Year of the Carrot and Stick: 2024 brings more risk and more optimism, says Morningstar

Via Getty

The 2024 fiscal forecast according to Morningstar looks something like this:

Heaps of risk, very high stakes – but with a decent smattering of ‘cautious optimism’ for stocks, bonds …and that the world probably won’t end.

This year’s annual take on what happens next year has Morningstar’s best offering both a comprehensive and also a slightly upbeat assessment of the global economic outlook and the impact that’ll have on its various markets for 2024.

It could be game on, they say – but with one important caveat:

Yes, there are stars aligning for the morning of 2024, but the dangers are more widespread and the stakes just keep getting higher.

I mean, how’s this for a come-thither-but-stay-back of an intro:

As we stand at the threshold of 2024, it’s essential we remind investors that the presence of uncertainty does not imply a scarcity of opportunities.

Our approach to the year will be a blend of caution and optimism.

For those in Australia, and Asia Pacific more generally, the investment arena may appear daunting given recent market volatility.

Yet we see investment opportunities emerging.

Periods of market volatility and pessimism should not be seen as a barrier to investment but rather are a normal part of the journey to reach financial goals.

With an eye on a beleaguered global macroeconomic backdrop, the Morningstar report put forward its ‘base case’ for investing in the new year.

“We are cautiously optimistic for both stocks and bonds as we enter 2024, even accounting for heightened risk,” Morningstar CIO Asia-Pacific Matt Wacher told Stockhead.

There’s those universally higher interest rates and the emerging influence of increasingly tougher debt servicing commitments. And there’s the rising pressure that’s placing on indebted households.

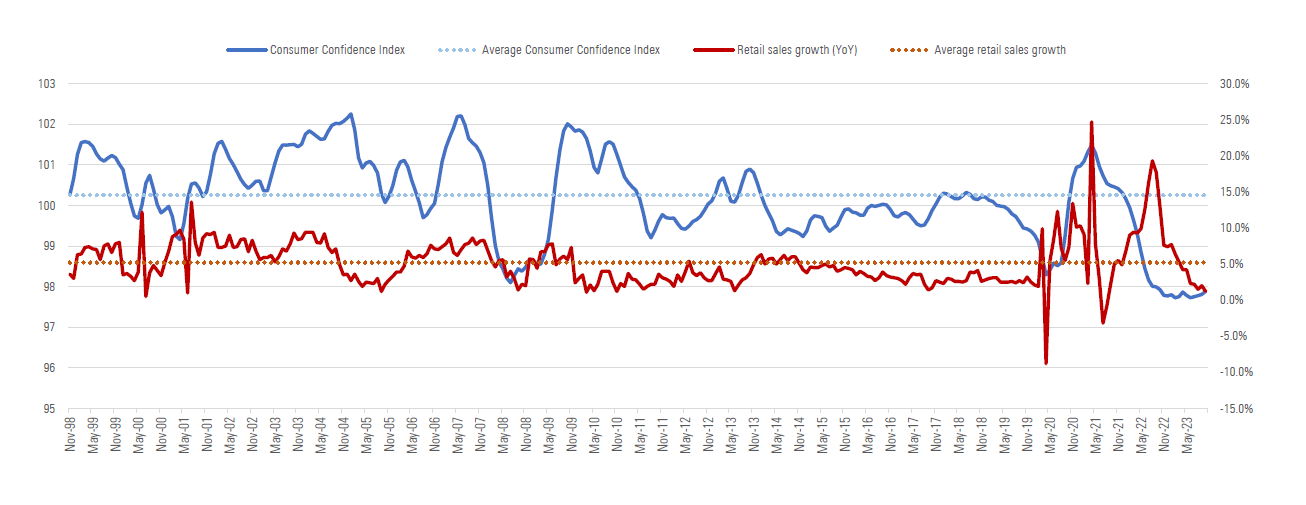

“High savings buffers and low unemployment have supported growth, but the consumer is showing signs of fatigue as revealed by falling retail sales and consumer confidence,” says Matt.

“While the risk to a recession is alive, it is not our base case.

“The Australian economy will continue to flatline, with falls in GDP per capita occurring over the first half of 2023 despite relatively low unemployment levels,” Matt says.

“We also think it is plausible for many central banks to cut rates from mid-2024 and into 2025 although these central banks will continue to walk a tight rope between reducing inflation and strangling a struggling economy.”

Morningstar’s Macroeconomic Outlook for 2024

ミ✰ We expect further economic change in 2024.

That’s to say the global economy remains fragile. Against this backdrop, the analysts reckon ‘it is plausible’ for many central banks to cut rates from mid-2024 and into 2025.

ミ✰ Questions around potential recession risks and the inflation outlook will likely persist as some economists still see a high chance of a recession in the next year.

Morningstar says that developed world central banks, including the RBA, are walking a tight-rope between reducing inflation and strangling a struggling economy. They warn that there’s a wide range of potential outcomes around the ‘base case.’

