Bad vibes good for gold as banks scramble to keep up with the flying metal

I'm picking up bad vibrations, gold's giving me excitations. Pic: Getty Images

- RBC says “bad vibes” around the performance of the global economy is powering gold higher

- Canadian investment bank now sees gold averaging US$3039/oz in 2025 and US$3195/oz in 2026

- Gold continues to push higher, hitting US$3125/oz last week

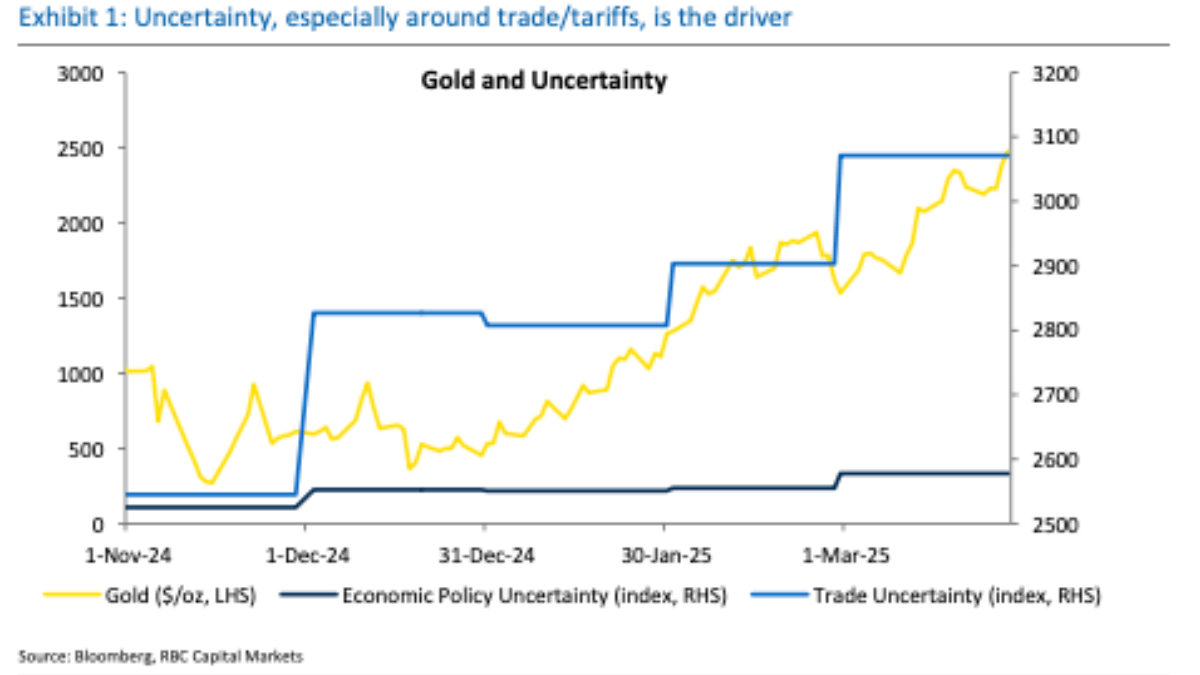

“Bad vibes” around the global economy has seen banks previously sceptical of the gold boom chase its price higher, lifting forecasts to levels that could only have occupied a miner’s dreams just months ago.

Gold has already crashed through US$3000/oz and lifted to as high as US$3125/oz.

That’s nearing on $5000/oz in Australian dollar terms, making the sector, unloved as inflationary pressures crushed margins a couple years ago, the beau, belle and everything else of the commodities ball right now.

RBC Capital Markets is the latest bank to raise its targets, setting its base case average for gold to US$3039/oz in 2025 and US$3195/oz in 2026 on “bad vibes and uncertainty”.

“While we are still not ruling out the possibility of a correction from uncertainty driven highs (towards our new low scenario of $2821/oz in 2025), it’s clear that economic sentiment has deteriorated and gold’s appeal is more durable in this environment, meaning elevated prices should hold,” RBC analysts led by Christopher Louney said.

“Yet, we think a further leg higher relies on soft data weakness turning into hard data weakness. This would drive a more aggressive investor-led push higher in prices towards our high scenario with more money flowing into the metal on an underlying basis than in our baseline.”

Could gold go all the way to US$3500/oz and beyond? RBC cautioned that uncertainty remains the key factor pushing gold to all time highs.

