‘Dr Copper’ woes loom over mining minnows

Pic: Getty

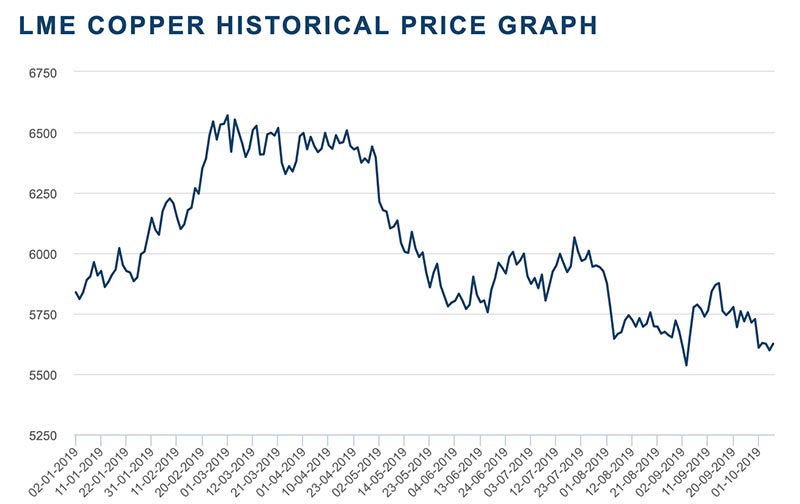

It’s not called “Doctor copper” for nothing as wariness over the outlook for global economic growth has prompted some analysts to downgrade their price forecasts for the key industrial metal.

So far this year, the copper price is down by well over 10 per cent in the wake of the never-ending trade war between China and the US.

As a result, Citibank recently cut its copper price forecast for 2020 by 5 per cent to $US6500 a tonne.

Citibank also slashed its 2021 and 2022 copper price forecasts by 12 per cent ($US6600/t) and 9 per cent ($US6800) respectively.

Analysts said that even though both the US and China are scheduled to continue talks in a bid to resolve the trade dispute, it remains cautious over a resolution.

Additionally, the price impact from China’s move to limit imports of copper scrap has been muted due to transitional arrangements. China is forcing importers to demonstrate they can process copper scrap to higher environmental standards or face cutbacks.

READ: Who made the gains? Here are September’s top 50 small cap miners and explorers

For smaller miners such as Metals X (ASX:MLX) and Aurelia Metals (ASX:AMI), the prospect of continued soft copper prices is unwelcome news as they face their own production issues which have pressured the share prices of both companies.

Aurelia Metals, which operates at Cobar in north western NSW, is navigating a changing production profile, with declining gold output hitting revenues that a rise in the output of copper was unable to offset.

This has seen its shares revisit near 18-month lows of around 40c.

Emerging copper production has helped to offset the impact of the decline in gold output on revenue and earnings for Aurelia, but the prospect of weaker than expected copper prices over the next few years may limit investor optimism until it is able to lift production of other base metals at its Cobar mine.

For its part, Metals X is now embroiled in a deepening stoush with shareholders over its problematic $74 million purchase of the Nifty copper mine.

When it bought the troubled mine from its Indian owners four years back, analysts were almost uniformly upbeat that Metals X would be able to whip the mine into shape.

But that optimism proved to be misplaced. After continued problems at the copper mine and following a highly dilutionary share placement last month (Metals X raised $33 million issuing shares at 15c), its largest investor, APAC Resources, has put forward a nominee for the Metals X board, which the miner is resisting.

Metals X’s chairman is also set to quit the company, which APAC supports.

And analysts are less than impressed with the company’s ongoing woes, although most who cover the company still have ‘buy’ calls out on its shares.

“Risks have risen sharply,” Hartley’s said in a recent note, with Bell Potter saying the latest equity raising sends “mixed messages”.

“While MLX’s equity raising sends mixed messages and is quite dilutive, having been done at a price of 15c a share,” Bell Potter wrote in an investor note, “we continue to watch for more tangible signs of a turnaround at Nifty and the growth in output at Renison [tin mine in Tasmania]”.

Canaccord points to two emerging “positive catalysts” for Metals X to give shareholders some solace: the prospect of resolution of the board fight, and the Nifty copper mine turning cash flow positive in early 2020.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.