Copper supply-demand outlook creates perfect storm for next generation of explorers to producers

Pic: Schroptschop / E+ via Getty Images

Major copper producers are losing market share as demand for the red metal gets set to explode thanks to the clean energy transition already underway. This opens up a big gap for emerging producers to step in and fill.

This was illustrated by Newmont’s $C456m ($477.7m) cash offer last month for GT Gold, a copper porphyry explorer in Canada. Juniors with new prospective projects in tier 1 jurisdictions appear set to be well rewarded.

Commodities research house Wood Mackenzie estimates that for the industry to counter the issue of grade declines and depletions, over the next decade it needs to inject an additional $US130bn ($170.7bn) to deliver an extra 6.5 million tonnes of copper supply each year.

And that’s just to meet Wood Mac’s “base case” scenario. If the energy transition was accelerated, copper producers would need to pump out an extra 9 million tonnes each year by 2030, requiring a massive $US325bn investment.

The latter scenario appears more likely and even conservative, according to international copper market commentator Gianni Kovacevic. “Copper is going through a once-in-a-hundred-year pivot with this global transition to electrification,” he said.

“The Green New Deal (in the US) and on top of that the restimulation of the global economy, which is now well in excess of $US10 trillion dollars — they all help copper.

“We need more copper in the next 20 years than was installed in the last 130 (years).”

Kovacevic’s view regarding the transition to electrification is backed up by the world’s largest miner, BHP (ASX:BHP), which estimates copper production will have to double over the next 30 years to satisfy these new demands.

Julian Kettle – senior vice president, vice chair metals and mining at Wood Mac – says this would stretch investor appetite and corporate financing capability, potentially to breaking point.

“Given lead times, investment needs to be mobilised in the next two to three years – and even this won’t prevent market shortages mid-decade, which are essentially ‘baked in’ due to insufficient elasticity of supply,” he said.

There is currently 17 million tonnes of future copper supply already in the pipeline, and while that is more than enough to meet projected demand, Kettle says many of these projects are in “risky jurisdictions” and not the “usual hunting grounds of the copper majors, who tend to prefer the richer pickings of low-risk jurisdictions and long-life, low-cost assets”.

By Wood Mac’s numbers, a major copper producer has to pump out at least 500 kilotonnes of copper each year.

Kettle said right now there were 13 entities that met that criteria and collectively they accounted for nearly 10 million tonnes per annum of copper production in 2020, giving them 47 per cent global market share.

“However, the major copper producers will collectively experience a net decline in output of 800 kilotonnes per annum by 2030, without further project development,” he explained.

“Set against an increase in market demand of around 6 million tonnes per annum, this means the majors’ collective market share will decline to just 34 per cent (assuming no further projects are sanctioned).

“The situation will become acute by 2040 when, without further investment, the ‘Big 13’ copper majors’ output will decline to 7 million tonnes per annum, or less than 25 per cent of global output.”

This provides the perfect platform for the smaller players already advancing projects in tier one jurisdictions like Australia and Canada to take advantage of the resulting opportunities.

Firstly, it creates the perfect storm for an increase in mergers and acquisitions activity as the majors look to replenish their project pipelines and grow resources inventory and production by acquiring prospective and advanced projects.

“Acquisition could offer an attractive opportunity to take a bigger bite out of the copper pie, attaching lower and known risks, and a guaranteed production stream,” Kettle explained.

“It could become a feeding frenzy.”

It also opens up the opportunities for joint ventures and provides a favourable environment for companies looking to take a project all the way to production and find demand for their copper if they choose to go it alone.

This trend is already starting to emerge in Canada’s leading copper porphyry belt, the Golden Triangle.

Newcrest Mining’s (ASX:NCM) deal to secure a 70 per cent interest in the Red Chris copper-gold porphyry mine is bearing fruit given its recent significant resource upgrade, and only last month Newmont, the world’s largest gold miner, also expanded its interest into the region with $C456m cash deal for GT Gold, an advanced porphyry explorer.

