Bald Hill: The battle to buy back a WA lithium producer literally undermined by Chinese machinations

Picture: Getty Images

- MinRes lobs a bid for the Bald Hill lithium mine in WA, Glencore also rumoured to be working on a $1.8bn proposal

- Bald Hill resource last updated 2018 to 26.5Mt at 1.0% Li2O

- Could new owner look outside boundary to boost resources?

- Surrounding ASX listed explorers include Torque, Boadicea

“Western Australian lithium is the most sought after product in the world,” said Mineral Resources (ASX:MIN) boss Chris Ellison, following the major’s decision to dump a $1 billion Chinese lithium processing JV and double down on its hometown advantage.

“I think the OEMs are looking to get product direct out of Australia if they can. They’re certainly giving us the signals they’re willing to pay a premium for that,” he said.

No surprise then that growth-focused MIN has lobbed a bid for the Bald Hill lithium mine in WA, days after Glencore was rumoured to be working on a $1.8bn proposal of its own.

MIN won’t disclose how much the mine could cost, but expects to fund the potential transaction from existing resources “and does not intend to raise equity”.

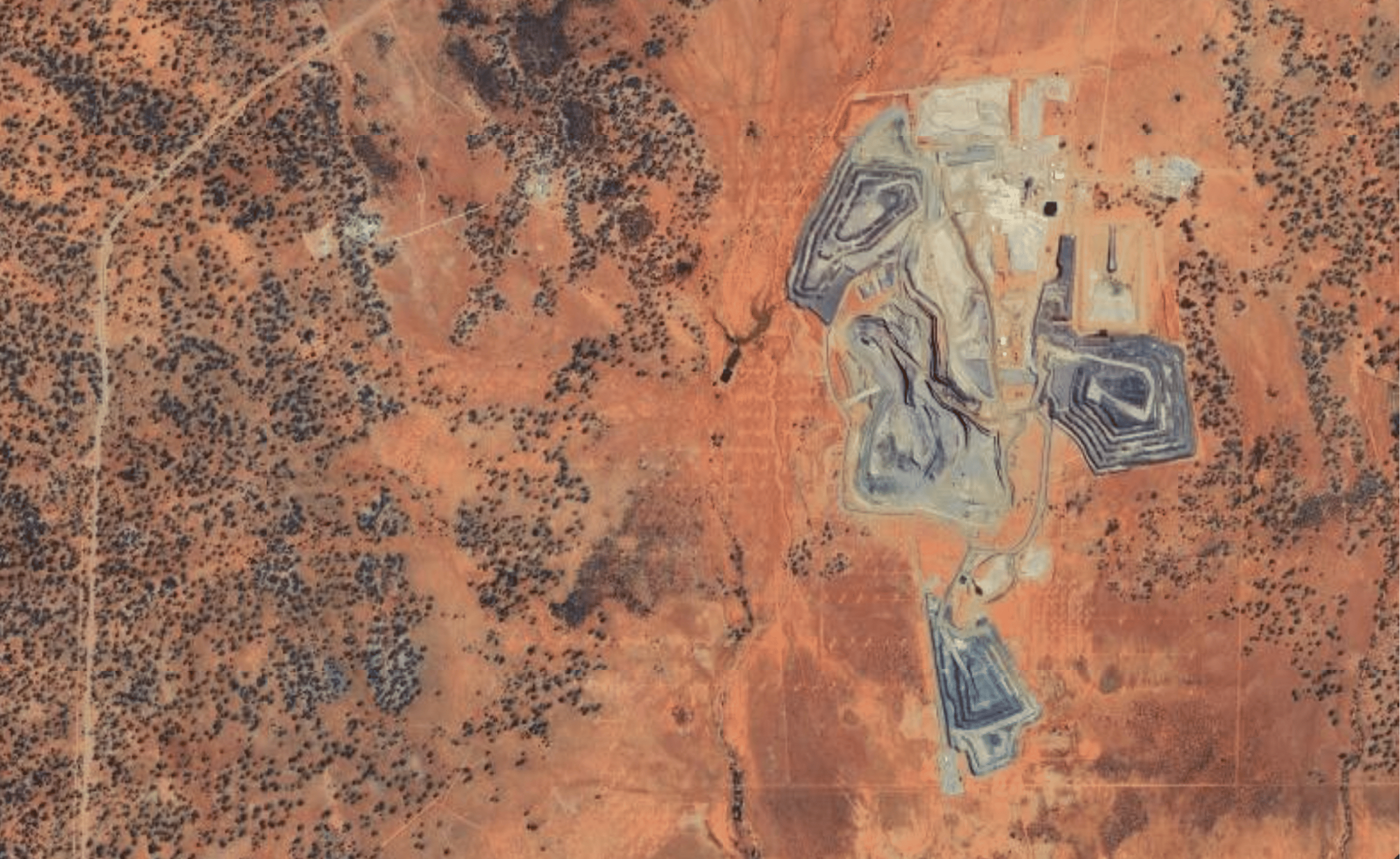

The revival of Bald Hill, one of Australia’s only producing lithium mines

Heavily indebted Bald Hill owner Alita went into administration in 2019 as one of the first high profile casualties of plummeting spodumene prices.

It was delisted from the ASX, but a China-connected company bought the debt and has been selling spodumene from Bald Hill – allegedly on the cheap – to Chinese buyers since mining recommenced in February 2022.

“It has been reported that the Bald Hill lithium mine operates under effective foreign control through a complex corporate structure,” MIN says.

“It is reported that the lithium mine operates at a loss under these arrangements, with profits transferred overseas via an offtake agreement with a Hong Kong-registered entity, Yihe Cleantech Material Limited.

