Traders’ Diary: Everything you need to know for the week ahead

Via Getty

What went down last week

Emotionally and morally global markets were mixed over the previous week of business. Like a kebab in Coogee, there was a lot going in and no-one could be certain how it would come out.

American and Japanese shares produced some solid returns, but Euro and Chinese diners went down – investors still digesting the relative feasting of the week before, rich with the central bank sauce of upwardly revised interest rate expectations.

The ASX at home was little changed neither helped by plucky jobs growth which added weight to rate hike expectations.

Losses for Materials and Telcos offset more gains for Financials and the Healthcare sector.

Oil prices found a little form. Metals prices did not, led by a disappointed posse of iron ore punters.

A less belligerent Greenback did lift last week, and the always unpalatable McAussie slid.

BTFW. The Euro looks to be moving away from 17-month highs just in time for me to leave.

AMP’s Dr Shane Oliver says globally and at home, shares remain at risk of a short-term correction given high recession risks.

He adds that worries about Chinese growth, the ever-present risk of more rate hikes (RBA inclusive), remaining wary and the seasonally rougher patch often seen through August to October.

“But the ongoing fall in global inflation with the promise of a peak in interest rates is consistent with our positive 12-month view on shares and appears to be dominating for now. So, any pull back may be shallow.”

After the dip in US inflation down to 3%yoy, Wall Street traders slaughtered the obligatory virgin, sifted through the entrails and there was much celebration. Not least because Canadian inflation fell to 2.8%yoy in June (from 3.4%) with the average of its underlying measures falling to 3.8%yoy (from 3.9%).

We all know Canada secretly rules the world at the head of some kind of five-eyed global cabal of like-minded sneakypants.

In New Zealand, inflation fell to 6%yoy in the June quarter from 6.7%, with core (excluding energy & food) inflation falling to 6.1%yoy from 6.5%. The Kiwis are just terrible with numbers and houses.

Meanwhile, the least useful five-eyed nation, Britain, spent the week cheating at cricket. Surely their position in the 5 is under extreme doubt now. Tahiti, North Korea, or perhaps Luxembourg are certainly among the names Canadian selectors must now be seriously considering as a potential fifth.

UK inflation also crashed to 7.9%yoy from 8.7% with core inflation falling to 6.9% from 7.1%. Just awful numbers.

Meanwhile on Wall Street, the atmosphere by Friday was rich with cocaine and virgin entrails with all this data adding to evidence that global inflationary pressures are in retreat.

ASX200 WEEKLY SECTOR RETURNS

Local shares tracked US markets lower on Friday, but the trigger-happy six-shooters are still out there searching for targets.

There’s bulls aplenty out there with a taste for fresh fields of equities.

ASX200 WEEKLY INDIVIDUAL RETURNS

On the Tech Sector watch, however, some whacking with the greedy stick was seen in US reporting on Thursday night, on Wall Street and some higher bond yields kept the rockets on the launch pad for a day.

At home the Big Four banks and their financial friends put the recent outperformance on pause Friday, pocketing recent gains and despite some weakness late in the week, Financials remained the benchmark’s best on field this week.

The ASX200 even fought back late in the day, clawing back a hefty deficit to end the week with a +0.15% gain after hitting three-month highs on Thursday.

US stock markets continued to exhibit some bipolar behaviours this week as weak quarterly earnings of some of Wall Street’s biggest names contrasted with the emergence of encouraging economic indicators.

Significant declines across the Nasdaq had little impact on the formidable ascent of the Dow Jones Industrial Average, which extended its winning streak for a ninth straight session.

Disappointing reports from Tesla and Netflix hurt the Tech-Heavy Nasdaq Composite, causing it to drop by 2%.

Netflix in particular, apparently running out of ideas to skim cash from drooling couch surfers, copped losses of 8% on Thursday. Lower-than-expected revenue also reflects an intensifying market for mesmere-eyeballs and generally ordinary content.

Similarly, Tesla’s stock crashed circa 10% on the same day, following dullard comments from ingénue CEO Elon Musk, who spilled a few beans on lagging production during the current quarter, due to certain updates being made in its factories. Moreover, Musk hinted at possible price reductions for its electric vehicles in an attempt to boost demand amidst intensifying competition in the automotive industry, potentially exerting further pressure on the company’s quarterly profit margins.