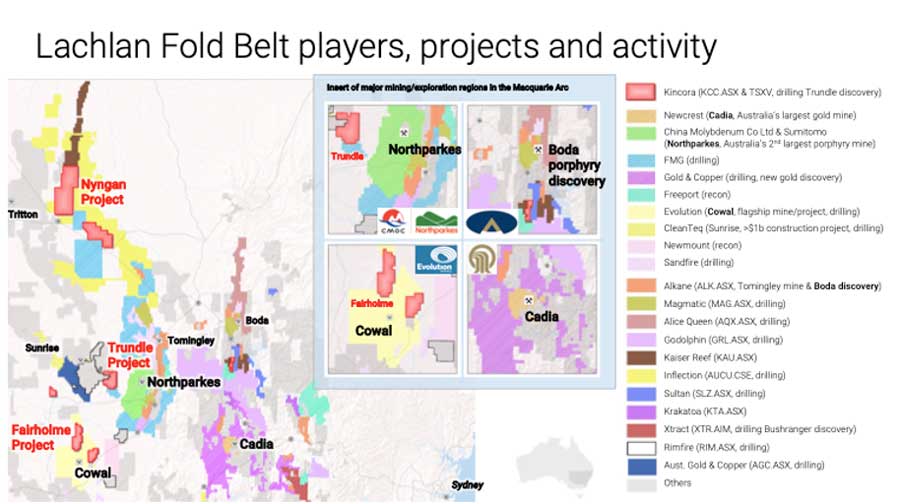

Kincora Copper (ASX:KCC), which just made its debut on the ASX making it a dual-listed company in Canada and Australia, is currently drilling the only brownfield project, Trundle, held by a listed junior in Australia’s foremost porphyry district — the Macquarie Arc in NSW, part of the Lachlan Fold Belt (LFB).

The LFB has become one of Australia’s hottest mining addresses thanks to Alkane Resources’ (ASX:ALK) Boda discovery in September 2019. The region is also host to Newcrest Mining’s (ASX:NCM) giant, low-cost and successfully producing Cadia copper-gold mine, Australia’s largest and most profitable gold mine, and Evolution Mining’s (ASX:EVN) flagship Cowal gold-base metals mine.

Interestingly, in a recent Cowal site visit presentation, Evolution talked up the regional opportunities available, saying the Macquarie Arc is a “world class geologic setting for gold and copper-gold deposits”.

Kincora controls a district scale 1,649sqkm, eight-licence project pipeline. Trundle shares the same mineralised system as the Northparkes mine, which is Australia’s second-largest porphyry mine and hosts 4.5 million tonnes of copper and 5.5 million oz of gold.

And you can see below just how close the company’s projects are to big operations, including Cowal and Northparkes, in the region.

Investor interest in Kincora has been immense.

After initially targeting $8m in its IPO, the company quickly upped this to $10m and received bids for many multiples of that from recognised local/international specialist resources funds, family offices and retail investors.

Kincora lit up the boards on March 30, trading as much as 30 per cent higher than its IPO price of 20c. The company is still up 17.5 per cent and has a market capitalisation of only $28m with over $12m in cash.

Kincora Copper (ASX:KCC) share price chart

“On the ASX there are about 10 to 20 gold juniors for every copper play, and even during the downturn many prospective copper plays were the focus of corporate activity,” Kincora CEO Sam Spring said.

“Given the favourable outlook for copper demand versus supply, the implications to pricing, with the industry’s project pipeline already being at record low levels, it is likely the trend already being seen in Canada for accelerating M&A will also increase in Australia for juniors with attractive projects.

“With an industry leading technical team, our existing targets, amount of drilling and balance sheet post our recent IPO on the ASX, we are looking to position Kincora as the leading pure play porphyry explorer in Australia’s foremost porphyry belt.”

Spring said Kincora was already drilling with two rigs, with very promising results and an initial skarn discovery at Trundle, which is in the same mineralised complex as Australia’s second largest porphyry mine at Northparkes.

“In the second half of the year, we will be drilling at our Fairholme project which is closer to the mill at Cowal than some of the targets Evolution is now talking up on its adjacent ground,” he explained.

“Given the location of these projects and their existing hallmarks to the neighbouring world-class mines, good results from the drill bit are expected to attract significant interest.”

The company plans to drill a minimum of over 17,000m across three projects in the LFB in the next 12 months as part of a much larger 34,000m drilling program.

This article was developed in collaboration with Kincora Copper, a Stockhead advertiser at the time of publishing.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.