“It has been alleged that this offtake agreement has also led to an under-payment of state royalties.”

Efforts by this company, Austroid, to acquire Alita outright were blocked by Federal Treasurer Jim Chalmers in July, on advice from the Foreign Investment Review Board.

Last week, the administrators of Alita Resources, McGrathNicol, started the liquidation process and entered a deal to sell the project to MIN.

What could it mean for junior explorers around Bald Hill?

Up-to-date info on the size of the prize at Bald Hill is sketchy at best, with the last known resource update to 26.5Mt at 1.0% Li2O (using 0.3% Li2O cut off) and 149ppm Ta2O5 occurring in 2018.

That’s not particularly big, as far as spodumene resources go.

We do know that before it went into administration Alita defined an exploration target immediately west of the pit (Pegmatite 3 West) of 17-24Mt at 1.25%-1.4% Li2O between 140-220m below surface.

According to Chinese mining contractor Liatam Mining – which also tried to buy the Alita assets in 2020 but was unable to get FIRB approval – exploration resumed after mining restarted in February 2022.

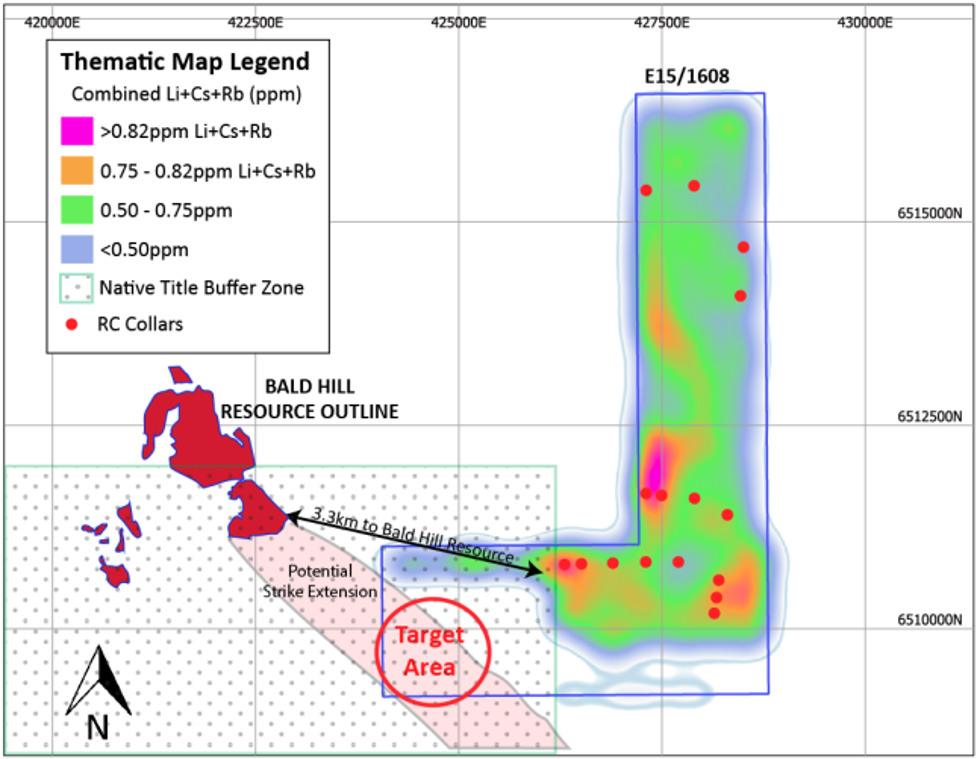

Still, with resources at tier one WA operations like Pilgangoora, Wodgina, Greenbushes and Mt Marion sitting on many multiples of that, the buyer could also look for tonnes outside its own 770sqkm tenement boundary.

Much of the remaining ground surrounding Bald Hill is held by the aforementioned Liatam and related companies like Bloomier Resources.

The rest is a collection of private enterprise and at least two ASX listed explorers – Torque and Boadicea.

Yesterday, Torque Metals (ASX:TOR) inked a deal to acquire a collection of gold, nickel and lithium-rich tenements — to be renamed Penzance — near its Paris gold camp in the Tier-1 Goldfields mining jurisdiction.

This includes New Dawn, an unmined lithium and tantalum occurrence on granted mining leases, 600m along strike of the established Bald Hill operation.

So close. Here’s another view:

The explorer is now mobilising for a 20-hole diamond drilling campaign this month to test some targets.

TOR managing director Cristian Moreno tells Stockhead the timing of the acquistion was incredibly fortuitous.

“I was dealing with the private vendor for two years prior to the deal being stuck,” he says.

“There are other companies interested in nearby tenements, but it’s so hard to get additional ground over here.”

Moreno wouldn’t be drawn on whether the new Bald Hill owner may look for extra lithium tonnes over the fence, but he did say “there are plenty of tracks and plenty of people working over there”.

And, like Ellison, Moreno is sold on WA.

“We don’t want projects in Canada. We don’t want projects in South America, or Europe,” he says.

“We believe the potential of Western Australia and Australia is huge.

“Why do we need to go to another country when Australia is the best destination for mineral exploration?”

On the other side is Boadicea Resources (ASX:BOA), which acquired the 17.6sqkm Bald Hill East tenement in December 2021 for just $300k.

Maiden drilling in September the following year failed to hit paydirt but the best part of the tenement – which “is closer to [and along strike from] the existing Bald Hill deposit and mine and considered more prospective” — still requires heritage clearance.

“Boadicea will continue to work with our native title partners to arrange land access at the earliest opportunity,” the company said late July.

We texted managing director Jon Reynolds for an update, but he is currently in the field “with very little comms”.

“I will call in a couple of days when I get back,” he says, so stay tuned for that.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.