital age is here

While last year’s survey held digital and data optimisation as one the top three risks, it has since fallen to ninth position.

“The lower ranking of issues like digital and data optimisation indicates that miners are now more confident in managing these risks,” Mitchell said.

“For many, they are considered business as usual, and for others they represent a key opportunity.”

Environment and climate could create new opportunities

The study found that slow or inadequate progress on plans to decarbonize operations might threaten the ability of companies to access capital in an increasingly tight market.

Increased stakeholder scrutiny of corporate behaviour seen during the COVID-19 pandemic is likely to continue post-pandemic, with significant implications for how mining and metals companies manage issues surrounding environmental, social and governance (ESG).

Locally, this is best highlighted by the uproar caused by Rio Tinto’s (ASX:RIO) destruction of a 46,000-year-old aboriginal heritage site in WA.

However, this could prove to be a boon, with Mitchell saying that companies with a strong focus on ESG could gain a competitive edge in the fight for capital.

Accelerating innovation

The study also found that companies can broaden the scope and increase the effectiveness of their innovation agenda by building on the rapid pivot response that the industry has already adopted to address the impact of COVID-19.

“The industry response to COVID-19 is acting as a catalyst to apply more creative, agile solutions to long-standing challenges around health and safety, the cost of energy and engagement with local communities,” Mitchell added.

“There is a huge opportunity to remove complexity, overcome historical obstacles to change, and accelerate a transformation agenda that will create long-term value for individual companies, the entire industry and communities.

“Now companies have the opportunity to reflect upon changes and focus on retaining the capabilities that enable agility and preparedness for future events.”

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.