Why the world’s metals traders are loving copper

Pic: Schroptschop / E+ via Getty Images

Barry FitzGerald writes his legendary Garimpeiro resources column weekly for Stockhead

The world’s metals traders have descended on London for LME Week, the annual bash put on by the London Metal Exchange.

Apart from the top nosh dinners and raucous cocktail parties, the traders get down to swapping notes on just where they think metal prices are headed in the year ahead.

Over the years it has proved to be a pretty reliable guide to what unfolds, as might be expected given metals traders are in the thick of things when it comes to watching metal flows and reading supply and demand signals.

For years now Australia’s own Macquarie has been savvy enough to corral more than 400 of the traders and other metals types in to a big enough room for its annual LME Week Base Metals Outlook Summit, and then pick their brains for their metals outlook.

The summit has come and gone and the results of the poll are in, with copper getting most of the love in the room.

Macquarie reported the metals expected to perform best in the next 12 months were the same as in 2017 — copper and nickel.

But copper was further out in front this year, capturing 45% of the votes, while nickel followed on 31%.

The loser was aluminium, with its share of the votes to be the best-performed dropping from last year’s 17% to only 5%.

The traders were also asked to pick a trading range for copper and the other metals.

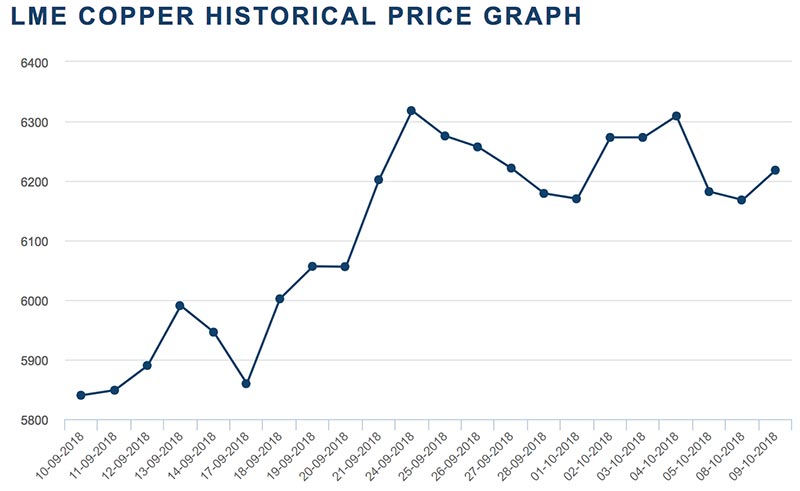

The most picked range for copper (55%) was $US6,550/t to $US7,300/t compared with the somewhat beaten up current price of $US6,174/t ($US2.80/lb):

Another 12% went the whole hog and tipped copper could surge to more than $US7,300/t ($US3.30/lb).

If that comes to pass, the copper producers will be a happy bunch. And given copper’s bellwether status on the global economy, things would have to be ticking along nicely generally.

Having said that, there are some special circumstances playing out in the copper market other than the ups and downs of global economic activity.

There isn’t a conference that goes by without someone pointing to the looming supply deficit at a time when the global fleet of mines is struggling to maintain full capacity because of falling grades and supply disruptions.

The same goes for the impact on the copper market (and a bunch of other metals) of the electric vehicle revolution.

EVs are copper intensive — using as much as four times the red metal as the typical internal combustion vehicle.

ASX copper stocks

Investors wanting to back home the metals traders’ call on higher prices (the 55% plonking for prices to rise by 7-18%) are spoilt for choice on the ASX.

BHP and Rio are among the world’s biggest producers of the metal — but their other mining assets mean their leverage to a stronger copper price is not as great as for the next tier down – Oz Minerals and Sandfire.

Greater leverage still is found further down among the junior producers like Aeris (ASX:AIS), mentioned here earlier in the week on the strength of its turnaround at its NSW copper mine and its exposure to the exciting Torrens copper/gold exploration program in South Australia.

WA copper (and tin) producer Metals X (ASX:MLX) has been gaining some support at its lower levels on the basis that it can improve the performance of its Nifty mine.

Among the developers, Venturex (ASX:VXR) has caught the eye after this week’s definitive feasibility study confirmed its Sulphur Springs project in WA was a robust development candidate.

The list of explorers is too long for this space but Aeon (ASX:AML), Minotaur (ASX:MEP) and Xanadu (ASX:XAM) have their fans.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.