Traders’ Diary: Everything you need to know before the ASX opens

Via Getty

What grabbed the headlines last week?

Wall Street fell on Friday to end a freshly volatile period of trade in the red.

Last week, the trifecta of major US indices snapped their stupendous five-week winning streaks, with the S&P 500 closing down 0.4%, the Dow Jones tipping 0.1% lower, and the Nasdaq Composite sliding 1.3%.

Traders looked dazed and confused during more than a few periods of trade, especially when a second inflation report caused secondary chaffing over concerns the US central bank will now cut interest rates later, rather than sooner.

Earlier in the week, the US CPI (consumer price index) startled markets with a bigger than expected 3.1%.

Then came the January PPI report on Friday – up by a larger than expected 0.3%, while core PPI excluding food and energy prices jumped 0.5% – both measures forcing traders to rejig their rate cut expectations.

The odds of a 25 bps (basis point) rate cut by the Fed in March is now at 11% vs the 65% it was this time last month, as per the daily gyrations of the CME FedWatch tool.

That would seriously undermine all these recent return-to-growth bets on (largely) US tech stocks.

Meanwhile, US earnings season continues to paint a messy picture of corporate America.

To underline for emphasis, Nvidia (NVDA) the apparent conduit for AI/semiconductor bets, cruised past Google daddy, Alphabet’s (GOOGL) market cap midweek, to become the 3rd largest of the Mag 7 companies.

That was ahead of this week’s highly-anticipated Q4 earnings.

The 10-year Treasury yield spiked above 4.3% following the hot PPI reading, and the two-year Treasury yield topped 4.7% to its highest level so far this year.

US Earnings…

Around 80% of US S&P 500 companies have now reported December quarter earnings with 78% coming in better than expected, which is above the norm of 76%, according to AMP.

Earnings growth for the quarter is running around +9.4%yoy, which is well up from consensus expectations for 4.3% growth at the start of the reporting season.

US earnings growth has been (OFC) driven by technology companies (+40%) and financials (+11%) with resources earnings down 22%.

Finally, and closer to home, China’s economy remains as weird and unsettling as ever, while Japan also finds itself in a technical recession after Q4 GDP fell 0.1% following a drop off in household spend and investment.

Local markets…

The global macro-economic juices are gurgling away just beneath equity markets and last week’s return to volatility is a direct result of mixing signals.

A lot of local blue chip stocks did a fair bit of snakes and ladders. Apparently some 20% of the ASX 200 constituents finished last week higher or lower by more than +5%.

The ASX200 (XJO) index

That being said, only one-third of those were falls, the rest were all ladders as Q3 earnings reads more like Jack Kerouac than Bram Stoker.

Despite some distractions, the central bank chief Michele Bullock and her Reserve Bank brains trust have continued to see the right card on inflation turn up at the right time. Last week’s jobless rate a good case in point.

What was another choppy week for traders on all sorts of levels, was more or less rescued midweek by unemployment lurching a little on the upside.

Josh Gilbert, market analyst at eToro, says the local labour market is loosening.

“Rising unemployment will be a significant reason for the RBA to cut rates, with market pricing looking to as early as June for the first.”

This week, the board receive another key data point in the shape of the Quarterly Wage Index.

“With capacity in Australia’s job market growing, wages should not see too much pressure to the upside from here, given that we will likely see the unemployment rate grow during 2024, all of which is good news for inflation,” Josh says.

The Wage Price index is expected to lift to 1% QoQ and to 4.1% year-over-year next week.