Rania Gule, Market Analyst at XS.com told Stockhead that despite these setbacks, the Dow Jones Index managed to climb by 0.5%. That was led by a cracking 6% surge in Johnson & Johnson’s (JNJ), fuelled by stirring quarterly business data. JNJ has lifted its profit projections for the FY24 as a result.

“These stark discrepancies in the US stock markets come amidst the Federal Reserve’s efforts to control inflation and bring it back to its target rate of 2%,” Gule said.

“Recent American data indicated a significant decline in inflation rates for June, but they remained close to 3%, leaving investors and markets uncertain about whether the Federal Reserve will raise interest rates again later this year, possibly by a quarter-point increase in November, with a 30% likelihood.”

At the same time, economic data suggests that the US economy is nearing a recession, but the labor market remains robust, as evidenced by last week’s lower-than-expected jobless claims. Markets are now eagerly anticipating the release of existing home sales data next week, which could provide further insights into the housing market’s recovery.

Gule said that with the US stock market “in constant flux,” investors will want to remain vigilant for any of the unlikely (and seemingly daily) developments that may overturn market trends in the coming week.

What’s going down this week

Following a relatively quiet week in terms of economic data and events, the spotlight now turns to three major central banks: the Federal Reserve, the European Central Bank, and the Bank of Japan.

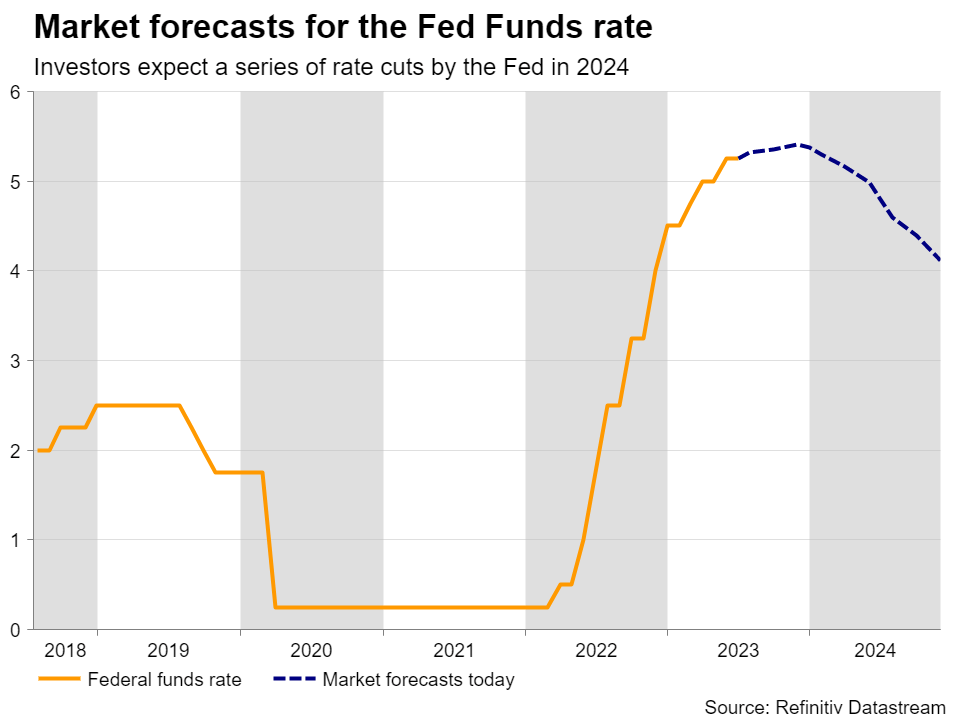

The Fed is expected to resume raising rates at the July 26 FOMC meeting. Fed funds futures see a 96% chance that the central bank will deliver a quarter-point rate rise, bringing the target range to between 5.25% and 5.50%.

That’s an almost a 22-year high, or one full third the age Our Editor Peter Farquhar looks on Sundays at 2300 hours.

Via Youtube: Unrelated distracting and foolish content.

“With investors anticipating only one more hike by the Fed, the focus will be on whether officials will signal the end of this hiking cycle, while with several ECB members pushing back on a September hike, it will be interesting to see whether (Christine) Lagarde has also changed her stance,” XM CEO told Peter McGuire told Stockhead over the weekend.

The Bank of Japan is leaning toward keeping its yield control policy unchanged at its policy meeting next week, according to Reuters sources, as policymakers prefer to scrutinise more data to ensure wages and inflation keep rising.

