Traders’ Diary: Everything you need to get ready for the week ahead

Via Getty

What grabbed the headlines last week?

Last week’s various indicative droppings on what kind of landing to expect provided global markets with some reassuringly softly-softly comfort, since most of the big ones are as far from the bottom as they’ve been, in many cases ever.

That’s not why they’ve become anxiously sensitive to the usual stuff like jobless reports and inflation prints, but in the absence of central bank forward guidance, all one need know is there’s a long ways to fall.

The Dow Jones added 135 points, to close at a fresh record high above the mercurial 40,00o mark.

The S&P 500 edged higher by 0.1%, while the Tech-Heavy Nasdaq finished a little lower.

Also: meme stocks.

The ASX200 done good, climbing circa 0.8% last week after retesting its all-time high on Thursday.

Seven of the 11 ASX sectors were higher over the last week.

Materials jumped 2.5%. Consumer fun stocks added 3.2%.

After setting a new 20-day high, the index benchmark climbed 0.84% last week and is currently 1.21% off of its 52-week high.

Doves flew all over last week, the data here and in the US screamed economic slowdown and potentially less inflation over April.

The US CPI month-on-month came in at 0.3%, below the estimated 0.4%, delivering the first slowdown of 2024.

Happily – unless you’re out of work – Aussie unemployment rose last month, the jobless rate hitting 4.1% in April from 3.9% in March.

And in Toronto, the stocks are rising, pronto.

The ASX200’s doppleganger S&P/TSX Composite clocked a new record high, with wins for the resources stocks eclipsing losses for IT.

The London exchange ended lower, European stocks have ended the week slowly sliding but only after thwacking into the windshield of multi-decade highs at an impressive velocity on Wednesday.

Very exciting end of the week also for anyone keen on China coming to the or even a party in 2024. Iron ore fans will have noted the measures by our governing mates in Chinese, who appeared to have had a genuine crack at actually sorting the unending nightmare of the country’s bloated property market.

The deets remain skinny, but Beijing’s reported plans to get local govs to snap up all the unsold homes and rescue the Party’s property crisis, is by far the brassiest stimmy scheme yet.

Either way, the Pilbara coloured 62% iron ore which Chinese steel makers like to buy ended last week not too far from the US$120 it went for to start the month – an eight-week high.

The PBoC also lifted China’s minimum mortgage interest rate and lowered downpayment rates – along with deploying some 1 trillion yuan in long-dated bonds, the central bank’s measures actually might make people spending money in Chinese property feel less screwed – and should Chinese state bodies go buy up some unsold property inventory at reasonable prices… well, that would be a game changer for the world’s crappest, most rigged game.

Silver climbed past $30 per ounce, its highest level since January 2013 and up more than 25% year-to-date, fuelled by both investment and industrial demand. ETFs featuring the precious metal haven’t really budged, but actual silver’s gone nuts.

Aluminium futures hit US2,600 per tonne in May, the highest since the near-two-year peak of $2,670 on April 22nd, tracking broad-based gains for main base metals.

US Earnings

The season is just about done, because the next one is almost here.

A few notables dribbling in over the next few days:

Nvidia, Palo Alto Networks, Nvidia, Lowe’s, Nvidia, PDD Holdings, Nvidia, TJX Companies, Nvidia, Analog Devices, Synopsys, Nvidia, Target, and Intuit.

