Traders’ Diary: What will happen now that The Fed’s rate cycle has hit terminal velocity?

Via Getty

THE WEEK THAT WAS

Australian equity markets ended last week on another unfamiliar high note, the ASX200 closing up +3.4% from Monday’s intra-day low.

In short, that’s because this is what happened on Wall Street last week:

-

Dow Jones +5.1% to 34,061

-

S&P 500 +5.9% to 4,358

-

The Nasdaq Composite +6.6% to 13,478

-

The Russell 2000 +7.6% to 1,761

-

The CBOE Volatility Index (VIX) down -29.9% to 14.91

From Wednesday morning to Friday arvo, the Aussie benchmark went on a 200-point rampage led by some furious buying across the market’s forlorn, rate-sensitive corners.

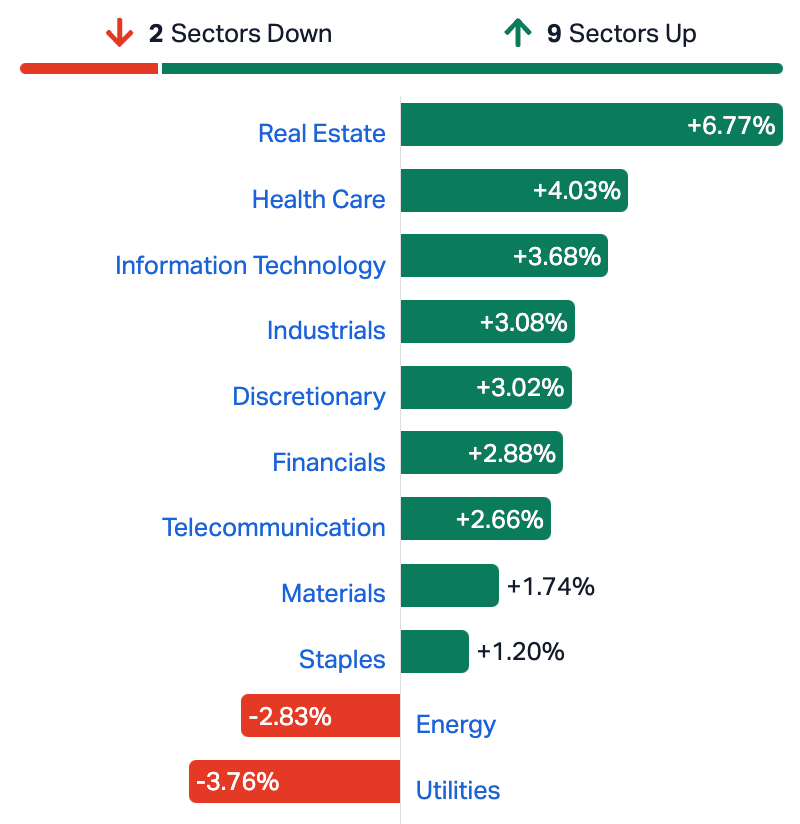

Real Estate stocks (+6.7%) went nuts leading the charge during a stellar surge in the back half of last week, with only the Utilities and Energy Sectors missing out.

On Sunday night in Sydenham, the SPI Futures are calling the ASX200 to open up +0.2% on Monday morning following the strong Friday night session on Wall Street, although some notable losses for BHP in US trade might take the shine off some of those gains.

ASX SECTORS LAST WEEK

Stocks were up for a fourth straight session on Friday, a pretty breathless turnaround from the last few months or maudlin trade – a run which began the very moment US Chair J Powell hinted that the Federal Reserve may’ve fired its last shot in its historic and bloody battle vs inflation at 5am on Wednesday according to the Sydenham clock.

To the intense relief of equity traders, 10-year US Treasury yields have jumped back almost 30 basis points from mid-week highs – back down to around 4.65% – and are close to their biggest weekly drop since March.

On Wall Street, the markets’ Gauge of Fear – the VIX – made a five-day long plunge of the kind not seen in almost 24 months. The unbreakable US dollar retreated the most since July and even the price of oil tumbled to $US81.

All encouraging signals of a still strong market backed by a still strong economy and enough to make everyone outside of the Middle East and Ukraine forget about the world’s litany of challenges

Wall Street extended the week’s advance on Friday night, with the S&P500 closing up +0.9%, notching its best week in 2023, again illustrating how bond yields drive stocks.