“… uncertainty is inherently uncertain – therefore necessitating soft data weakness turning harder to really achieve some of the loftier targets out there (our high scenario has $3263/oz in 2025, peaking at $3496/oz before year-end),” Louney and Co. said.

Further details from note

Central banks, especially in the East, have driven gold demand to record highs in recent years.

But it’s the recovery in demand from previously sidelined western investors late last year that has brought the push to record highs into view.

ETF inflows have risen as fears the breakout seen in US stocks last year will falter have emerged, with the tariff-forward economic policies of Republican President Donald Trump sending jitters through markets, now concerned the Yanks are heading for recession.

While gold typically enjoys an inverse relationship to the US dollar and treasury yields, it’s equity markets that gold has become the Newtonian equal and opposite reaction that gold has leveraged off.

A break in the S&P 500 below 5500 could trigger a ‘growth scare drawdown’, that could put the high price scenario for gold in play, Louney’s crew said (emphasis added by us).

“Beyond that, any visits to Tier 3 or 4 of her ‘Tiers of Fear’ (a reference to a note from RBC US equity strategy head Lori Calvasina) would likely see gold surpass our high scenario. For what it’s worth, in the most optimistic of her models where political tailwinds improve for stocks this year, we could see gold lose ground and reach out low scenario,” they wrote.

“Given the attitude among gold market participants, and the uncertainty, sentiment, economic, and market attitude driven nature of gold’s price moves of late, we view this equity market framework as an important guidepost for gold.

“Especially as we see investors continuing to warm up to gold and consider allocations to offset risks elsewhere in their portfolios, the direction of equity markets matters now, perhaps more than usual.”

On a macro level, RBC sees gold as “overvalued” in reference to long-term indicators. “In totality, our larger model requires significant uncertainty to get to current levels. While the floor has firmed for gold, it’s been for other reasons in our view.”

But worse hard economic data from the States could trigger an even more bullish push into ETFs from Western investors.

“We will likely see inflows into gold ETFs as investors grow allocations due to uncertainty, but to trigger a leg higher in interest and prices, soft data weakness needs to turn to hard data weakness, driving ETP AUM beyond the 2022 high and to the 2020 high and our high scenario prices.”

Soft data includes indicators like consumer confidence surveys, while hard data refers to quantitative measures like inflation, GDP and unemployment prints.

Where are other brokers placed on bullion

How bullish has consensus gotten on gold and are we likely to go higher?

Perth broker Argonaut has ratcheted up its gold forecasts by 20-50% for the next five years, with analysts Hayden Bairstow and Patrick Streater saying they see a pathway to US$4000/oz by 2027.

“The global backdrop has shifted to a perfect storm for the yellow metal, with record US debt levels, geopolitical uncertainty and concerns over the direction and pace of interest rates pushing spot prices beyond US$3,000/oz,” they told clients.

“EFT inflows have now joined the party and we see a pathway for gold to continue to climb to US$4,000/oz by 2027.

Also among the most ambitious gold forecasters is Victor Smorgon Group’s gold fund portfolio manager Cameron Judd, who suggested a few weeks ago that US$3600/oz was on the cards.

That’s not looking so outlandish now, and a number of big banks and brokers have joined him.

Macquarie thinks gold will crack an inflation adjusted high of US$3500/oz by the third quarter of this year, a measure that has stood since January 1980.

Goldman Sachs sees gold hitting US$3300/oz by the end of this year. The bank lifted its central bank purchase expectations from 50t per month to 70t per month this year and thinks bullion could go as high as US$3680/oz if ETF investors really jump on the bandwagon.

A 10% lift in investment demand would take gold to US$3500/oz within two years, Bank of America thinks, while Citi has a near-term base case of US$3200/oz and US$3500/oz is on the cards as the year progresses.

Smaller brokers without their own in house economics teams often use consensus forecasts as a stand in, which are predictably rising in the current environment.

Consensus Economics, which amalgamates upgrades from 29 banks and financial monitors, last estimated the consensus forecast for 2025 at US$2851/oz in mid-March. Recent updates will push that higher.

Consensus forecasts have the price tracking down to US$2554/oz by 2029, with a long-term real price estimate of US$2312/oz (adjusted for inflation) and nominal of US$2880/oz.

While forecasts may be speculative they can move markets because they change valuations for miners, resulting in a feedback loop as funds adjust their holdings based on their respective models.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.