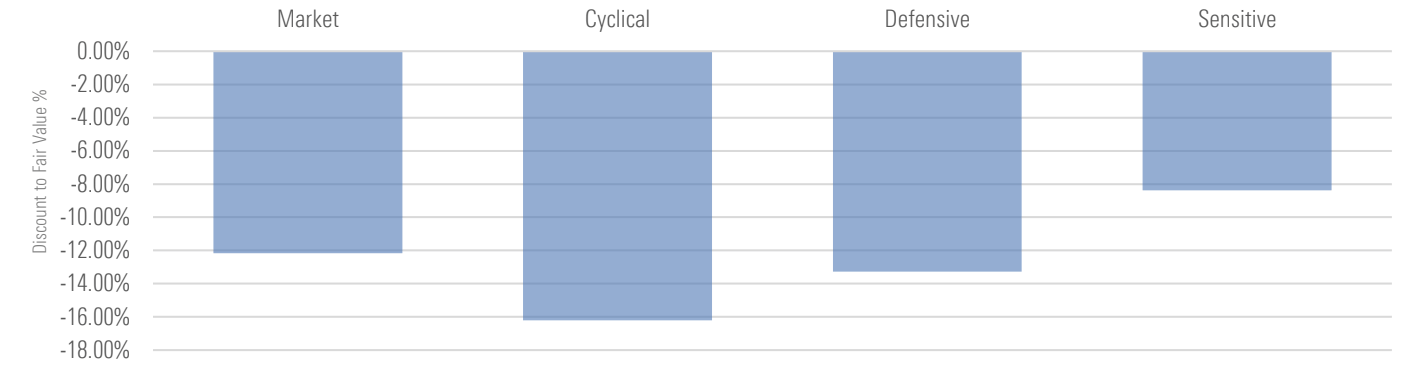

ミ✰ Among equities, valuations present us with opportunities.

Morningstar’s Matt Wacher says that by ‘looking for undervalued areas of the market’ investors can ‘add robustness’, with defensive stocks of particular interest.

ミ✰ Certain scenarios pose a challenge to any ‘base case’ assessment.

Right now, known risks include geopolitics and the impact that has on the oil price, for example.

ミ✰ The Australian economy continues to flatline, with falls in GDP per capita occurring over the first half of 2023 despite relatively low unemployment levels.

As higher interest rates have increased debt servicing commitments, the disposable income of indebted households is under pressure. The savings buffer from massive fiscal stimulus programs in 2020 and 2021 has depleted and household consumption is being curtailed.

Known Unknowns

“However,” Matt adds, “our scenario analysis sheds light on various potential outcomes that are currently unknown too, offering a perspective on non-normal scenarios that can greatly influence investment decision- making.

“Defensive equities and a mix of bond holdings feature as core assets to manage these risks.”

Based on Morningstar’s ‘scenario testing,’ the key portfolio positions that can ‘help facilitate robustness’ include:

Defensive equities, including healthcare and utilities,

Inflation-linked bonds,

Diversified currency exposure outside the US dollar.

Current Valuations Slightly Favour Cyclical Assets, Defensives Aren’t Far Behind (Discount to Fair Value):

But hang on, here are three ‘swing factors’ that could upend Morningstar’s base case:

1. Geopolitics

Matt says with the return of military conflict in eastern Europe and the Middle East, geopolitics has become ‘a greater swing factor’ than in recent years.

“We’ve also seen more abrasive relations between China and the U.S. and scope for elections to result in large policy shifts.

“As investors anticipate change and adapt to new risks, these conflicts have already impacted prices, with potential knock-on effects on commodity prices including critical energy supplies. We must also weigh the economic effects of an ongoing rise in military spending in Europe, Asia and the US.”

2. Climate

“Natural events impacting our physical environment and health have the potential to impact growth and inflation depending on severity and government responses.

“Extremes in weather impacted energy demand in 2021 with shortfalls in solar and wind in North Asia causing higher demand and prices for gas while pandemics had tragic impacts and ongoing constraints on supply that especially impacted the economy in China from 2020 to 2022.”

3. Technology

Morningstar’s third swing factor is the take up of technological innovation.

“Only when the breakthrough discoveries of the past like the printing press, steam engines, electricity and computing were applied at scale did they enhance productivity, increase growth and ease inflationary pressures.

“The faster artificial intelligence is applied, the faster the effects will be felt and we are at the point now where application is expected to ramp up,” according to Matt.

So, cover ALL your bases

According to Matt, taken together, in periods of change like today, investors need to prepare themselves for a wider-than-usual range of potential economic scenarios.

“This means looking at a well-diversified portfolio that goes beyond a focus on equities.”

To ensure a robust portfolio, Matt likes defensive equities, including healthcare and utilities; inflation-linked bonds; and diversified currency exposure outside the US dollar.

AI/Tech stocks: Just mind the valuations

The report highlighted opportunities in artificial intelligence, but investors need to be wary of frothy valuations.

“Artificial intelligence is an exciting theme, and we expect a lot of market interest in 2024,” Matt said.

“However, while some of these companies are great businesses, valuations at the moment appear lofty. Based on its current valuations a business like Nvidia will need to buy another Nvidia if it is fulfill its current share price.

“The risk/reward equation is not in favour of the investor despite it being a fantastic company.”

Morningstar notes that one effective way to access the AI theme without paying huge valuation premiums is via second-derivative plays. These are not the chip makers or those that offer technology interfaces, but rather, those who can effectively embed AI into their workflow and drive new revenue growth opportunities.

These ‘second derivative plays’ are business such as IT consulting companies, data management providers and data centres.

“We see opportunities in businesses like Taiwan Semiconductor or Samsung that could support stocks like Nvidia,” Matt Wacher says.

“Even bigger IT consultants like IBM or Fujitsu are well placed for the future.”

Carrots and Stocks:

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.