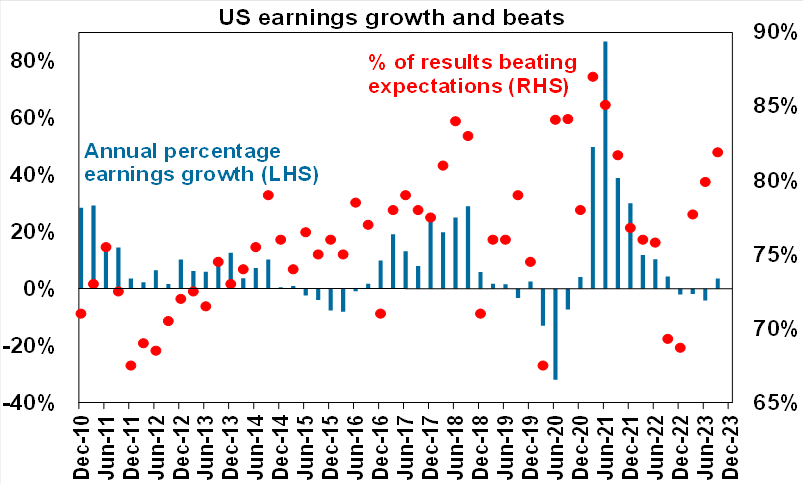

US earnings beats are at the best they’ve been in two years.

AMP says 81% of US S&P 500 companies have now reported September quarter earnings with 81.9% beating expectations, well above the norm of 76% and the strongest in two years.

Earnings growth for the quarter has improved to +3.6%yoy from +0.6% at the start of the reporting season.

Even the very hot US labour market cooled off some according to Friday’s non-farm jobs data.

That in turn assisted the down/up shift in US bonds and equities.

Markets all over the place didn’t muck around – Asian markets led the way in embracing the very notion that perhaps The Fed is done with rate hikes.

In offshore economic news it was a week for the central banks – dominated primarily by the BoJ and the FOMC and a nod to the BoE which also kept rates on hold as widely expected.

In Tokyo, the BoJ held its policy rate unchanged at ‑0.1% and the 10-year Japanese government bond (JGB) yield target was also unchanged at 0%, but the board did nix the hard upper limit around their 10-year JGB target, instead referring to the upper limit as a ‘reference’.

CBA says markets broadly took the policy change as a keeper.

“The FOMC left the Fed funds rate on hold at 5.25‑5.50%. Markets assign a low probability that the Fed will raise rates again and our International Economics team agree that the current rate will be terminal for this cycle.”

HOME ECONOMICS

It was a busy week for local economic news.

CoreLogic reported on the recovery in Australian home prices which CBA says ‘remains firmly in place’ with home values up by 0.9%/mth across the eight capital cities in October.

Sometime in the next few weeks we’ll be back at record highs, CoreLogic’s Tim Lawless reckons, and they did so in the face of some 400 basis points of interest rate hikes delivered by the RBA.

Price gains were most robust in Perth (+1.6%), Brisbane (+1.4%) and Adelaide (1.3%).

Supply and demand dynamics have overwhelmed the impact of higher borrowing costs with strong population growth and low listing stock supporting prices. Building approvals fell by 4.6%/mth in September. The level remains near decade lows and is even weaker on a per‑capita basis.

New housing lending rose by 0.6%/mth, led higher by strength in investor lending.

Warm weather and government policies provided a tailwind for domestic spending with retail trade data showing a decent 0.9% month on month gain in September.

Last week we also got a look at the real (inflation‑adjusted) retail trade figures. The volume of retail spending increased by 0.2%/qtr in the September quarter, CBA says.

“This represents the first gain since Q3 2022. Annual growth remains very weak, down by 1.7%, and down by 4.0% once population growth is taken into account. Lower price growth, good weather and special events including the FIFA Women’s World Cup boosted Q3 spend.”

The Aussie trade balance has narrowed further to $6.8bn, driven by a jump in industrial transport equipment imports.

Rates Day on Race Day

This week, the economic data flow in Australia will get mugged by local monetary policy with the RBA Board meeting on Tuesday.