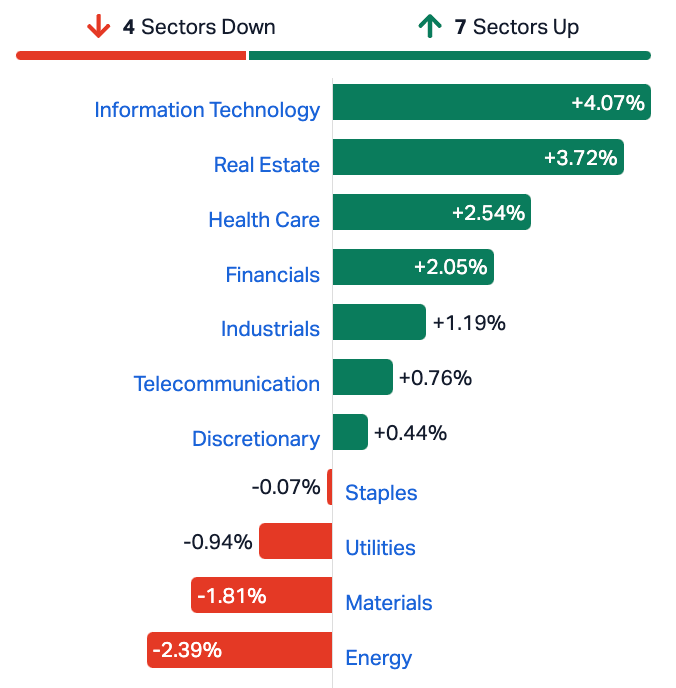

ASX Sectors Last Week

The Week Ahead

It’s another exciting week for all you crazy central bank watchers out there, with key decisions from Mainland China, Turkey, Indonesia and South Korea, while meeting minutes from the Federal Reserve and Reserve Bank of Australia drop.

According to S&P Global Fed chair Jerome Powell has already caused markets to pull back their expectations of a March rate cut with his recent comments.

Elsewhere we have business and consumer confidence surveys such as Germany’s Ifo, as well as a bevvy of official inflation numbers from all over.

Thursday is pretty much global PMI day.

The Aussie Economic Calendar

Monday February 19 – Friday February 23

All sources: IG Markets, S&P Global Market Intelligence, CommSec

MONDAY

Nope

TUESDAY

Australia RBA Meeting Minutes (Feb)

WEDNESDAY

Australia Wage Price Index (Q4)

THURSDAY

Australia Judo Bank Flash PMI, Manufacturing & Services

FRIDAY

Nope

The Everyone Else Economic Calendar

Monday February 19 – Friday February 23

MONDAY

Japan Machinery Orders (Dec)

Thailand GDP (Q4)

Canada PPI (Jan)

Brazil Business Confidence (Feb)

Tuesday

China (mainland) Loan Prime Rate (Feb)

Malaysia trade (Jan)

Switzerland Balance of Trade (Jan)

South Africa Unemployment (Q4)

Canada Inflation (Jan)

United States CB Leading Index (Jan)

China (mainland) New Yuan Loans, M2, Loan Growth (Jan)

Wednesday

South Korea Business Confidence (Feb)

Japan Balance of Trade (Jan)

Turkey Consumer Confidence (Feb)

Indonesia BI Interest Rate Decision

South Africa Inflation (Jan)

Eurozone Consumer Confidence (Feb, flash)

United States Fed FOMC Minutes (Jan)

Thursday

Japan au Jibun Bank Flash PMI, Manufacturing & Services

India HSBC Flash PMI, Manufacturing & Services

UK S&P Global Flash PMI, Manufacturing & Services

Germany HCOB Flash PMI, Manufacturing & Services

France HCOB Flash PMI, Manufacturing & Services

Eurozone HCOB Flash PMI, Manufacturing & Services

US S&P Global Flash PMI, Manufacturing & Services

New Zealand Trade (Jan)

South Korea BoK Interest Rate Decision

France Business Confidence (Feb)

Hong Kong SAR Inflation (Jan)

Italy Inflation (Jan, final)

Eurozone Inflation (Jan, final)

Turkey TCMB Interest Rate Decision

Mexico GDP (Q4, final)

Canada Retail Sales (Dec)

United States Existing Home Sales (Jan)

United Kingdom Gfk Consumer Confidence (Feb)

Friday 23 Feb

China (mainland) House Price Index (Jan)

Malaysia Inflation (Jan)

Singapore CPI (Jan)

Germany GDP (Q4, final)

Germany Ifo Business Climate (Feb)

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.