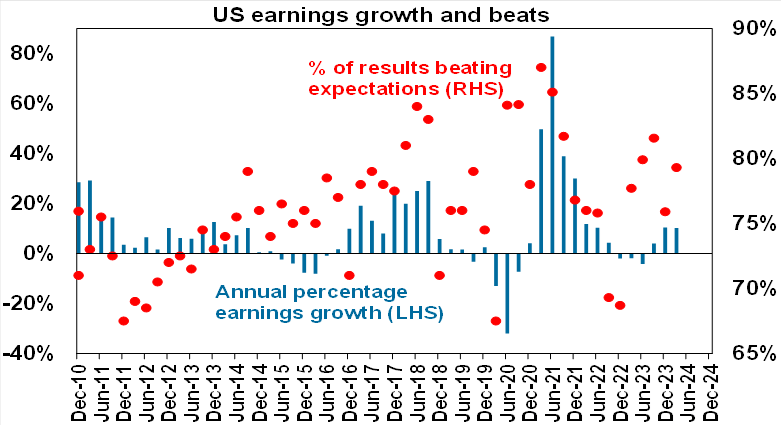

According to AMP, 92% of S&P 500 companies have reported with 79% beating, against a norm of 76% and earnings growth expectations now at 10%y-o-y, up from 4.1% on four weeks ago.

The Week Ahead

We’re watching the Chinese central bank, as the PBoC makes a call on its key lending tool, the (LPR) loan prime rates later Monday.

The betting is for a hold as the need for yuan support weighed against Beijing’s target for higher loan demand.

Meanwhile, the shock and yawn of when the US Fed will lower rates will somehow ramp even further up that ramped-up ramp this week with the imminent release of the FOMC minutes and appearances by various Fed speakers.

After that, the Michigan Consumer read is about as hot as data plans to get in the United States.

An early peek at the economic conditions for May start rolling out all over the place this week, via a slew of S&P Global Flash PMIs, while inflation data drops in London and Tokyo.

Speaking of, there’s some big central bank meets in our neck of the woods, South Korea, Indonesia and further afield – most exciting, in Turkey.

And we’re flashing wildly on PMIs which will provide a handy glimpse into regional business conditions from Delhi, to Tokyo and Canberra.

April data showed India’s economy continuing to grow at one of the strongest rates seen over the past 14 years.

S&P reckons Aussie business expansion is running close to two-year highs.

Also happening here – May’s Westpac consumer sentiment index and PMI prints, while (almost forgot) the RBA drops its minutes from the last rates meeting on Toosday.

US Futures overnight:

The Economic Calendar

Monday May 20 – Friday May 24

MONDAY

Canada, Norway, Switzerland, India Market Holiday

China (Mainland) Loan Prime Rate (May)

Malaysia Trade (Apr)

Germany PPI (Apr)

Taiwan Export Orders (Apr)

TUESDAY

Australia Westpac Consumer Confidence (May)

Australia RBA Meeting Minutes

Eurozone Balance of Trade (Mar)

Canada Inflation (Apr)

WEDNESDAY

Singapore, Thailand, Malaysia Market Holiday

Japan Balance of Trade (Apr)

Japan Machinery Orders (Mar)

New Zealand RBNZ Interest Rate Decision

United Kingdom Inflation (Apr)

Indonesia BI Interest Rate Decision

South Africa Inflation (Apr)

United States Existing Home Sales (Apr)

United States FOMC Meeting Minutes (May)

THURSDAY

Indonesia Market Holiday

Australia Judo Bank Flash PMIs

Japan au Jibun Bank Flash PMIs

India HSBC Flash PMIs

UK S&P Global Flash PMIs

Germany HCOB Flash PMIs

France HCOB Flash PMIs

Eurozone HCOB Flash PMIs

US S&P Global Flash PMIs

South Korea BoK Interest Rates

Singapore Inflation (Apr)

Taiwan Industrial Production (Apr)

Hong Kong SAR Inflation (Apr)

Turkey TCMB Interest Rate Decision

Mexico GDP (Q1, final)

Eurozone Consumer Confidence (May)

United States New Home Sales (Apr)

FRIDAY

Indonesia Market Holiday

New Zealand Trade (Apr)

Japan Inflation (Apr)

Singapore GDP (Q1, final)

Malaysia Inflation (Apr)

Singapore Industrial Production (Apr)

United Kingdom Retail Sales (Apr)

France Business Confidence (May)

Canada Retail Sales (Mar)

United States Durable Goods Orders (Apr)

United States UoM Sentiment (May, final)

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.