“With inflation having exceeded the BOJ’s target for more than a year, markets had been simmering with speculation the BOJ could tweak yield curve control as early as this month,” Pete says.

As for the BoJ, Governor Ueda’s latest remarks added to the likelihood of no action. Last week, Ueda again said there’s a way to go yet for Japan to ping that 2% inflation target ‘sustainably and with stability.’

So he’s determined to plough on with the ol’ ultra-loose policy for now.

The US Federal Reserve meeting.

A big one to be sure.

One which may well deliver the final interest rate blow of a hiking cycle Tenzing Norgay would’ve been proud of.

Even Norgay would be pleased with keeping up with the radical climb of the RBA’s latest idea of a hike (that’s the trail, in red):

Another unexpectedly tight weekly read last week from the unhappily effective US jobs market really left a lingering and pungently doubtful smell that ‘peak Fed’, as Reuters puts it, may or may not be upon us, just yet.

The jobs report last week showed a resilient labour market in Australia, with unemployment at near 50‑year lows, notes CBA.

The June quarter inflation figures should show further easing and will be front‑of‑mind ahead of the RBA’s August meeting.

Other local data out next week include retail trade, producer and trade prices.

Around the world, around the world …the focus will be on the US FOMC and Christine’s ECB monetary policy meetings, where CBA expects 25bp hikes at both.

“The BoJ also meets next week and in what we consider a finely balanced decision will likely keep policy settings unchanged,” the bank’s economics team said on Friday.

Three things to watch out for, with Joshua

We asked Josh Gilbert, Mild Mannered Market Analyst at eToro, to apply his relentless pursuit of returns by suggesting three key moments to look out for during the week ahead.

1. Australian Quarterly CPI – A key piece of the puzzle

After inflation significantly declined in June to 5.6% from 6.8%, the RBA kept rates on hold in July.

Next week sees the release of the quarterly CPI, which gives a more accurate reading of inflation in Australia and therefore, clearer data for the RBA to plot its next move. The average consensus from Bloomberg is that the quarterly CPI reading will decline to 6.2% from 7% in Q1 but similarly to the monthly readings, the consensus is broad; ranging from a low of 5.8% to a high of 6.7%. After this week’s employment numbers showed further resilience in Australia’s labour market, anything but reading under consensus at 6.2% would likely solidify another rate rise from the Reserve Bank next month.

It’d be surprising not to see at least one more hike from the RBA in its current cycle, with the threat of entrenched inflation still a clear worry for the board (something it noted in recent minutes) along with further evidence this week of a labour market that doesn’t look set to cool any time soon. There’s no doubt this impending data will be a market mover in the days ahead and may set up another volatile week on the ASX.

2. Rio Tinto Half-Year Results

China’s faltering economic recovery is impacting many sectors globally, but miners such as Rio Tinto are feeling the full impact of weaker demand from the world’s largest iron ore importer.

A second quarter production update this week showed its shipments fell by 1% from a year earlier, which could have an impact on its half-yearly results next week. It wasn’t all bad news, however. Rio still expects full-year iron ore shipments at the upper end of its guidance, which could soften the blow for any weakness in its half-year results announcement next week, if its outlook is positive. Strength from Q1, when iron ore prices rebounded from 2022 lows, may help to offset its disappointing Q2 production. The expectation is that EBITDA will jump by 17% next week from its H2 2022 results to $12.5 billion.

Unfortunately for investors, that still may not be enough to stop the miner’s typically impressive dividend from being trimmed next week.

3. A big week for big tech

Earnings weeks don’t get much bigger than this, with Microsoft, Alphabet, Amazon and Meta making up over 10% of the S&P500. After a poor start from Tesla and Netflix this week, investors will be eagerly awaiting more upbeat numbers from some of the world’s biggest names to ensure the tech rally doesn’t fade. This week has taught us that anything but a near-perfect report will be punished, given tech’s colossal rally and higher valuations.

AI will most likely take centre stage once again, with Microsoft set to be front-and-centre as a leader in the AI space, thanks to its stake in ChatGPT creator OpenAI. However, Wall Street will want to see the tech giants starting to convert this innovative technology into revenue.

Meta may be the standout, with earnings expected to grow year-over-year for the first time since Q3 2021.