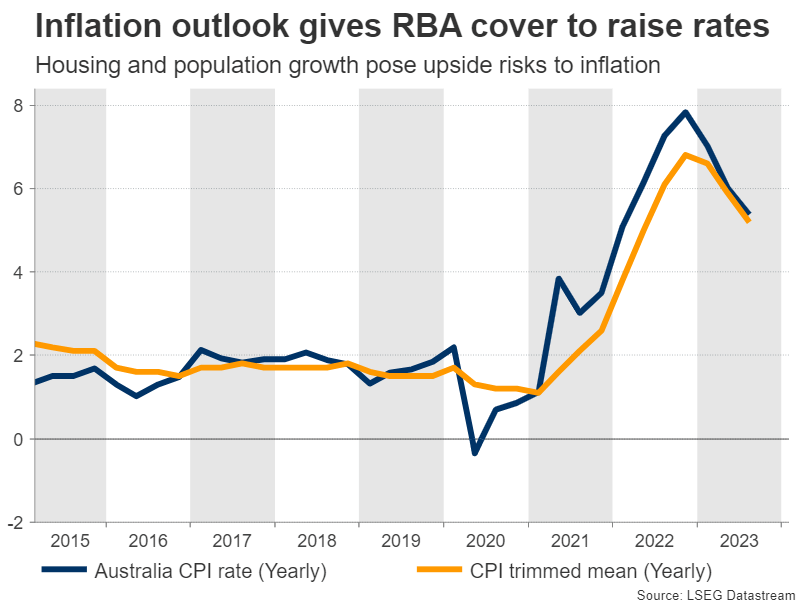

“We expect the RBA will be forced to act on its hiking bias that it has retained since the last hike in June and which has sharpened in recent communication. An upside surprise to both headline and trimmed mean inflation last week was the catalyst for us to change our base case to include a hike in November and push back our forecast for cuts out to Q3 24.

Even the IMF last week warned the RBA it needs to raise rates further to cool an Aussie economy running beyond full capacity. A historically tight labor market and booming population growth is adding weight to the argument that local inflation might pose a problem for a bit longer yet.

Certainly, Gareth Aird, head of Australian Economics at CBA, says it’ll be a rate rise.

“The stronger than anticipated inflation figures as well as continued tightness in the labour market and solid retail spending in September leaves us with high conviction (we ascribe an 80% chance) of a hike next week. The RBA will release the quarterly Statement on Monetary Policy on Friday which will include fresh economic forecasts.”

The Australian Economic Calendar

Monday November 6 – Friday November 10

Source: Commsec, Trading Economics, S&P Global Research, AMP

MONDAY

Nope

TUESDAY

RBA Interest Rate Decision

WEDNESDAY

Australia Building Permits (Sep, final)

THURSDAY

Nope

FRIDAY

Australia RBA Statement on Monetary Policy

The Everyone Else Economic Calendar

Monday November 6 – Friday November 10

Across the Pacific, China will focus on inflation rates, new yuan loans, and foreign trade data.

The UK, the Philippines, and Indonesia will release their Q3 GDP growth rates.

Spain, Italy, Brazil, and Canada will share service PMIs, and Germany will provide updates on factory orders and industrial production.

MONDAY

Worldwide Services, Composite PMIs, inc. global PMI (3-6 Oct)

Japan BOJ Meeting Minutes

Indonesia GDP (Q3)

Thailand Inflation (Oct)

TUESDAY

Japan Household Spending (Sep)

Philippines Inflation (Oct)

China (Mainland) Trade (Oct)

Malaysia Industrial Production (Sep)

Taiwan Inflation and Trade (Oct)

Germany Industrial Production (Sep)

United Kingdom Halifax House Price Index* (Oct)

Eurozone Construction PMI* (Oct)

Eurozone PPI (Sep)

Canada Trade (Sep)

United States Trade (Sep)

S&P Global Sector PMI (Oct)

WEDNESDAY

Germany Inflation (Oct, final)

France Trade (Sep)

Taiwan Trade (Oct)

Eurozone Retail Sales (Sep)

Canada BOC Summary of Delibrations

United States Wholesale Inventories (Sep)

S&P Global Metal Users and Electronics PMI* (Oct)

THURSDAY

South Korea, Taiwan Market Holiday

Japan BOJ Summary of Opinions (Oct 30-31)

Japan Current Account (Sep)

Philippines Industrial Production (Sep)

China (Mainland) CPI, PPI (Oct)

Philippines GDP (Q3)

United States Jobless Claims

FRIDAY

Taiwan Market Holiday

Malaysia GDP (Q3)

Norway Inflation (Oct)

Turkey Industrial Production (Sep)

United Kingdom monthly GDP, incl. Manufacturing, Services and Construction Output (Sep)

United Kingdom GDP (Q3, prelim)

United Kingdom Goods Trade (Sep)

Hong Kong SAR GDP (Q3, final)

Brazil Inflation (Oct)

India Industrial Production (Sep)

United States UoM Sentiment (Nov, prelim)

US EARNINGS THIS WEEK

The earnings season will continue, featuring reports from companies such as Berkshire Hathaway, Gilead Sciences, Uber, and Walt Disney.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.