This, combined with the Q3 2023 launch of its new ‘Threads’ platform, which earned 100 million new users in five days, making it the fastest-growing app of all time, could boost Q3 guidance for Meta. This level of success bodes well for the company as it seeks to turn around public sentiment following its patchy foray into the VR app space with the ill-fated ‘Horizon Worlds’.

The bottom line is that results need to be solid – and outlooks will be just as important. Big Tech has the potential to keep outperforming, particularly with AI tailwinds, but it certainly won’t be without its challenges.

Thanks Josh, don’t go changing, but also, don’t feel you’re not allowed to.

The Australian Economic Calendar

Monday July 24 – Friday July 28

All sources from Commsec, Trading Economics, S&P Global Research, AMP, Westpac

MONDAY

Australia Judo Bank Flash PMI, Manufacturing & Services

TUESDAY

Australia Inflation (Q2)

WEDNESDAY

Nope

THURSDAY

Australia Import and Export Prices (Q2)

FRIDAY

Australia Retail Sales (Jun, prelim)

Australia PPI (Q2)

The Everyone Else Economic Calendar

Monday July 24 – Friday July 28

MONDAY

Japan Jibun Bank Flash Manufacturing PMI

UK S&P Global/CIPS Flash PMI, Manufacturing & Services

Germany HBOB Flash PMI, Manufacturing & Services

France HCOB Flash PMI, Manufacturing & Services

Eurozone HCOB Flash PMI, Manufacturing & Services

US S&P Global Flash PMI, Manufacturing & Services

Malaysia Inflation (Jun)

Singapore CPI (Jun)

Taiwan Industrial Production, Retail Sales (Jun)

TUESDAY

United States House Price Index (May)

United States Consumer Confidence (Jul)

South Korea GDP (Q2, advance)

Indonesia BI Interest Rate Decision

Hong Kong Trade (Jun)

Germany Ifo Business Climate (Jul)

WEDNESDAY

United States New Home Sales and Building Permits (Jul)

United States FOMC Interest Rate Decision

Singapore Industrial Production (Jun)

THURSDAY

Eurozone ECB Interest Rate Decision

United States GDP (Q2, advance)

United States Durable Goods (Jun)

United States Initial Jobless Claims

United States Wholesale Inventories (Jun, advance)

United States Goods Trade Balance (Jun, advance)

United States Pending Home Sales (Jun)

China (mainland) Industrial Profits (Jun)

Hong Kong HKMA Interest Rate Decision

Taiwan Consumer Confidence (Jul)

Thailand Trade and Industrial Production (Jun)

FRIDAY

United States Personal Income and Spending (Jun)

United States Core PCE Index (Jun)

United States UoM Sentiment (Jul, final)

South Korea Industrial Production and Retail Sales (Jun)

Singapore Unemployment Rate (Q2, prelim)

Japan BOJ Interest Rate Decision

France GDP (Q2, prelim)

France Inflation Rate (Jul, prelim)

Germany PPI (Jul)

Taiwan GDP (Q2, advance)

Eurozone Economic Sentiment (Jul)

Germany Inflation (Jul, prelim)

Canada GDP (May, prelim)

Key US Earnings this week

Wall Street’s endless cycle of reports actually gets serious this week.

We’ve enjoyed L’amuse-bouche of US banks as a fine starter. Last week we got serious with the Big Tech Entrée (Hors-d’œuvre)

This week US earnings will go big and/or go home.

Key updates in alphabetical order are incoming from (wait for it…) Alphabet (GOOG).

Then sit back and enjoy…Airbus, AstraZeneca, AT&T, Barclays, BASF, Biogen, BNP Paribas, Boeing, Bristol-Myers Squibb, Chevron, Chipotle Mexican Grill, Comcast, Exxon, Ford Motor, General Electric, General Motors, GSK, Hermes International, Honeywell International, Intel, Mastercard, McDonald’s, Meta Platforms, Microsoft, Nestle, PG&E, Procter & Gamble, Raytheon Technologies, Samsung Electronics, STMicroelectronics, Texas Instruments, Thermo Fisher Scientific, UniCredit, Unilever, Union Pacific, Verizon Communications, Visa, and Volkswagen.

Here’s Monday in the States, Tuesday morning Sydenham time:

Monday morning #earningshttps://t.co/lObOE0dgsr$DPZ $APLD $PHG $BOH $BMRC $DX $HBT $HOPE pic.twitter.com/RCTp7IDTkr

— Earnings Whispers (@eWhispers) July 21, 2023

A really good picture:

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.